This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

District Court for the Eastern District of Texas granted the CFPBs unopposed motion for a 90-day stay in the litigation filed by Cornerstone CreditUnion League and Consumer Data Industry Association (the Plaintiffs). WHAT THIS MEANS, FROM AYLIX JENSEN OF MOSS & BARNETT: OnFebruary 6, the U.S. More details here.

For creditunions and smaller banks in North America, the challenge of how to compete with their bigger counterparts is a constant and pressing matter. Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a creditbureau.

Shouldn’t all unpaid debts ( medical or otherwise), be reported to credit reports in the same way? Forcefully suppressing unpaid medical debts from creditbureau reporting will certainly result in many unintended consequences. Wouldn’t this increase the risk of the bank/creditunion with whom he takes that mortgage?

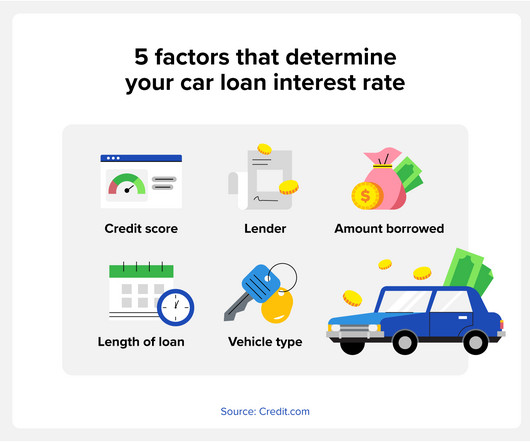

Average New and Used Car Loan Interest Rates Each quarter, the creditbureau Experian® releases the State of the Automotive Finance Market Report , and it tracks a variety of new and used car finance trends. Get a co-signer If you have a low credit score, getting a co-signer for your auto loan can help you get a better interest rate.

To further enhance flexibility and predictive power, the addition of FICO® Score 10 T incorporates trended creditbureau data. With the FICO® Score 10 Suite, lenders gain up to a ten percent predictive lift over previous FICO Score models. We have used FICO® Scores for many years.

The law does not apply to banks, savings and loan associations, savings banks, thrift companies, or creditunions. Providing inaccurate information to a creditbureau. Engaging in any unfair or deceptive practice or misrepresenting or omitting any material information in connection with the servicing of a student loan.

For creditunions and smaller banks in North America, the challenge of how to compete with their bigger counterparts is a constant and pressing matter. Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a creditbureau.

The report found that roughly a quarter of consumers are still being charged these fees despite the CFPB’s hostility towards so called “junk fees,” which has led many banks and creditunions to eliminate such fees. Overdraft fees are somewhat more prevalent than NSF fees (23.6% versus 20%, respectively).

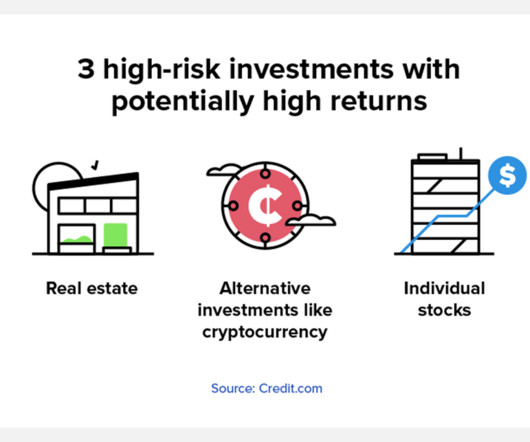

The creditbureau Experian® describes compound interest as “when interest gets added to the principal amount invested or borrowed, and then the interest rate applies to the new (larger) principal.” Risk level: Very low How to invest: Banks, creditunions, and online banks Potential returns: Moderate 2.

There are many creditbureaus, but the ones you’ve probably heard of are the influential big three: Equifax, TransUnion, and Experian. These operate nationwide, and lenders, banks, and creditunions report your credit history to them. Here’s a breakdown of how Equifax rates credit scores: 670 to 739.

Average Interest Rates for New Credit Card Offers LendingTree analyzed the terms and conditions of 200 credit cards from upwards of 50 different credit card companies, banks, and creditunions. With this data, they were able to gather an assortment of information involving annual percentage rates (APR).

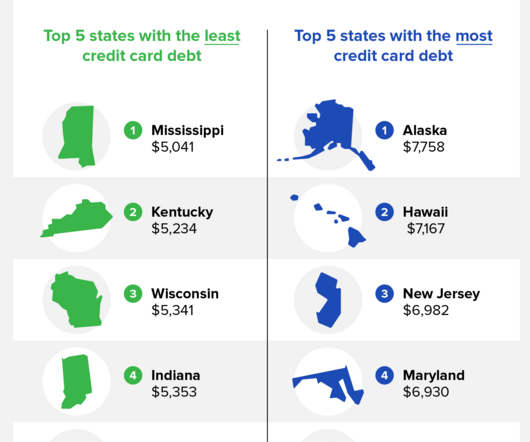

5 percent decrease, and some states were able to continue keeping their debt low, according to Credit Karma’s report. Average interest rates for new credit card offers Lending Tree analyzed the terms and conditions of 200 credit cards from upwards of 50 different credit card companies, banks and creditunions.

Lenders can include car dealerships, banks, and creditunions. The Effects of Your Credit Score on Car Insurance. the cost, how insurers calculate their premiums, and, possibly, does credit score affect car insurance? It’s always a good idea to research a few lenders to find out who will offer you the best conditions.

You can get a free credit report each year from the three main creditbureaus—Equifax, Experian, and TransUnion—by going to www.annualcreditreport.com. Dispute negative items : If you notice any mistakes on your credit report, complain to the relevant creditbureau.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content