This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

million Americans have studentloan debt, which totals over $1.7 If you owe tens of thousands of dollars in studentloan debt, you’re not alone. According to the Federal Reserve’s ConsumerCredit report, 43.5 million Americans have some form of federal or private studentloan debt. 2021 37 10.2

To help studentloan borrowers avoid scams, NerdWallet is rounding up information on legitimate sources of help, like this one. Organization: American ConsumerCredit Counseling. The article American ConsumerCredit Counseling Review: StudentLoan Help originally appeared on NerdWallet.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York , leading to a shift in consumer spending for 2024. And we’re seeing consumers often need help to organize the different debts.”

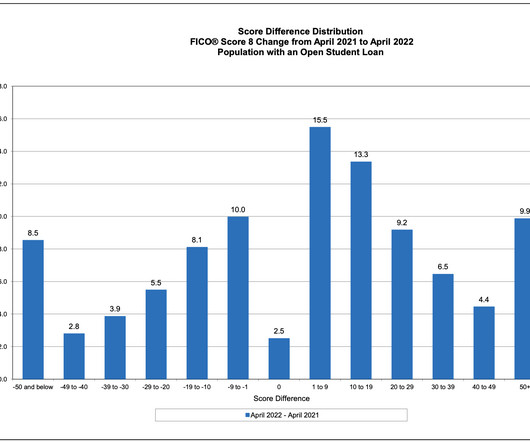

Home Blog FICO Are StudentLoan Holders at Risk as Deferments Expire? Here we present results of our research into FICO® Score dynamics for holders of studentloan debt between 2021 and 2022, to give an indication of key factors that seem to accompany large decreases in the FICO Scores of this population.

On June 14, Nevada Governor Joe Lombardo signed into law AB 332 , An Act Relating to Student Education Loans, requiring, among other things, studentloan servicers to be licensed by the Commissioner of Financial Institutions and regulating certain conduct of the servicers towards borrowers.

On September 29, the Consumer Financial Protection Bureau (CFPB or Bureau) released a special edition of its Supervisory Highlights , focusing on studentloan servicing. It’s time to open up the books on institutional student lending to ensure all students with private studentloans are not harmed by illegal practices.”.

consumercredit card debt has increased to nearly $1 trillion. Credit card balances jumped more than $60 billion over Q4 2022, lifting the total amount of U.S. credit card debt to an all-time high of $986 billion, the report found. If successful, many consumers will see their overall debt burden decrease.

On November 17, the Consumer Financial Protection Bureau (CFPB) announced it is seeking public comment on its proposal to develop a new data set to better monitor the auto loan market. Because studentloans are largely administered by the federal government, we know more about them too.

If you want to lose the plastic altogether, think about applying for a debt consolidation loan. Go for a loan with a low interest. Then, avoid putting any more money on credit cards until you’ve paid off most of the consolidation loan. . Compare Rates on Debt Consolidation Loans. Check Your Credit Score.

This week, the CFPB introduced a new research tool, its ConsumerCredit Trend Tool. According to the CFPB, the new tool’s purpose is to track originations of various consumercredit products. For now, the tool will focus on four credit products: mortgage, studentloan, credit cards and auto loans.

According to the research from Cornerstone Advisors , these point-of-sale short-term installment loans with low credit amounts have been increasing in popularity during recent years for retail purchases like clothing, household goods, electronics, and more.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York, leading to a shift in consumer spending for 2024. And we’re seeing consumers often need help to organize the different debts.”

And another factor might make the increases more painful for some consumers: The pause on federal studentloan payments ended Sept. Studentloan balances have already begun accruing interest again, and soon, borrowers will be expected to start making regular payments.

Early in the COVID-19 pandemic, FICO data scientists discovered that the FICO® Resilience Index was a strong predictor of the likelihood that consumers were receiving loan accommodations such as payment deferrals and forbearances following implementation of the CARES Act. .

When you borrow money, whether through a revolving account, like credit cards , or an installment account, like an auto loan or studentloan , the information is gathered by the credit bureaus. The data the bureaus keep in your credit files is the date used to calculate your credit scores.

In addition, the Symposium welcomes discussion over the recent decision by the Uniform Law Commission to address debt collection efforts by third-party debt collectors or buyers based on default judgments.

trillion, according to the Federal Reserve Bank of New York’s latest Quarterly Report on Household Debt and Credit. Mortgage and auto loan balances continued climbing, increasing to $12.44 Credit card balances also declined seasonally as expected in Q1 to $1.12 trillion and $1.62 trillion respectively.

ruling that the plaintiff failed to specifically allege facts to support an inference that Navient Corporation and Navient Solutions LLC violated the Fair Credit Reporting Act (FCRA) and the California ConsumerCredit Reporting Agencies Act (CCRAA). Navient Corp.

The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. Credit card balances increased by $45 billion, from $986 billion in Q1 2023 to a series high of $1.03 Other balances, which include retail cards and other consumerloans, increased by $15 billion.

The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. The New York Fed also issued an accompanying Liberty Street Economics blog post examining growing balances of home equity lines of credit (HELOC). Credit card balances increased by $27 billion to $1.14

The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. The New York Fed also issued an accompanying Liberty Street Economics blog post examining credit card utilization and its relationship with delinquency. Credit card balances decreased by $14 billion to $1.12

Pursuant to its authority under Section 1022(b)(1) of the Dodd-Frank Act, the Consumer Financial Protection Bureau (CFPB) issued an advisory opinion to consumer reporting agencies (CRAs), highlighting their obligation to screen for and eliminate obviously false data from consumers’ credit reports.

It gathers credit reports from the three major credit bureaus and analyzes anonymous consumer data to generate a scoring model specific to each bureau. VantageScore, on the other hand, uses a combined set of consumercredit files, also obtained from the three major credit bureaus, to come up with a single formula.

Credit Risk and FICO Score Trends? And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, such as in the form of rising balances, credit seeking behavior, and eventually for some, missed payments.

On October 11, an automotive management company settled claims by the Department of Justice (DOJ) alleging that the company had violated the False Claims Act by knowingly providing false information in support of its Paycheck Protection Program (PPP) loan forgiveness application. For more information, click here.

Hochul specifically mentioned studentloan servicers who encourage the quickest repayment plans or plans not suitable for the party repaying. In 2023, Hochul signed laws scrubbing all medical debt from consumercredit reports and prohibited wage garnishments for medical debt and liens on primary residences.

Add these all together and the financial outlook for consumers, especially those in debt, is scary. For one, the consumercredit market is looking strong with signs of expansion, specifically, originations for credit cards and personal loans are increasing. But there are silver linings, as well.

Sure, credit-scoring models are complicated (all that algorithm-ing and such). But, when you get right down to it, the secret sauce to building good credit is actually pretty straightforward: Take a whole bunch of on-time loan payments, keep a pinch of debt, stir in some new accounts, and let the thing bake. Open a New Account.

On May 1, the CFPB proposed a rule to implement a congressional mandate to establish consumer protections for residential property assessed clean energy (PACE) loans. PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels.

That’s the headline from a recent NBC News story about the millions of Americans who have deferred payment on mortgages, rent, studentloans and utility bills. 26% of Consumers Have a Third-Party Collection Tradeline on Their Credit Report. “Payment deferrals were a lifeline for millions during Covid.

The Federal Trade Commission recommends finding a reputable credit counseling organization that uses certified counselors trained in consumercredit and debt management. Unsecured debts, such as credit cards, store cards and personal loans, can be part of your DMP. Studentloans aren’t covered, either.

The ConsumerCredit Protection Act caps these types of garnishments. What if the loan company or debt collector has already started the lawsuit? Exceptions apply for things like child support, spousal support, studentloans and some property liens. The lessor of these two amounts applies. Don’t skip court.

It has taken actions to collect data on a number of new industries, including debt relief and earned wage access providers, and has filed a cease-and-desist order against a studentloan debt relief company charging borrowers exorbitant fees for the false promise of getting their student debt wiped.

Just like with consumercredit, debt from a civil judgment must be validated under the Fair Credit Reporting Act. How Long Do Judgments Stay on My Credit Report? Just like consumercredit, court-ordered debt could stay on your credit report up to seven years if you don’t take action to remove it.

Credit card delinquency rates also rose across the board, according to the New York Fed, but especially among millennials, or borrowers between the ages of 30 and 39, who are burdened by high levels of studentloan debt. The average annual percentage rate is now more than 20% — also an all-time high.

It was for a PMSI loan for an outdoor wood burning furnace. I came to learn that FDR mainly only works with credit cards. I also have solar panels with FDR; fortunately for me that is an unsecured loan, so they can help with that one.” – Laura Whipple, 4-star review, TrustPilot. I was not told that by my consultant.

While the markets are pricing these into forecasts , consumers will feel them more acutely in a number of ways. And opening a new credit card line may prove difficult – many lenders are or will be changing their strategies to stave off the looming threat of…. Missed payments on certain loans are already on the rise.

In fact, medical debt is one of the most common types of debt reported on consumercredit reports. According to the Consumer Financial Protection Bureau, consumercredit reports show $88 billion in medical debt as of June 2021. Many Chapter 13 Debtors pay pennies on the dollar back to their unsecured creditors.

Hochul specifically mentioned studentloan servicers who encourage the quickest repayment plans or plans not suitable for the party repaying. In 2023, Hochul signed laws scrubbing all medical debt from consumercredit reports and prohibited wage garnishments for medical debt and liens on primary residences.

On March 30, the Consumer Financial Protection Bureau (CFPB) sanctioned Edfinancial for deceiving studentloan borrowers about their eligibility for Public Service Loan Forgiveness, and the steps they could have taken to obtain loan cancellation.

Federal Activities: On December 16, the Consumer Financial Protection Bureau (CFPB) issued a series of orders to five companies offering “buy now, pay later” (BNPL) credit. The CFPB is concerned about accumulating debt, regulatory arbitrage, and data harvesting in a consumercredit market already quickly changing with technology.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. In reviewing the market for potential consumer harm, the report presents the latest research on consumer card use, cost, and availability.

In a letter sent to the leaders of the House and Senate , CUNA President/CEO Jim Nussle stated his objections to section 403 of the bill, which would amend the Fair Credit Reporting Act to prohibit credit scoring models from treating certain medical debt information on consumers’ credit report as a negative factor.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content