This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York , leading to a shift in consumer spending for 2024.

“Amounts owed” comprises some 30% of the overall FICO® Score calculation and is heavily weighted towards credit card balances and utilization so the observed reduction in credit card debt is helping to drive scores upwards. Fewer consumers are actively seeking credit. There has been a 12.1% The Other Side of the Coin.

As part of the settlement, the entities will forgive $223,685 in loans, pay $33,991 in restitution, and pay $33,000 in civil penalties and costs to the state. and its related entities provided personalloans to consumers to finance taxes and down payments associated with vehicle purchases.

This net was driven by decreases in delinquent first mortgage and unsecured personalloan balances, which were offset by increases in delinquent bankcard balances and on a dollar basis in delinquent second mortgages.

WHAT THIS MEANS, FROM LORI QUINN OF MESSER STRICKLER BURNETTE: Plaintiff brought a putative Class Action against Oliphant in State Court that was removed to Federal Court alleging violations of the Fair Debt Collection Practices Act, Maryland Consumer Debt Collection Act and Mary Maryland’s Consumer Protection Act.

BNPL loans are cited as a potential driver of greater financial inclusion, both in terms of consumer access to the BNPL loan themselves, as well as access to credit products that could enable unbanked and underbanked consumers to establish (or re-establish) their credit histories with one or more of the Consumer Reporting Agencies (CRAs). .

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York, leading to a shift in consumer spending for 2024.

Sign up for consumercredit counseling. Reach out to a credit counseling agency. Many credit card lenders allow you to transfer personalloans, and other types of debt, not just your credit card balance. The complication is that you typically need good credit.

You could also: Put together a realistic debt-repayment plan Increase your income with a better-paying job, or ask your boss for a raise Ask your lenders for a lower interest rate Consider consumercredit counseling Concentrate on one debt at a time to avoid feeling overwhelmed. >> Download our free budget template to get started.

Add these all together and the financial outlook for consumers, especially those in debt, is scary. For one, the consumercredit market is looking strong with signs of expansion, specifically, originations for credit cards and personalloans are increasing. But there are silver linings, as well.

TransUnion ( NYSE: TRU ) confirmed that consumercredit activity keeps rising from the COVID-19 pandemic lows, but some areas like automobile loans (subprime) performance have lagged. Matt Komos , VP of Research and Consulting at TransUnion, stated: “On the surface, the consumercredit market is performing quite well.

As lenders acknowledge the need for alternative credit data, companies are finding innovative ways to track non-traditional payments without requiring consumers to borrow money or use a credit card. Rental agencies and alternative credit providers use the data to screen applicants and establish consumercredit scores.

The just recently released Federal Reserve ConsumerCredit-G.19 consumercredit outstanding has reached historic levels; outstanding consumercredit is now at $4.7 In August, consumercredit increased at a seasonally adjusted annual rate of 8.3 19 report shows that U.S.

In reality, its impact would extend far beyond payday lenders to the broader consumercredit market to cover affordable small dollar loans (including “accommodation” loans) that depository institutions are being encouraged to offer, credit cards, personalloans, and overdraft lines of credit,” the letter reads. “As

These in-depth insights can help lenders expertly manage credit risk in these uncertain times, while continuing to make competitive credit offers to consumers. .

Consumers trying to make ends meet have continued turning to credit cards and other credit types to bridge the income to expense gap. consumercredit card debt has increased to nearly $1 trillion. Credit card balances jumped more than $60 billion over Q4 2022, lifting the total amount of U.S.

Credit card balances reached a record-setting $866 billion in the third quarter of last year, which represents a year-over-year increase of 19%. Credit balances reached a record-setting $866 billion in the third quarter of last year – and they are expected to keep climbing, the report from TransUnion said.

We found that FICO® Resilience Index continues to be a strong predictor of the presence of loan accommodations in place as of October 2020 – representing a mix of “long haul” accommodations by mortgage lenders and newer short-term accommodations allowed on bankcard, auto finance and personalloan accounts.

It requires collectors to obtain prior express consent before making automated or prerecorded calls to consumers’ cell phones. Fair Credit Reporting Act (FCRA): The FCRA governs the accuracy, privacy, and use of consumercredit information. It also restricts unsolicited text messages and fax communications.

Information and data continue to be key tools at our disposal to better understand the dynamics of the last couple of years, and better navigate what lies ahead for the Canadian consumercredit environment.

For many of these consumers, this decrease has likely been driven by the inverse of the trends that drove the national average FICO® Score up during the first year of the pandemic: a slow-down in economic growth , surging inflation, a decrease in household saving rates and ramping down of government stimulus programs. Ethan has a B.S.

Credit Card, PersonalLoan Delinquencies Expected to Surge in 2023. The company’s 2023 ConsumerCredit Forecast released Wednesday projects serious credit card delinquencies will climb to 2.6% TransUnion said delinquency rates for those categories have not reached that level since 2010.

The Federal Trade Commission recommends finding a reputable credit counseling organization that uses certified counselors trained in consumercredit and debt management. Unsecured debts, such as credit cards, store cards and personalloans, can be part of your DMP. Student loans aren’t covered, either.

This applies to unpaid debts such as: Unsecured debts: These are debts not tied to a specific asset, like credit card debt, medical bills, or personalloans. Overdue child support or alimony payments Unpaid taxes Federal laws, like the ConsumerCredit Protection Act (CCPA) , limit the amount of your wages that can be garnished.

How Might Buy Now, Pay Later Loans Impact FICO® Scores? Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. consumercredit files. But on the other hand, adding positive BNPL payment data in the consumercredit file could help the FICO® Score.

Still, consumercredit scores have remained high, helped by a strong labor market and cooling inflation, along with the removal of certain medical collections data from consumercredit files, recent reports show. “My rent is going up, so even though all my bills are paid, sometimes I’m living paycheck to paycheck.”

A hike in the federal interest rate prompts a jump in the Bank Prime Loan Rate ( prime rate ), the credit rate that banks offer to their most credit-worthy customers and off of which they base other forms of consumercredit like mortgages and consumerloans. We all knew this was coming.

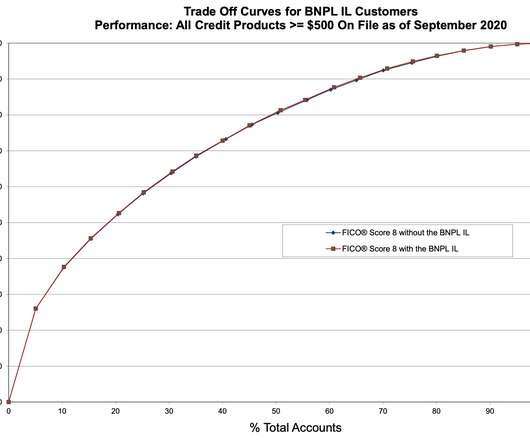

auto, mortgage, personalloan) and lifecycles (e.g., In other words, even as the relationship between odds of repayment and score has shifted, the score has retained its powerful ability to distinguish repayment likelihood between low and high scoring consumers. originations).

Although a prime score isn’t the highest credit score you can have—credit scores generally range from 300 to 850—it’s high enough to help you qualify for many loans and credit cards. Additional Score Categories Prime is just one of the five categories used to classify consumercredit scores in the context of lending.

In the last 30 years, the Fair Isaac and Company, better known as FICO, changed the way the lenders evaluate consumer applications. The FICO score, introduced in 1989, uses consumercredit payment history, to create a proprietary three-digit number predicting future repayment risk. Which Lenders Use the FICO XD.

The DFPI continues to experience and respond to a more than 40 percent increase in consumer complaints, calls and inquiries since the onset of COVID-19 in the state. The DFPI is tracking all COVID-19 related complaints and reporting harmful emerging consumer trends to the enforcement division for investigation.

Citi also offers personalloans, lines of credit, and mortgages, which can prompt a hard inquiry. If you are overwhelmed by dealing with negative entries on your credit report, we suggest you ask a professional credit repair company for help. File a Dispute with the Credit Bureaus. Balance transfers.

Citi also offers personalloans, lines of credit, and mortgages which can prompt a hard inquiry. If you are overwhelmed by dealing with negative entries on your credit report, we suggest you ask a professional credit repair company for help. File a Dispute with the Credit Bureaus. Balance transfers.

When you apply for new credit, lenders know your old lenders lost money on your accounts. So a collection account will have a negative impact on your ability to apply for new credit — whether it’s a mortgage, a major credit card, or a personalloan. Wilshire ConsumerCredit. TrueAccord.

.” Between the lines: The stabilization in delinquency rates reflects improved household budgets, with 63% of consumers reporting finances as “as planned or better” in late 2024. Learn more.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content