This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

District Court for the Eastern District of Texas granted the CFPBs unopposed motion for a 90-day stay in the litigation filed by Cornerstone Credit Union League and Consumer Data Industry Association (the Plaintiffs). Failing to pay a debt and being subject to foreclosure, eviction, and litigation is understandably difficult for consumers.

It’s smart to know how to remove negative items from your credit report, especially if you are soon to be applying for a mortgage or car loan. In fact, you can remove something from your credit history before seven years pass. Here’s How To Remove Negative Items From Your Credit Report.

Stringent data protection laws are another reason why credit organizations don’t share your credit report with creditbureaus outside the country. This gap in communication between two creditbureaus from different nations creates a barrier to transfer your credit score abroad.

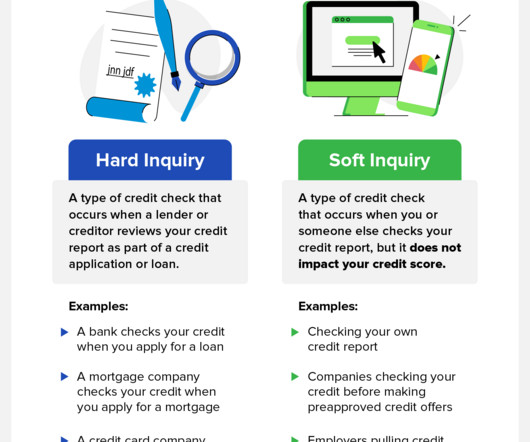

Checking your credit score will not hurt it. When you check your credit score, it is considered a “soft inquiry,” which means it does not negatively impact your score. Remember that while a few points may not seem like a lot, they could make a difference in whether or not you get approved for credit and what interest rate you receive.

While it doesn’t usually affect your credit score , you may want to correct information with the creditbureau if an employer you’ve never worked for is listed. Phone Numbers: You’ll see phone numbers associated with your credit accounts. Credit Cards. Account number of your loan or credit line.

Account errors: If someone steals your identity, your credit report may list accounts you never opened. Creditors may also make errors when reporting payment dates and payment amounts. Balance errors: A creditor may report the wrong balance or the wrong credit limit, which affects your credit utilization ratio.

Any time you apply for new credit, like a card, loan, or line of credit, the lender might run a hard credit check. Hard inquires give creditors an all-access pass to your credit reports. Hard inquiries get added as a new entry on your credit report, remaining there for two years. Foreclosure.

Soft inquiries have no effect on your credit. Whenever you apply for a credit card, the creditor might only obtain one of your reports, or they could opt for all three. Dealing with lenders and creditbureau representatives regarding fraudulent inquiries can be a hassle. Foreclosure. Charge-offs.

These credit pulls let lenders, landlords, and employers take an in-depth look at your credit usage, granting them access to your full credit report. When you apply for a card, the creditor could request your Equifax, Experian, or TransUnion report, or a combination of the three. Foreclosure. Charge offs.

This kind of inquiry has virtually no effect on your credit, leaving your score untouched and staying off your report. They grant creditors access to your full credit reports, and they’re required any time you apply for funding. When you file a dispute with a creditbureau, they have 30 days to investigate your claim.

This kind of inquiry has virtually no effect on your credit, leaving your score untouched and staying off your report. They grant creditors access to your full credit reports, and they’re required any time you apply for funding. When you file a dispute with a creditbureau, they have 30 days to investigate your claim.

Suspending rent payments die to COVID-19 may put you at risk for foreclosure if you can’t make up your deferred payments all at once. Amid economic uncertainty, and lockdowns extending through April and possibly into May, it is tempting to call creditors requesting payment extensions. Delayed payments are not forgiven payments.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content