This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With inflation proving more sticky than policymakers had hoped and uncertainty around how the new administrations policies might affect it, it may take longer for people to see lower interest rates on their mortgages, car loans and credit card balances, which could prove challenging to household budgets. for this year, increased to 3.0%

“Growing debt balances, stubborn interest rates and elevated prices are still a thorn for consumers, and contribute to their overall financial stability,” explains TrueAccord CEO Mark Ravanesi in his Q4 Industry Insights: Cautious Optimism with a Side of Holiday Hangover.

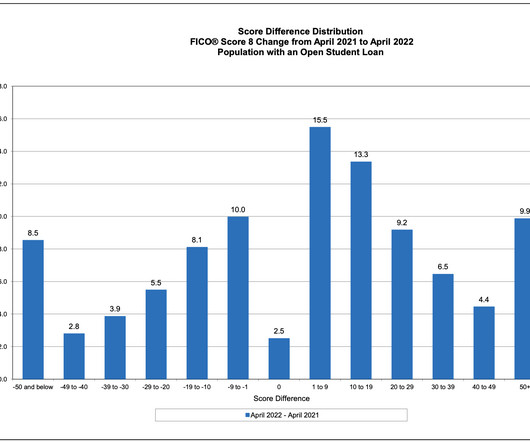

Home Blog FICO Are StudentLoan Holders at Risk as Deferments Expire? Here we present results of our research into FICO® Score dynamics for holders of studentloan debt between 2021 and 2022, to give an indication of key factors that seem to accompany large decreases in the FICO Scores of this population.

On September 29, the Consumer Financial Protection Bureau (CFPB or Bureau) released a special edition of its Supervisory Highlights , focusing on studentloan servicing. It’s time to open up the books on institutional student lending to ensure all students with private studentloans are not harmed by illegal practices.”.

On November 17, the Consumer Financial Protection Bureau (CFPB) announced it is seeking public comment on its proposal to develop a new data set to better monitor the auto loan market. Because studentloans are largely administered by the federal government, we know more about them too.

Consumers trying to make ends meet have continued turning to credit cards and other credit types to bridge the income to expense gap. consumercredit card debt has increased to nearly $1 trillion. Credit card balances jumped more than $60 billion over Q4 2022, lifting the total amount of U.S.

“Growing debt balances, stubborn interest rates and elevated prices are still a thorn for consumers, and contribute to their overall financial stability,” explains TrueAccord CEO Mark Ravanesi in his Q4 Industry Insights: Cautious Optimism with a Side of Holiday Hangover.

The four key trends we’re studying are: resumed foreclosure activity, extensive medical bills, the end of child tax credits and historically high inflation. Add these all together and the financial outlook for consumers, especially those in debt, is scary. And lenders are happy to lend. But there are silver linings, as well.

Then, avoid putting any more money on credit cards until you’ve paid off most of the consolidation loan. . Compare Rates on Debt Consolidation Loans. First, call all your lenders and tell them what’s going on. Check Your Credit Score. Winners keep score—and they stay on top of their credit scores, too.

Meanwhile, the Consumer Financial Protection Bureau (CFPB) has been busy, with new rules impacting lenders and collectors across the spectrum. Read on for our take on what’s impacting consumer finances, how consumers are reacting and what else you should be considering as it relates to debt collection in 2024.

In July 2016, the Consumer Federation of America (CFA) and VantageScore Solutions reported that most consumers—more than 80%—knew basic facts about their credit scores, including that credit scores are used by lenders to approve or deny mortgages and by credit card issuers to approve or deny credit cards.

As BNPL loans become a more commonplace form of credit used by consumers, these loans could also become an important factor in consumercredit reports, and by extension, in the FICO ® Scores based on those credit reports. The BNPL accounts in question were reported as installment loans to Experian.

While consumer groups praised the bill for its recourse for consumers harassed by debt collectors, CUNA and NAFCU saw the bill as complicating the legal relationship between consumers, members and lenders. In the letter, Nussle stated, “Lenders rely on complete and accurate credit reports when underwriting loans.

Credit Risk and FICO Score Trends? And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, such as in the form of rising balances, credit seeking behavior, and eventually for some, missed payments.

Lenders use a multitude of scoring methods to determine your creditworthiness and make decisions about whether or not to give you credit. It gathers credit reports from the three major credit bureaus and analyzes anonymous consumer data to generate a scoring model specific to each bureau.

Pursuant to its authority under Section 1022(b)(1) of the Dodd-Frank Act, the Consumer Financial Protection Bureau (CFPB) issued an advisory opinion to consumer reporting agencies (CRAs), highlighting their obligation to screen for and eliminate obviously false data from consumers’ credit reports.

We found that FICO® Resilience Index continues to be a strong predictor of the presence of loan accommodations in place as of October 2020 – representing a mix of “long haul” accommodations by mortgage lenders and newer short-term accommodations allowed on bankcard, auto finance and personal loan accounts. by Sharon Tilley.

Buy now, pay later services act as a lender of sorts and are currently not licensed by the state. Hochul specifically mentioned studentloan servicers who encourage the quickest repayment plans or plans not suitable for the party repaying. The government will look to stop these exploitative tactics and more.

It has taken actions to collect data on a number of new industries, including debt relief and earned wage access providers, and has filed a cease-and-desist order against a studentloan debt relief company charging borrowers exorbitant fees for the false promise of getting their student debt wiped.

The ConsumerCredit Protection Act caps these types of garnishments. These liens notify lenders of the creditor’s rights to your property. Exceptions apply for things like child support, spousal support, studentloans and some property liens. The lessor of these two amounts applies. Property liens.

Just like with consumercredit, debt from a civil judgment must be validated under the Fair Credit Reporting Act. How Long Do Judgments Stay on My Credit Report? Just like consumercredit, court-ordered debt could stay on your credit report up to seven years if you don’t take action to remove it.

A hike in the federal interest rate prompts a jump in the Bank Prime Loan Rate ( prime rate ), the credit rate that banks offer to their most credit-worthy customers and off of which they base other forms of consumercredit like mortgages and consumerloans. Key Factor 3: Rising Delinquencies.

Buy now, pay later services act as a lender of sorts and are currently not licensed by the state. Hochul specifically mentioned studentloan servicers who encourage the quickest repayment plans or plans not suitable for the party repaying. The government will look to stop these exploitative tactics and more.

For example, if you fail to pay a debt, the lender can take you to court. Ultimately, if you don’t pay a debt , the lender or bill collector can file a lawsuit against you to recoup the money. The ConsumerCredit Protection Act caps these types of garnishments. What Is a Judgment on a Credit Report? Property liens.

PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels. The proposed rule would require lenders to assess a borrower’s ability to repay a PACE loan and would provide a framework for how these loans will be treated under the Truth in Lending Act.

The Department has also begun licensing debt collectors. The first change under the CCFPL was a new name for the Department which was formerly the Department of Business Oversight.

Nelson, aged 27, took out a private studentloan of $10,000 to cover unforeseen college costs after using up his federal loan. You can use several methods: Consumercredit counseling. Mary and Stuart ended up with $14,000 in department store debt after their wedding costs escalated beyond their budget. “A-”

The FTC’s Safeguards Rule requires nonbanking financial institutions, such as mortgage brokers, motor vehicle dealers, and payday lenders, to develop, implement, and maintain a comprehensive security program to keep their customers’ information safe. For more information, click here. On October 26, Senator Cynthia M.

On July 26, the CFPB published a blog focused on consumercredit scores. On July 25, a large credit reporting agency revealed to investors in regulatory filings that it’s facing a probe by the CFPB. For more information, click here. For more information, click here.

The report highlights enforcement actions related to the acts and their implementing regulations, including in the areas of automobile purchases and financing, payday lending, credit repair and debt relief, other credit, and electronic fund transfers. For more information, click here. For more information, click here.

On April 14, the Consumer Financial Protection Bureau (CFPB or Bureau) published a report titled StudentLoan Borrowers Potentially At-Risk when Payment Suspension Ends. Pre-pandemic payment assistance on studentloans. Pre-pandemic payment assistance on studentloans. Multiple studentloan servicers.

Federal Activities: On April 14, the Consumer Financial Protection Bureau (CFPB or Bureau) published a report titled, “ StudentLoan Borrowers Potentially At-Risk when Payment Suspension Ends.” Pre-pandemic payment assistance on studentloans. Pre-pandemic payment assistance on studentloans.

Federal Activities: On September 29, the Consumer Financial Protection Bureau (CFPB) released its fifth biennial report to Congress on the consumercredit card market, finding that the market’s growth over the last few years reversed course in 2020. Privacy and Cybersecurity Activities. Among other provisions, S.B.

Supreme Court in support of the Biden administration’s studentloan forgiveness plan. Among the changes discussed by Governor Hochul in her State of the State Address is a plan to amend the state’s ConsumerCredit Fairness Act to cover medical debt. For more information, click here. For more information, click here.

On October 21, the Eighth Circuit temporarily blocked President Joe Biden’s studentloan forgiveness program. On October 20, Supreme Court Justice Amy Coney Barrett, who oversees Seventh Circuit emergency matters, rejected an emergency request to stop President Biden’s studentloan forgiveness program.

Uejio has been with the CFPB since 2011 and worked with Chopra, who served as the bureau’s studentloan ombudsman during the Obama administration. That experience will enable Uejio to lay solid groundwork for Chopra, said Richard Cordray, the bureau’s first director. The two share many of the same priorities, Cordray said.

On June 30, the CFPB released a blog post regarding trends of commercial reporting on consumercredit. State Activities: On July 14, Colorado’s attorney general (AG) will hold a virtual meeting to discuss new draft rules on studentloan servicing and collections. For more information, click here.

One of the more fascinating platform items of the Biden presidential campaign was the idea of transferring consumercredit ratings from Equifax (NYSE: EFX), Experian PLC (OTC: EXPGY) and TransUnion (NYSE: TRU) to a public registry under the Consumer Financial Protection Bureau. Paying off a mortgage can reduce a credit score.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content