This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

So credit repair, consumercredit and credit bureaus—they’re all tied together. To understand why they’re so important, you might want to learn a bit more about the history of credit scores and repair. Luckily, we’ve compiled everything you need to know about the history of the credit repair industry.

It marks the highest fine ever issued to a lender for what it deemed a breach of consumercredit rules. But more tellingly, the penalty related to the mistreatment of business and personal customers who fell behind on credit card and loan payments between 2014 and 2018 – well before many of us had even heard of COVID-19.

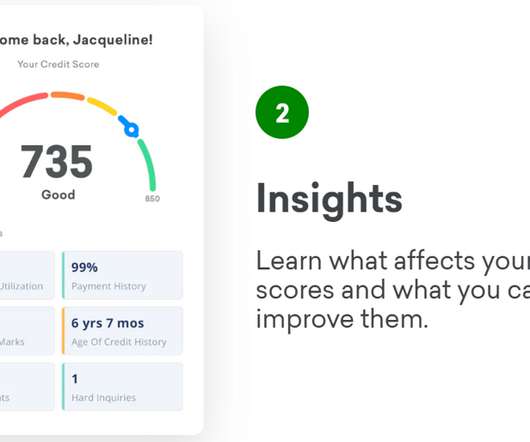

At any given point, we may have several credit scores based on our financial history, as measured by companies such as FICO or VantageScore Solutions, another credit analysis company. It’s important to keep in mind that your score is calculated using both positive and negative information on your credit reports.

Find out more about free credit repair for low-income families and individuals below. As of early 2023, you could still get your free credit report once a week with each of the bureaus, though this option may end at any time. Request the report in writing after being denied credit. Get your credit score via your lender.

That’s why at FICO we are constantly innovating with alternative data sources that go beyond the traditional credit bureau file to increase financial inclusion and bring more of these consumers into the system. Rental payment data has always been largely absent from consumers’ credit files. Categories. Scoring Solutions.

October 26, 2020, marks the 50th anniversary of the Fair Credit Reporting Act (FCRA, 15 U.S.C. which along with the Fair Debt Collection Practices Act, Telephone Consumer Protection Act, Section 5 of the Federal Trade Commission Act, and the Truth in Lending Act, forms the foundation of federal consumer rights law in the United States.

In affirming the lower court’s findings, the Eleventh Circuit held that a defendant does not “recklessly” violate the FCRA unless its interpretation of the FCRA’s requirements was “objectively unreasonable” under the statute itself or under other applicable guidance outlined by the courts or agencies such as the Federal Trade Commission (“FTC”).

Such events cast many borrowers into uncomfortable territory, creating what may be a defining moment in the relationship between them and their lenders. Lenders who get the strategy right may earn a loyal customer for life, while those who misfire risk cannibalizing valuable long-term relationships that often span multiple asset classes.

FICO® Score At 716, Indicating Improvement In ConsumerCredit Behaviors Despite Pandemic. Ethan Dornhelm wrote: The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of credit risk. Fewer consumers are actively seeking credit.

A recent settlement between the Federal Trade Commission (FTC) and a lead generator provides new insight into the FTC’s enforcement of sensitive personal data collection and sales under the Fair Credit Reporting Act (FCRA) and the agency’s Section 5(a) authority. Consent Order Requirements and Penalties.

On January 20, 2023, California Attorney General Rob Bonta submitted a letter to the CFPB agreeing with its preliminary determination that California’s Commercial Financing Disclosures Law (CFDL) is not preempted by TILA because the CFDL only applies to commercial financing and not to consumercredit transactions within the scope of TILA.

s something that the CSA and other trade bodies, as well as firms, have argued is overdue from as far back as 2014.? ?Communications Communications with consumers in default do need to be clear and comprehensible, but they now need to be designed for the 21st century and sensitive to customer circumstances. ? Chris adds. ?The

On March 6, the Commodity Futures Trading Commission (CFTC) Chair Rostin Behnam called on Congress to pass legislation addressing regulatory jurisdictions in the crypto industry. The SEC alleged that Shapeshift violated Section 15(a) of the Securities Exchange Act of 1934 by facilitating trades in crypto assets without registration.

In keeping with Federal Trade Commission rules , Freedom Debt Relief doesn’t charge upfront fees. Focused on protecting and helping consumers. In 2010, the company helped to establish Federal Trade Commission rules to ban abusive debt settlement practices and protect consumers. Ads by Money.

The FTC’s Safeguards Rule requires nonbanking financial institutions, such as mortgage brokers, motor vehicle dealers, and payday lenders, to develop, implement, and maintain a comprehensive security program to keep their customers’ information safe. For more information, click here. For more information, click here.

For example, the bill distinguishes a “digital asset” from a “digital commodity,” empowering the Securities and Exchange Commission (SEC) to regulate the former and the Commodity Futures Trading Commission (CFTC) to regulate the latter. On July 26, the CFPB published a blog focused on consumercredit scores.

The CFPB also released several reports shining a light on factors that may influence fair access to credit, including how medical debt affects tens of millions of consumers’ credit profiles, how people in under-resourced rural areas struggle to access financial services, and the challenges faced by justice-involved individuals and families.

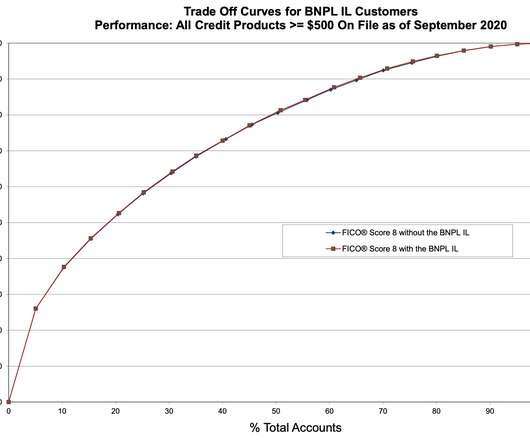

Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. market: BNPL reporting approach: How a BNPL lender reports these accounts to a credit bureau can materially influence the impact these loans ultimately have on the FICO® Score. consumercredit files.

Federal Activities: On September 29, the Consumer Financial Protection Bureau (CFPB) released its fifth biennial report to Congress on the consumercredit card market, finding that the market’s growth over the last few years reversed course in 2020. On September 28, Federal Trade Commission (FTC) Chair Lina M.

Since you are more of a participant in the process, you’ll have a better understanding of your individual situation when you reach out to a credit repair company. Other times a tax lien may have been resolved in reality but not reported as resolved to one of the three credit reporting agencies. Alternatives to Credit Repair.

The proposed rule would require lenders to assess a borrower’s ability to repay a PACE loan and would provide a framework for how these loans will be treated under the Truth in Lending Act. On May 1, the Federal Trade Commission (FTC) announced a permanent ban from debt relief telemarketing for operators of debt relief scam.

Two trade groups the Consumer Data Industry Association (CDIA) and the Cornerstone Credit Union League yesterday filed a lawsuit in the District Court for the Eastern District of Texas against the Consumer Financial Protection Bureau over its new rule prohibiting the inclusion of most medical debts on consumercredit reports.

On January 26, the Securities and Exchange Commission (SEC) rejected Cboe BZX Exchange’s (BZX) request to list and trade Ark 21Shares, the proposed spot-Bitcoin exchange traded fund (ETF) managed by asset managers ARK Investment Management and 21Shares (collectively hereinafter, the “trust). For more information, click here.

On June 8, the Commodities Futures Trading Commission (CFTC) obtained a default judgment against a decentralized autonomous organization (DAO) Ooki Dao in the U.S. with operating its crypto asset trading platform as an unregistered national securities exchange, broker, and clearing agency. For more information, click here.

To help you keep abreast of relevant activities, below find a breakdown of some of the biggest events at the federal and state levels to impact the Consumer Finance Services industry this past week: Federal Activities. State Activities. For more information, click here. On October 19, the U.S. For more information, click here.

To help you keep abreast of relevant activities, below find a breakdown of some of the biggest events at the federal and state levels to impact the Consumer Finance Services industry this past week: Federal Activities. million to consumers and pay a $500,000 civil penalty for deceiving consumers with false claims about their services.

The proposed rule would require lenders to assess a borrower’s ability to repay a PACE loan, as well as provide a framework for how these loans will be treated under the Truth in Lending Act. On April 27, Federal Trade Commission (FTC) Chair Lina M. Brown argued that medical debt “correlates with illness,” not with credit risk.

20 tapped Uejio, previously the Consumer Financial Protection Bureau’s chief strategy officer, to run the agency until his nominee for permanent director, Rohit Chopra, is confirmed. Chopra is currently a member of the Federal Trade Commission. President Biden on Jan.

There are some exceptions: The Military Lending Act caps interest for active duty servicemembers and dependents at 36% for consumercredit. Federally chartered credit unions have an 18% limit. Eight trade groups representing lenders such as banks and credit unions wrote a letter to Sen. For example, Sen.

On October 18, the Federal Trade Commission (FTC) announced that a for- profit college has been ordered to cancel $3.4 Among other provisions under the stipulated order, the for-profit school must request that consumer reporting agencies delete the debt from consumers’ credit reports. For more information, click here.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content