This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Saudi CreditBureau Delivers Access To Loans For Millions with Score. Prior to the implementation, lenders in the region had been relying heavily on salary data to assess a consumer’s propensity to repay a loan. The adoption of the FICO® Score has allowed lenders to grow their portfolios and increase financial inclusion.

For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional creditbureau files. Figure 1: Creditbureau coverage is greater for some types of data than others. FICO has a solution to this problem.

For most of the credit-eligible US population there is sufficient traditional creditbureau data available for calculating a FICO® Score. An independent study conducted by the CFPB reached very consistent conclusions to our own, sizing the ‘credit invisible’ population at 26 million consumers.

Score 10 T gives mortgage lenders the flexibility and predictive power to make more precise lending decisions. It is FICO’s most powerful score to-date and gives mortgage lenders unparalleled flexibility and predictive power while preserving the trusted and proven FICO Score minimum scoring criteria. FICO Admin. by James Wehmann.

Personal loans accounted for $148 billion in consumer debt in the fourth quarter of 2020, a decline from the same period in 2019, according to creditbureau TransUnion. Lenders rely on. Personal loans are usually unsecured, meaning they don’t require collateral like a house or a car, and you can use them for almost anything.

Collection accounts are bad for your credit score. These negative marks on your credit report indicate you might not pay your bills on time—or ever, which is why lenders don’t like to see them. Collection accounts can stay on your credit report for up to 7 years. Each creditbureau has different information about you.

Depending on the specific creditbureau or bureaus that your vehicle loan lender reports to, it will only show up on those credit reports. There are three different creditbureaus that are mainly used by all lenders: Experian, Equifax, and Transunion. What Contributes to Your Credit Score?

When Is a Credit Card Payment Considered Late? As far as credit card companies are concerned, the payment is considered late if it’s submitted after the cutoff period, which varies depending on the lender. Generally speaking, a late fee is issued if payment is received after the credit card issuer’s cutoff time.

FAQ Consider Hiring a Credit Repair Company How Collection Accounts Impact Your Credit Collection accounts have a significantly damaging impact on your credit score because they’re negative marks that indicate to lenders you may not pay your bills on time—or ever. Does your account information seem accurate?

Shouldn’t all unpaid debts ( medical or otherwise), be reported to credit reports in the same way? Then let the lenders decide which one they want to consider or ignore. Forcefully suppressing unpaid medical debts from creditbureau reporting will certainly result in many unintended consequences.

The Truth in Lending Act is part of the Consumer Credit Protection Act. This law deals with what information lenders must disclose, how they can advertise their products and rates and what rights you have when a lender isn’t truthful or transparent. Credit law can be complex.

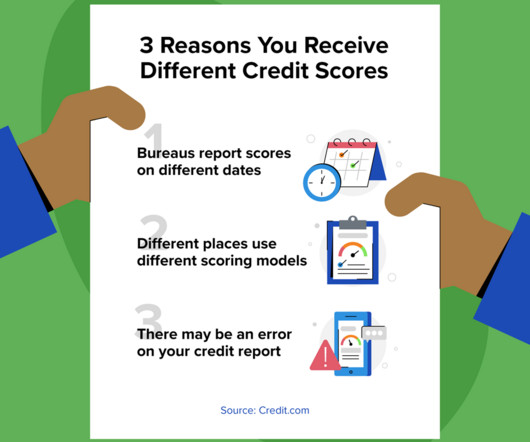

The primary credit scoring models are FICO® and VantageScore®, and both are equally accurate. Although both are accurate, most lenders are looking at your FICO score when you apply for a loan. There’s a lot to learn about credit scores and credit reports and having more than one credit score can get confusing.

Some creditbureaus are now incorporating alternative credit data like rent and utilities payments so that consumers with a very limited history of managing debt can qualify to take on more debt. Credit card companies market credit scores as a badge of honor, giving you the power to negotiate better rates and terms from lenders.

Incorrect Personal Information Lender Inquiries You Don’t Recognize Accounts You Never Opened Credit Utilization Goes Up Credit Score Goes Up or Down Unexpectedly Public Records You Don’t Recognize. How Do I Check My Credit for Identity Theft? Warning Sign 2: Lender Inquiries You Don’t Recognize.

When using artificial intelligence (AI) or complex credit models, can lenders rely on the checklist of reasons provided in Regulation B sample forms for adverse action notices? According to today’s guidance issued by the Consumer Financial Protection Bureau (CFPB or Bureau), the answer to that question is, in many circumstances, no.

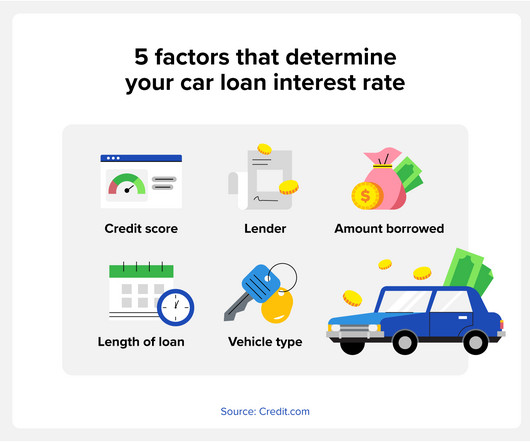

Average New and Used Car Loan Interest Rates Each quarter, the creditbureau Experian® releases the State of the Automotive Finance Market Report , and it tracks a variety of new and used car finance trends. A credit score plays a large role when lenders determine vehicle interest rates, but it’s not the only factor.

High Credit Card Balances The amount of credit card debt you have compared to your credit limits, known as your credit utilization ratio, is another crucial factor in calculating your credit score. Solution: Aim to keep your credit card balances low relative to your credit limits.

and globally -- making access to credit more efficient and objective, which has continued into the present day. FICO® Scores are dynamic and evolve as changes in consumer behavior are reflected in the underlying creditbureau data housed and managed by the three primary U.S. consumer reporting agencies (CRAs). in April 2022.

The credit score was invented in 1989 to make credit reports more actionable for lenders. Credit scores affect many parts our lives: whether we qualify for a loan, what interest rate we pay, even where we can rent or whether we get our dream job. However, this does not influence our evaluations.

We work with lenders worldwide who want to grant credit to people who traditionally found it hard to get credit, because there’s just no data on them to guide a decision. Our Financial Inclusion Initiative was founded precisely to help lenders serve these unbanked and underbanked people worldwide.

To have a FICO Resilience Index score , you must have at least one account that was reported to the creditbureau in question in the past 6 months. As of July 2020, the FICO Resilience Index is being provided in pilot testing to lenders. Does This New Number Make Credit Scores Less Important?

Over the last 30 years, FICO has continued to analyze the minimum amount of creditbureau data that is necessary to deliver a reliable, predictive FICO® Score to the market - which benefits both consumers and lenders alike. consumers that do not have sufficiently current creditbureau data to generate a score.

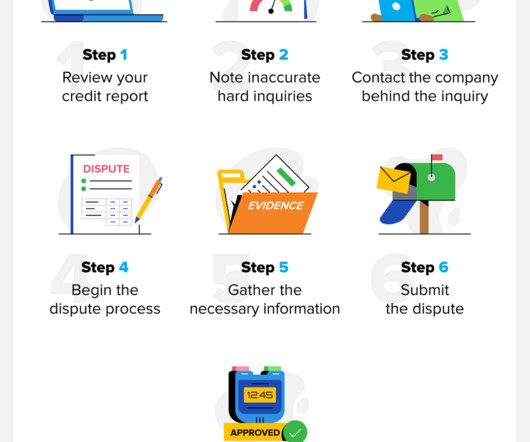

If you’ve got an error of your credit report, it’s up to you to find it, dispute it, and fix the error. Formally disputing an error involves writing a formal dispute letter to the creditor as well as the appropriate creditbureau reporting the inaccuracy. Tell the creditbureau what action you want them to take.

Professional credit repair projects tend to take two to three months. This would be money well spent if it restored your good standing with lenders in time to secure a loan with low-interest rates. What Will Help Improve Your Credit Score. In reality, paying off these accounts will not help your credit. Ads by Money.

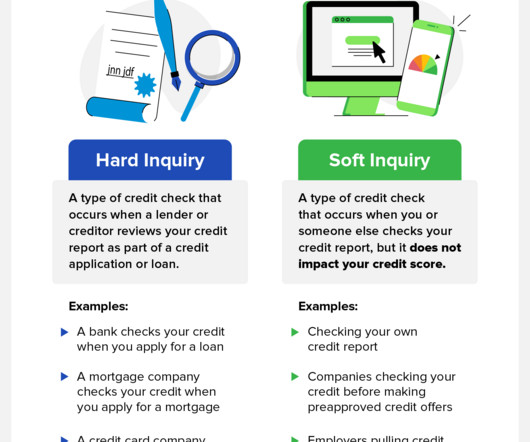

Lenders and credit card issuers carry out two types of checks on your credit. The first, a soft credit check, doesn’t impact your credit score at all. We’re going to walk you through soft and hard credit checks and what they mean for your credit score. This is why it doesn’t affect your credit score.

Approximately one third of consumers with a creditbureau file were contacted by at least one creditor or debt collector each year, according to a CFPB (Consumer Financial Protection Bureau) survey. The FDCPA applies only to debt collectors (the third-party collection agencies), not to the original lender.

Rent, home payments, utilities such as gas, water, electric, and even things like cable or other on-time payment history can be used by creditbureaus to create a reliable credit score from which they can underwrite credit. What lenders use alternative credit data to grant credit?

When youre late on payments or stop making payments on a loan, the lender can repossess or repo the item youre financing to settle your debt. Knowing how to get a repo off your credit report can help you boost your score and minimize the impact of those negative items on your credit score. Review Your Credit Report Step 3.

Your credit score is an important aspect of your financial health and is oftentimes used by lenders, landlords, and even employers to determine your creditworthiness. It’s crucial to keep track of your credit score regularly, but many people are hesitant to check it because they’re afraid it will have a negative impact.

consumer data not present in the traditional creditbureau files) to enhance the predictiveness and inclusiveness in credit scoring. with little or no credit information in their traditional creditbureau files, who have traditionally struggled to access credit. More than 200 million U.S.

All three for-profit credit reporting agencies, Experian, Equifax and Transunion compile and report consumer credit and debt payment activity and sell this consumer information to lenders seeking to grant credit. Here’s why: Who Decides Your Credit Score? Final Thoughts.

You can request the removal of hard inquiries from your credit report by pointing out unauthorized checks or going through a formal dispute process with major credit agencies. Whether you’re looking to buy a house, lease a car, or get a loan, lenders need to check your credit. Note all inquiries you did authorize.

Examples of such factors are changes in macroeconomic conditions, employment status, and shifts in lender underwriting standards. Many will successfully weather this pandemic using the necessary data and tools will help you to manage potential emerging risks without cutting off access to credit for those resilient customers.

For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional creditbureau files. Figure 1: Creditbureau coverage is greater for some types of data than others. FICO has a solution to this problem.

It serves as a broad-based, independent standard measure of credit risk. It is relied upon by stakeholders across the entire lending ecosystem – from regulators, investors and boards to consumers, lenders, and brokers – as a baseline metric for assessing credit risk that is fair to both lenders and consumers. .

Many lenders give borrowers a grace period before they technically consider the payment late. Lenders consider any payment not made within this allotted time frame a late payment. Since each lender has its own terms and conditions, it’s important to read the terms of your auto loan. So, how late can you be on a car payment?

While the BNPL product offers consumers some attractive features, it is essential that both lenders and consumers alike understand the potential impact these BNPL loans could have on consumers’ FICO Scores. But what might be the impact to the FICO ® Score of BNPL accounts being included in the credit report?

Stringent data protection laws are another reason why credit organizations don’t share your credit report with creditbureaus outside the country. This gap in communication between two creditbureaus from different nations creates a barrier to transfer your credit score abroad.

The FICO® Score 10 Suite outperforms all previous FICO Scores, giving lenders unparalleled predictive power to make more precise lending decisions. With the FICO® Score 10 Suite, lenders gain up to a ten percent predictive lift over previous FICO Score models.

The letter should include details about the debt, the original lender, and the debt collector’s authority to collect the money. A debt validation letter is written correspondence that debt collectors are legally obligated to send you that provides information about the debt they’re collecting.

This data is supplied by lenders, creditors and businesses where you have accounts. The information contained in your credit report determines your credit score. Higher credit scores are more attractive to lenders and creditors. You also want to ensure your creditor reports payments to the creditbureau.

Let’s assume the lender in this example is aiming to grow its new-to-system customer portfolio via launching a new digital lending product: small-ticket unsecured instalment loans. However, for an instant, digital credit decision process, this capability is a must. . So what do I mean by “strong data ingestion capability”?

While the FICO® Score has been trusted by consumers, lenders and investors for decades, the data that goes into a FICO® Score can be as recent as a payment reported by your lender today. . How frequently the data is updated depends on where it resides: CreditBureau Data. How current is the data in my FICO Score?

Whenever you apply for anything—a loan, credit card, etc.—the the lender will need to look into your credit report. Called a credit check, there are two kinds of credit checks—hard and soft. Each is used for different reasons and has a different impact on your credit score. The Bottom Line on Soft Inquiries.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content