This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

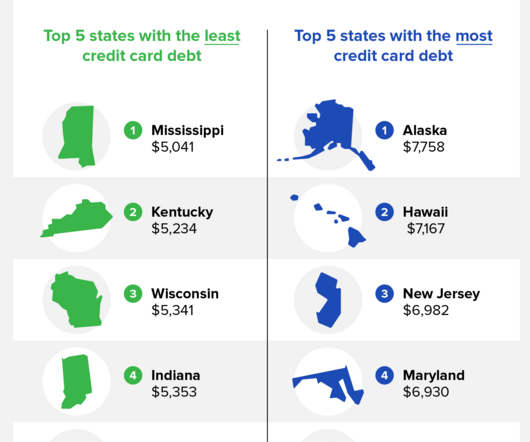

The average household creditcarddebt in America is $9,654, and the states with the largest amount of creditcarddebt are Alaska, Hawaii, and New Jersey. Between the first quarters of 2022 and 2023, The Federal Reserve Bank of New York reported that the creditcarddebt in America rose by $145 billion.

The average household creditcarddebt in America is $9,260, and the states with the largest amount of creditcarddebt are Alaska, Hawaii, and New Jersey. Between the first and final quarter of 2022 , TransUnion® reported that the average American’s creditcarddebt rose roughly $400 per person.

Creditcarddebt has plunged — but what if you’re still up to your neck? Creditcarddebt has fallen during the pandemic, with figures from creditbureau Experian showing the average debt dropped from $6,194 in 2019 to $5,313 in 2020. Source: site. Who’s dealing with the heaviest load?

More importantly, will my existing debts impact my credit score in a new country? From renting a house to applying for creditcards, credit score plays a major role in availing basic amenities in a new country. I was worried if my credit score and creditcarddebts back home would hurt my credit score abroad.

It contains data on your current and past debts, payment history, residential history and other facts. This data is supplied by lenders, creditors and businesses where you have accounts. The information contained in your credit report determines your credit score. Monitor Your Credit Report and Credit Score.

You can request your free credit report at annualcreditreport.com , but if you want to view your credit score, you will need to pay an additional fee. In response to pressure from the CFPB (Consumer Financial Protection Bureau), most banks and creditcard companies now offer free consumer credit scores as an account benefit.

It contains data on your current and past debts, payment history, residential history and other facts. This data is supplied by lenders, creditors and businesses where you have accounts. The information contained in your credit report determines your credit score. Keep It Simple for Now.

Account errors: If someone steals your identity, your credit report may list accounts you never opened. Creditors may also make errors when reporting payment dates and payment amounts. You may even see the same debt listed more than once. It’s also possible for the same account to be listed under two different creditors.

This figure is also called the utilization ratio.For example, if you have $10,000 of available credit combined on two creditcards accounts, and your outstanding (unpaid) balance combined on the two cards equals $4,000, your utilization ratio is 40%. Contact us today at (888) 488-4517 or Apply Online now.

Debt Consolidation Guide. Owing money to several creditors and remembering when the monthly payments are due for all of them can be overwhelming. And worse, forgetting to pay on time will lower your credit score and cost you more in late payment fees. But is debt consolidation a good idea for you? Get Some Relief!

On May 1, the Federal Trade Commission (FTC) announced a permanent ban from debt relief telemarketing for operators of debt relief scam. The FTC charged the defendants with taking tens of millions of dollars from people by falsely promising to eliminate or substantially reduce their creditcarddebt.

However, the potential financial “fall out” of missing a payment, charging creditcards up to and over their limit or opening several new credit accounts over a short period of time can have a negative impact on the scores. For additional resources on protecting your credit during COVID-19, visit ficoscore.com/coronavirus.

Amid economic uncertainty, and lockdowns extending through April and possibly into May, it is tempting to call creditors requesting payment extensions. Contacting the company by phone is the only way to get help, which typically includes the following: waived payments, interest, and penalties, along with suspended creditbureau reporting.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content