This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

On September 19, the Consumer Financial Protection Bureau (CFPB) released a blog post , exploring the potential relationship between rising car prices and changes in auto loan performance. For example, auto loans for consumers with deep subprime credit scores were 2.4%

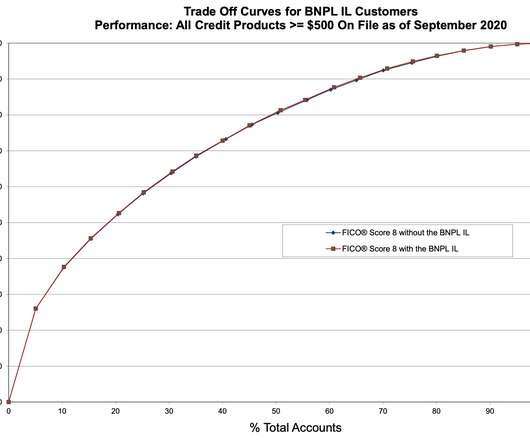

How Might Buy Now, Pay Later Loans Impact FICO® Scores? Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. consumercredit files. NicholetteLarsen@fico.com. Tue, 03/23/2021 - 22:16. by Suna Hafizogullari. expand_less Back To Top. Mon, 06/20/2022 - 15:00.

So credit repair, consumercredit and credit bureaus—they’re all tied together. To understand why they’re so important, you might want to learn a bit more about the history of credit scores and repair. Luckily, we’ve compiled everything you need to know about the history of the credit repair industry.

As part of the settlement, the entities will forgive $223,685 in loans, pay $33,991 in restitution, and pay $33,000 in civil penalties and costs to the state. As part of the settlement, the entities will forgive $223,685 in loans, pay $33,991 in restitution, and pay $33,000 in civil penalties and costs to the state.

Quicken Loans Inc. , –– Fed Appx. ––, 2021 WL 2799939 (Jul. Section 1681(g) of the FCRA requires a lender to provide a CSD to a consumer whenever their consumercredit score is utilized in connection with a loan application “initiated or sought by a consumer.” In Ajomale v.

Individuals, like you or I, have a credit history which determines our eligibility for home and car loans, ability to rent an apartment, obtain insurance, find a job and even maintain long-term romantic relationships. This doesn’t mean they have a bad credit history, because some of them may pay all their bills on time.

A recent settlement between the Federal Trade Commission (FTC) and a lead generator provides new insight into the FTC’s enforcement of sensitive personal data collection and sales under the Fair Credit Reporting Act (FCRA) and the agency’s Section 5(a) authority.

In keeping with Federal Trade Commission rules , Freedom Debt Relief doesn’t charge upfront fees. It was for a PMSI loan for an outdoor wood burning furnace. I came to learn that FDR mainly only works with credit cards. Focused on protecting and helping consumers. You can use several methods: Consumercredit counseling.

Sure, credit-scoring models are complicated (all that algorithm-ing and such). But, when you get right down to it, the secret sauce to building good credit is actually pretty straightforward: Take a whole bunch of on-time loan payments, keep a pinch of debt, stir in some new accounts, and let the thing bake.

The Federal Trade Commission recommends finding a reputable credit counseling organization that uses certified counselors trained in consumercredit and debt management. Unsecured debts, such as credit cards, store cards and personal loans, can be part of your DMP. Student loans aren’t covered, either.

Your credit history and scores can impact your entire life. Whether or not you can get a loan—and at what interest—often depends on your credit. Credit can also play a role in whether you can rent the apartment you want, get a credit card for use in daily life or enjoy a great deal on car insurance.

In particular, the minimum loan size for three Main Street facilities available to for-profit and nonprofit borrowers was reduced from $250,000 to $100,000, and the fees were adjusted to encourage the provision of these smaller loans. The legislation would benefit banks and credit unions with assets under $15 billion.

On January 20, 2023, California Attorney General Rob Bonta submitted a letter to the CFPB agreeing with its preliminary determination that California’s Commercial Financing Disclosures Law (CFDL) is not preempted by TILA because the CFDL only applies to commercial financing and not to consumercredit transactions within the scope of TILA.

The Federal Trade Commission (FTC) took action against a firm that used a government website as part of its scheme connected with consumercredit reports. The complaint seeks both civil penalties and consumer redress, according to the news release. Source- site.

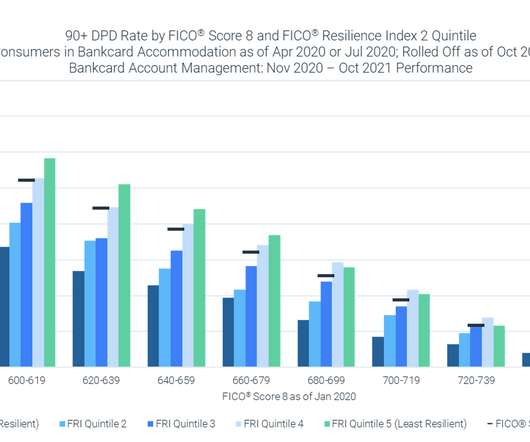

In the early months of the COVID-19 pandemic, FICO found that the FICO® Resilience Index was a strong predictor of the likelihood that a consumer would receive a loan accommodation (payment deferral, forbearance, etc.) In today's market conditions, we can observe the credit behavior of consumers who have exited these accommodations.

It marks the highest fine ever issued to a lender for what it deemed a breach of consumercredit rules. But more tellingly, the penalty related to the mistreatment of business and personal customers who fell behind on credit card and loan payments between 2014 and 2018 – well before many of us had even heard of COVID-19.

We break this down in our article: “ What Exactly is Credit Repair & How it Works,” but the short answer is that credit repair is the process of reviewing, disputing, and negotiating negative items on your credit report that may negatively impact the credit risk tier you’re in and the loans and interest rates you qualify for.

FICO® Score At 716, Indicating Improvement In ConsumerCredit Behaviors Despite Pandemic. Ethan Dornhelm wrote: The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of credit risk. Fewer consumers are actively seeking credit.

For example, the bill distinguishes a “digital asset” from a “digital commodity,” empowering the Securities and Exchange Commission (SEC) to regulate the former and the Commodity Futures Trading Commission (CFTC) to regulate the latter. On July 26, the CFPB published a blog focused on consumercredit scores.

You may have a CBNA entry from Community Bank NA if you have worked with them to apply for a loan or line of credit. This would refer to a hard inquiry into your credit history before you are approved. The Federal Trade Commission has a website that consumers can use to document and report instances of identity theft.

District Court for the Southern District of Texas granted motions filed by three groups of trade association intervenors to extend the court’s existing injunction against the CFPB’s enforcement of its final rule under § 1071 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Final Rule) to cover all small business lenders nationwide.

On October 11, the Federal Trade Commission (FTC) announced a new proposed rule to prohibit junk fees, which are hidden and bogus fees that can harm consumers and undercut honest businesses. The FTC has estimated that these fees can cost consumers tens of billions of dollars per year in unexpected costs.

I want to make sure my credit report is accurate so I can at least qualify for loans.’. So they started looking at their credit report more, and they found more mistakes,” he said. But a trade group that represents the credit reporting companies questioned the reliability of the CFPB’s complaint reports.

The blog post posited that closing costs significantly impact a borrower’s financial commitment and, potentially, monthly payments and identified a “noticeable increase” in closing costs, with median total loan expenses on home purchase loans increasing by 21.8% between 2021 and 2022. For more information, click here.

On May 1, the CFPB proposed a rule to implement a congressional mandate to establish consumer protections for residential property assessed clean energy (PACE) loans. PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. In reviewing the market for potential consumer harm, the report presents the latest research on consumer card use, cost, and availability.

Federal Activities: On December 16, the Consumer Financial Protection Bureau (CFPB) issued a series of orders to five companies offering “buy now, pay later” (BNPL) credit. The CFPB is concerned about accumulating debt, regulatory arbitrage, and data harvesting in a consumercredit market already quickly changing with technology.

The CFPB also released several reports shining a light on factors that may influence fair access to credit, including how medical debt affects tens of millions of consumers’ credit profiles, how people in under-resourced rural areas struggle to access financial services, and the challenges faced by justice-involved individuals and families.

On November 9, the Department of Education (DOE) announced its plan to implement an oversight strategy of federal student loan servicers that provides several pathways for identifying problems that can harm borrowers, in real-time. For more information, click here. For more information, click here. For more information, click here.

consumercredit payment holidays to borrowers so far. s main announcements on business taxation: The Chancellor is banking on the volumes of consumer savings squirrelled away in deposits to be unlocked and help get things moving ? No-Interest Loans? an alternative to relying on high-cost credit? Chancellor?s

On January 26, the Securities and Exchange Commission (SEC) rejected Cboe BZX Exchange’s (BZX) request to list and trade Ark 21Shares, the proposed spot-Bitcoin exchange traded fund (ETF) managed by asset managers ARK Investment Management and 21Shares (collectively hereinafter, the “trust). For more information, click here.

On June 8, the Commodities Futures Trading Commission (CFTC) obtained a default judgment against a decentralized autonomous organization (DAO) Ooki Dao in the U.S. with operating its crypto asset trading platform as an unregistered national securities exchange, broker, and clearing agency. For more information, click here.

On June 15, the Consumer Financial Protection Bureau (CFPB) issued an update about its December 2021 market monitoring inquiry into Buy Now, Pay Later (BNPL) — a short-term, no-interest consumercredit product that has become nearly ubiquitous at the point of purchase online and, increasingly, in brick-and-mortar stores.

To help you keep abreast of relevant activities, below find a breakdown of some of the biggest events at the federal and state levels to impact the Consumer Finance Services industry this past week: Federal Activities. On August 5, President Biden signed the COVID-19 Economic Injury Disaster Loan Fraud Statute of Limitations Act ( R.7334

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. Since businesses are not taxed on the proceeds of a forgiven PPP loan, the expenses are not deductible. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The 2020 review found that credit risk for large, syndicated loans has increased over the last year.

To help you keep abreast of relevant activities, below find a breakdown of some of the biggest events at the federal and state levels to impact the Consumer Finance Services industry this past week: Federal Activities. On October 21, the Eighth Circuit temporarily blocked President Joe Biden’s student loan forgiveness program.

On November 2, the Consumer Financial Protection Bureau (CFPB) released a blog post, exploring the potential impact of student loan payment reinstatement. The CFPB found that student loan borrowers are increasingly likely to struggle once their monthly student loan payments are reinstated.

To help you keep abreast of relevant activities, below find a breakdown of some of the biggest events at the federal and state levels to impact the Consumer Finance Services industry this past week: Federal Activities. million to consumers and pay a $500,000 civil penalty for deceiving consumers with false claims about their services.

On October 13, the CFPB, the Federal Reserve Board, and the Office of the Comptroller of the Currency (OCC) announced that the 2023 threshold for exempting loans from special appraisal requirements for higher-priced mortgage loans will increase from $28,500 to $31,000. For more information, click here. For more information, click here.

PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels. On April 27, Federal Trade Commission (FTC) Chair Lina M. Senate Committee on Banking held a full committee hearing, titled “Oversight of the Credit Reporting Agencies.”

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. House of Representatives that seeks to amend the Fair Credit Reporting Act to exclude COVID-19-related evictions from consumers’ credit reports.

Department of the Treasury (Treasury) launched an inquiry into specialty financial products, such as medical credit cards and installment loans, that consumers can use to pay for medical care. The CFPB further alleged that the defendants made guarantees about lowering consumers’ credit card interest rates.

20 tapped Uejio, previously the Consumer Financial Protection Bureau’s chief strategy officer, to run the agency until his nominee for permanent director, Rohit Chopra, is confirmed. Chopra is currently a member of the Federal Trade Commission. President Biden on Jan. The two share many of the same priorities, Cordray said.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content