This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It serves as a broad-based, independent standard measure of credit risk. It is relied upon by stakeholders across the entire lending ecosystem – from regulators, investors and boards to consumers, lenders, and brokers – as a baseline metric for assessing credit risk that is fair to both lenders and consumers. .

“Growing debt balances, stubborn interest rates and elevated prices are still a thorn for consumers, and contribute to their overall financial stability,” explains TrueAccord CEO Mark Ravanesi in his Q4 Industry Insights: Cautious Optimism with a Side of Holiday Hangover.

Add these all together and the financial outlook for consumers, especially those in debt, is scary. For one, the consumercredit market is looking strong with signs of expansion, specifically, originations for credit cards and personalloans are increasing. And lenders are happy to lend.

Before you create your plan, try calling your lenders to simply ask if they’re willing to work out a payment schedule that fits in with your plan. Sign up for consumercredit counseling. Many credit card lenders allow you to transfer personalloans, and other types of debt, not just your credit card balance.

Rent, home payments, utilities such as gas, water, electric, and even things like cable or other on-time payment history can be used by credit bureaus to create a reliable credit score from which they can underwrite credit. What lenders use alternative credit data to grant credit?

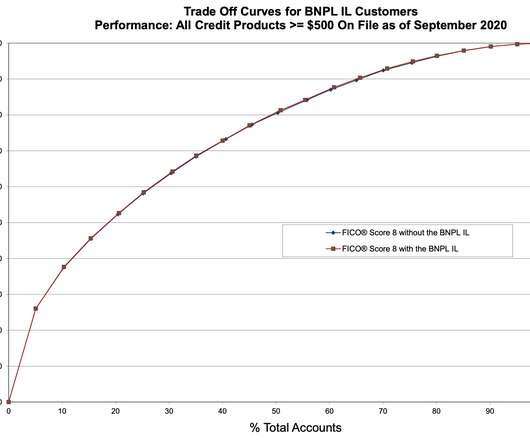

As BNPL loans become a more commonplace form of credit used by consumers, these loans could also become an important factor in consumercredit reports, and by extension, in the FICO ® Scores based on those credit reports. The BNPL accounts in question were reported as installment loans to Experian.

Then, avoid putting any more money on credit cards until you’ve paid off most of the consolidation loan. . Compare Rates on Debt Consolidation Loans. First, call all your lenders and tell them what’s going on. How much debt does the average person owe? . How Can I Get Out of Debt with No Money?

“Growing debt balances, stubborn interest rates and elevated prices are still a thorn for consumers, and contribute to their overall financial stability,” explains TrueAccord CEO Mark Ravanesi in his Q4 Industry Insights: Cautious Optimism with a Side of Holiday Hangover.

The FICO® Score 10 Suite, which includes FICO Score 10 and FICO Score 10 T, is now generally available from all three credit bureaus. The FICO® Score 10 Suite outperforms all previous FICO Scores, giving lenders unparalleled predictive power to make more precise lending decisions.

TransUnion ( NYSE: TRU ) confirmed that consumercredit activity keeps rising from the COVID-19 pandemic lows, but some areas like automobile loans (subprime) performance have lagged. Matt Komos , VP of Research and Consulting at TransUnion, stated: “On the surface, the consumercredit market is performing quite well.

In reality, its impact would extend far beyond payday lenders to the broader consumercredit market to cover affordable small dollar loans (including “accommodation” loans) that depository institutions are being encouraged to offer, credit cards, personalloans, and overdraft lines of credit,” the letter reads. “As

From April 2021 to April 2022, mortgage loan missed payment rates have remained stable likely driven by the continued home price appreciation and the higher payment accommodation rates for mortgage loans than those for bankcards and auto loans. Now, the average FICO® Score has leveled off during the second year of the pandemic.

A prime credit score typically refers to a high credit score, usually above 720. It shows lenders that you have a history of responsibly managing credit and can qualify you for better loan terms and lower interest rates. Few numbers are as important as your credit scores.

We found that FICO® Resilience Index continues to be a strong predictor of the presence of loan accommodations in place as of October 2020 – representing a mix of “long haul” accommodations by mortgage lenders and newer short-term accommodations allowed on bankcard, auto finance and personalloan accounts.

A hike in the federal interest rate prompts a jump in the Bank Prime Loan Rate ( prime rate ), the credit rate that banks offer to their most credit-worthy customers and off of which they base other forms of consumercredit like mortgages and consumerloans. Key Factor 3: Rising Delinquencies.

The new FICO XD scoring model retrieves information from sources like the National Consumer Telecom and Utilities Exchange to collect data on payments to utility, cell phone service, internet, and cable television providers and uses the payment history data from these and other sources to build a credit score.

Consumers trying to make ends meet have continued turning to credit cards and other credit types to bridge the income to expense gap. consumercredit card debt has increased to nearly $1 trillion. Credit card balances jumped more than $60 billion over Q4 2022, lifting the total amount of U.S.

Information and data continue to be key tools at our disposal to better understand the dynamics of the last couple of years, and better navigate what lies ahead for the Canadian consumercredit environment. In this post, we have been citing trends and insights based on the latest FICO® Score for the Canadian market – FICO® Score 10.

auto, mortgage, personalloan) and lifecycles (e.g., In other words, even as the relationship between odds of repayment and score has shifted, the score has retained its powerful ability to distinguish repayment likelihood between low and high scoring consumers. originations).

The DFPI continues to experience and respond to a more than 40 percent increase in consumer complaints, calls and inquiries since the onset of COVID-19 in the state. The DFPI is tracking all COVID-19 related complaints and reporting harmful emerging consumer trends to the enforcement division for investigation.

How Might Buy Now, Pay Later Loans Impact FICO® Scores? Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. consumercredit files. But on the other hand, adding positive BNPL payment data in the consumercredit file could help the FICO® Score.

Citi also offers personalloans, lines of credit, and mortgages, which can prompt a hard inquiry. If you are overwhelmed by dealing with negative entries on your credit report, we suggest you ask a professional credit repair company for help. They’re required for getting new credit. Balance transfers.

Citi also offers personalloans, lines of credit, and mortgages which can prompt a hard inquiry. If you are overwhelmed by dealing with negative entries on your credit report, we suggest you ask a professional credit repair company for help. Luckily, hard inquiries are some of the least significant credit entries.

Then kindly ask the debt collector to remove collections from your credit report out of goodwill. With some newer scoring models of FICO and VantageScore, they ignore a collection marked as “paid”, though many lenders still utilize older formulas that will still weigh a paid collection account against you. TrueAccord.

.” Between the lines: The stabilization in delinquency rates reflects improved household budgets, with 63% of consumers reporting finances as “as planned or better” in late 2024. Learn more.

With inflation proving more sticky than policymakers had hoped and uncertainty around how the new administrations policies might affect it, it may take longer for people to see lower interest rates on their mortgages, car loans and credit card balances, which could prove challenging to household budgets.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content