This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York , leading to a shift in consumer spending for 2024. And we’re seeing consumers often need help to organize the different debts.”

As part of the settlement, the entities will forgive $223,685 in loans, pay $33,991 in restitution, and pay $33,000 in civil penalties and costs to the state. As part of the settlement, the entities will forgive $223,685 in loans, pay $33,991 in restitution, and pay $33,000 in civil penalties and costs to the state.

“Amounts owed” comprises some 30% of the overall FICO® Score calculation and is heavily weighted towards credit card balances and utilization so the observed reduction in credit card debt is helping to drive scores upwards. Fewer consumers are actively seeking credit. There has been a 12.1% The Other Side of the Coin.

According to the research from Cornerstone Advisors , these point-of-sale short-term installment loans with low credit amounts have been increasing in popularity during recent years for retail purchases like clothing, household goods, electronics, and more.

Sign up for consumercredit counseling. Reach out to a credit counseling agency. This requires you to apply for a new fixed-rate, low-interest loan – you use the new loan to pay off your current debt, then pay back the new loan over a set term. The complication is that you typically need good credit.

WHAT THIS MEANS, FROM LORI QUINN OF MESSER STRICKLER BURNETTE: Plaintiff brought a putative Class Action against Oliphant in State Court that was removed to Federal Court alleging violations of the Fair Debt Collection Practices Act, Maryland Consumer Debt Collection Act and Mary Maryland’s Consumer Protection Act.

If you want to lose the plastic altogether, think about applying for a debt consolidation loan. Go for a loan with a low interest. Then, avoid putting any more money on credit cards until you’ve paid off most of the consolidation loan. . Compare Rates on Debt Consolidation Loans. Check Your Credit Score.

Early in the COVID-19 pandemic, FICO data scientists discovered that the FICO® Resilience Index was a strong predictor of the likelihood that consumers were receiving loan accommodations such as payment deferrals and forbearances following implementation of the CARES Act. .

How Might Buy Now, Pay Later Loans Impact FICO® Scores? Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. consumercredit files. NicholetteLarsen@fico.com. Tue, 03/23/2021 - 22:16. by Suna Hafizogullari. expand_less Back To Top. Mon, 06/20/2022 - 15:00.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York, leading to a shift in consumer spending for 2024. And we’re seeing consumers often need help to organize the different debts.”

Add these all together and the financial outlook for consumers, especially those in debt, is scary. For one, the consumercredit market is looking strong with signs of expansion, specifically, originations for credit cards and personalloans are increasing. But there are silver linings, as well.

consumercredit card debt has increased to nearly $1 trillion. Credit card balances jumped more than $60 billion over Q4 2022, lifting the total amount of U.S. credit card debt to an all-time high of $986 billion, the report found. If successful, many consumers will see their overall debt burden decrease.

As lenders acknowledge the need for alternative credit data, companies are finding innovative ways to track non-traditional payments without requiring consumers to borrow money or use a credit card. Rental agencies and alternative credit providers use the data to screen applicants and establish consumercredit scores.

TransUnion ( NYSE: TRU ) confirmed that consumercredit activity keeps rising from the COVID-19 pandemic lows, but some areas like automobile loans (subprime) performance have lagged. Matt Komos , VP of Research and Consulting at TransUnion, stated: “On the surface, the consumercredit market is performing quite well.

The just recently released Federal Reserve ConsumerCredit-G.19 consumercredit outstanding has reached historic levels; outstanding consumercredit is now at $4.7 In August, consumercredit increased at a seasonally adjusted annual rate of 8.3 19 report shows that U.S. The post U.S.

As shown in figure 3, recent missed payments are up most notably on bankcards , followed by auto loans. During the first year of the pandemic, the combination of government stimulus programs such as the CARES Act and payment accommodation programs offered by lenders helped millions of consumers stave off missed payments. See all Posts.

“Proponents believe a cap on fees and interest would help consumers, especially subprime borrowers with less-than-perfect credit histories, by limiting what they pay on payday loans and other less-regulated short-term credit. For a loan product to be sustainable, depository institutions must be able to recover costs.”.

These in-depth insights can help lenders expertly manage credit risk in these uncertain times, while continuing to make competitive credit offers to consumers. .

Credit card balances reached a record-setting $866 billion in the third quarter of last year, which represents a year-over-year increase of 19%. Credit balances reached a record-setting $866 billion in the third quarter of last year – and they are expected to keep climbing, the report from TransUnion said.

It shows lenders that you have a history of responsibly managing credit and can qualify you for better loan terms and lower interest rates. Few numbers are as important as your credit scores. Lenders use them to determine if you qualify for auto loans, home loans, credit cards and other products.

The Federal Trade Commission recommends finding a reputable credit counseling organization that uses certified counselors trained in consumercredit and debt management. Unsecured debts, such as credit cards, store cards and personalloans, can be part of your DMP. Student loans aren’t covered, either.

While the markets are pricing these into forecasts , consumers will feel them more acutely in a number of ways. And opening a new credit card line may prove difficult – many lenders are or will be changing their strategies to stave off the looming threat of…. Missed payments on certain loans are already on the rise.

Credit Card, PersonalLoan Delinquencies Expected to Surge in 2023. The company’s 2023 ConsumerCredit Forecast released Wednesday projects serious credit card delinquencies will climb to 2.6% The number of “buy now, pay later” loans grew more than tenfold during the pandemic, a U.S.

This applies to unpaid debts such as: Unsecured debts: These are debts not tied to a specific asset, like credit card debt, medical bills, or personalloans. Overdue child support or alimony payments Unpaid taxes Federal laws, like the ConsumerCredit Protection Act (CCPA) , limit the amount of your wages that can be garnished.

It requires collectors to obtain prior express consent before making automated or prerecorded calls to consumers’ cell phones. Fair Credit Reporting Act (FCRA): The FCRA governs the accuracy, privacy, and use of consumercredit information. It also restricts unsolicited text messages and fax communications.

Credit card delinquency rates also rose across the board, according to the New York Fed, but especially among millennials, or borrowers between the ages of 30 and 39, who are burdened by high levels of student loan debt. The average annual percentage rate is now more than 20% — also an all-time high.

In the last 30 years, the Fair Isaac and Company, better known as FICO, changed the way the lenders evaluate consumer applications. The FICO score, introduced in 1989, uses consumercredit payment history, to create a proprietary three-digit number predicting future repayment risk. Which Lenders Use the FICO XD. Final Thoughts.

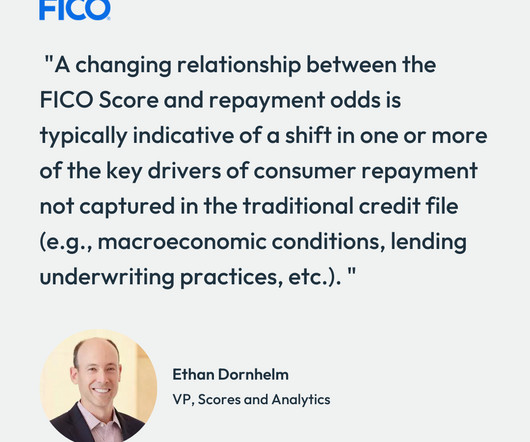

What the FICO Score is not designed to do is provide a specific, fixed estimate of credit risk; we know from tracking the scores over three-plus decades that the relationship between the FICO Score and consumers’ likelihood of loan repayment can and does shift over time and across economic and financial cycles. originations).

Information and data continue to be key tools at our disposal to better understand the dynamics of the last couple of years, and better navigate what lies ahead for the Canadian consumercredit environment.

Citi also offers personalloans, lines of credit, and mortgages, which can prompt a hard inquiry. If you are overwhelmed by dealing with negative entries on your credit report, we suggest you ask a professional credit repair company for help. How Does a CBNA Sioux Falls Hard Inquiry Affect Your Credit?

Citi also offers personalloans, lines of credit, and mortgages which can prompt a hard inquiry. If you are overwhelmed by dealing with negative entries on your credit report, we suggest you ask a professional credit repair company for help. How Does a CBNA Sioux Falls Hard Inquiry Affect Your Credit?

It has taken actions to collect data on a number of new industries, including debt relief and earned wage access providers, and has filed a cease-and-desist order against a student loan debt relief company charging borrowers exorbitant fees for the false promise of getting their student debt wiped.

A collection account will lower your credit score and can generally stay on your credit report for up to seven years. Often, a collection entry will even keep you from getting a mortgage or securing an auto loan, which is why it’s important to do all you can to remove collections from your credit report quickly.

.” Between the lines: The stabilization in delinquency rates reflects improved household budgets, with 63% of consumers reporting finances as “as planned or better” in late 2024. Learn more.

With inflation proving more sticky than policymakers had hoped and uncertainty around how the new administrations policies might affect it, it may take longer for people to see lower interest rates on their mortgages, car loans and credit card balances, which could prove challenging to household budgets.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content