This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

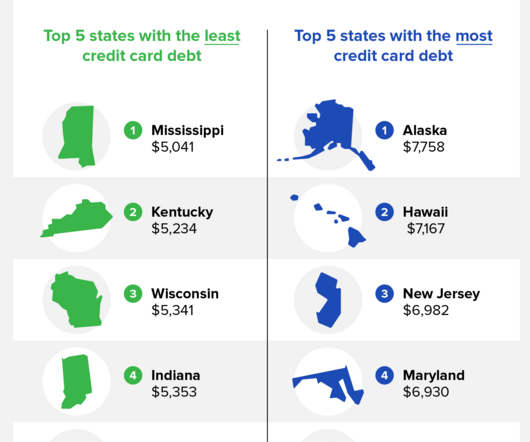

The average household creditcarddebt in America is $9,654, and the states with the largest amount of creditcarddebt are Alaska, Hawaii, and New Jersey. Between the first quarters of 2022 and 2023, The Federal Reserve Bank of New York reported that the creditcarddebt in America rose by $145 billion.

The average household creditcarddebt in America is $9,260, and the states with the largest amount of creditcarddebt are Alaska, Hawaii, and New Jersey. Between the first and final quarter of 2022 , TransUnion® reported that the average American’s creditcarddebt rose roughly $400 per person.

Creditcarddebt has plunged — but what if you’re still up to your neck? Creditcarddebt has fallen during the pandemic, with figures from creditbureau Experian showing the average debt dropped from $6,194 in 2019 to $5,313 in 2020. Source: site. Who’s dealing with the heaviest load?

Creditcard balances reached a record-setting $866 billion in the third quarter of last year, which represents a year-over-year increase of 19%. A Consumer Pulse study conducted by the creditbureau found that more than half of Americans expressed confidence about their financial health in 2023.

High CreditCard Balances The amount of creditcarddebt you have compared to your credit limits, known as your credit utilization ratio, is another crucial factor in calculating your credit score. Solution: Aim to keep your creditcard balances low relative to your credit limits.

and globally -- making access to credit more efficient and objective, which has continued into the present day. FICO® Scores are dynamic and evolve as changes in consumer behavior are reflected in the underlying creditbureau data housed and managed by the three primary U.S. consumer reporting agencies (CRAs). in April 2022.

Rent Bureau , now owned by the creditbureau Experian, electronically compiles rental data from property management companies and individual landlords. Rental agencies and alternative credit providers use the data to screen applicants and establish consumer credit scores.

Due to the fact that not all companies report to all three creditbureaus, there are often differences in the information retained by each creditbureau. Credit scoring companies like FICO rely primarily on the information contained in the credit report, which can result in a different credit score for each creditbureau.

Even though all these companies review credit to determine deposit requirements, they do not report on-time payments to the creditbureau because it is not considered debt. To address these disparities, some lenders now accept credit scores like the FICO XD , which uses alternative data.

Mix in the fact that many consumers – enabled, in part, by historic levels of savings at least partly driven by government stimulus such as enhanced unemployment benefits – have shifted their focus to paying down their creditcarddebt, and the result is a greater than 10% decrease in the average creditcard balance and utilization of the U.S.

For this report, the CFPB used consumer responses to the 2022 Making Ends Meet survey as well as an anonymized sample of creditbureau records. However, the report concluded by noting that the majority of BNPL users have access to traditional credit.

Additionally, research examining the first several months of the pandemic showed that “delinquencies as reported in creditbureau data declined, creditcarddebt fell even for financially vulnerable consumers, bank account balances rose, and survey-based measures of financial conditions rose.”.

There isn’t a right or wrong answer regarding how many creditcards somebody should have — it all depends on your money management skills and finances. Some people may be able to manage two creditcards, while others may be comfortable with 10 or more. Is It Good to Have Multiple CreditCards?

More importantly, will my existing debts impact my credit score in a new country? From renting a house to applying for creditcards, credit score plays a major role in availing basic amenities in a new country. I was worried if my credit score and creditcarddebts back home would hurt my credit score abroad.

Unfortunately, holiday creditcarddebt lingers far longer than leftover turkey. If you don’t—or can’t—repay holiday debt promptly, it’ll accumulate over time. How much debt does the average person owe? . In 2019, shoppers in the US spent 3.4% more than they did in 2018.

But if you have a valid reason, such as needing a car or money for college, a small loan in your name can help you build credit. As with creditcards, loans only build a good credit history if you pay them on time every month. You also want to ensure your creditor reports payments to the creditbureau.

A closer examination of key credit dimensions that comprise a consumer’s FICO Score provides key insights into the FICO® Score trends observed. Comparing Canadian creditbureau data between April 2021 to April 2020, we saw a notable decrease in missed payments.

Monitoring your credit is one of the best ways to learn what will positively or negatively impact your scores. You can check your credit report for free annually with each major creditbureau. As you review your report, look for any negative or inaccurate information that could be screwing up your credit.

Utilization measures how much revolving debt (typically this is creditcarddebt) you have compared to your total credit limit. Balance and credit limit errors may artificially inflate your utilization ratio, making it more difficult to qualify for loans and creditcards.

However, skipping a payment before getting an approved forbearance will result in a delinquency reported to the creditbureau. You increased creditcard spending in a manner not typical of your prior spending history. In most cases, lenders continue to report the account as current.

Contacting the company by phone is the only way to get help, which typically includes the following: waived payments, interest, and penalties, along with suspended creditbureau reporting. In some cases, the company could extend the credit line. However, aid is not automatic or uniform. About Titan Consulting Group.

The creditbureau Experian® describes compound interest as “when interest gets added to the principal amount invested or borrowed, and then the interest rate applies to the new (larger) principal.” Once you have minimal debt, you can create a budget to see how much you can invest each month.

Correct Any Errors on Your Credit Reports First When you review your credit situation, order your credit reports from all three major bureaus. Look for any inaccurate information, particularly any error that might be hurting your credit, and dispute it with the creditbureau.

On May 1, the Federal Trade Commission (FTC) announced a permanent ban from debt relief telemarketing for operators of debt relief scam. The FTC charged the defendants with taking tens of millions of dollars from people by falsely promising to eliminate or substantially reduce their creditcarddebt.

You can combine creditcarddebt, car finance, personal loans, student loans, medical bills, payday loans, and other types of unsecured debt. But is debt consolidation a good idea for you? Dispute negative items : If you notice any mistakes on your credit report, complain to the relevant creditbureau.

Or they may unintentionally sell it to criminal gangs, which then rack up thousands of pounds of fraudulent creditcarddebt. Cross-border fraud is also exacerbated in the UK, EU and Middle East by a lack of cross-border creditbureau facilities. Both of these crimes are first-party fraud.

Making your payments on time is the biggest factor impacting your credit score. Paying a bill 30 days late or later can drop your credit score as much as 100 points. Late payments are not reported to the CreditBureau until they are 30 days past due, which gives you time to pay them off though generally with a late fee.

consumers had on average $6,004 in creditcarddebt, down from an average of $6,934 back in January 2020. A reduction in amounts owed (30% of the FICO® Score calculation), and especially the amount of creditcard limits being used can yield measurable gains in a consumer’s FICO® Score.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content