This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Personalloans accounted for $148 billion in consumer debt in the fourth quarter of 2020, a decline from the same period in 2019, according to creditbureau TransUnion. Personalloans are usually unsecured, meaning they don’t require collateral like a house or a car, and you can use them for almost anything.

When a lender doesn’t receive payments for a line of credit, they may choose to eventually sell that credit to a debt collection agency to get some of their money back. That line of credit will then be reported to the credit reporting bureaus as a collection account—a collections account for a credit card, personalloan, etc.—and

and globally -- making access to credit more efficient and objective, which has continued into the present day. FICO® Scores are dynamic and evolve as changes in consumer behavior are reflected in the underlying creditbureau data housed and managed by the three primary U.S. consumer reporting agencies (CRAs). in April 2022.

Your New Car Loan Shows up on Your Credit Report. As with any new credit account that you get, your new car loan will show up on your credit report. Depending on the specific creditbureau or bureaus that your vehicle loan lender reports to, it will only show up on those credit reports.

FAQ Consider Hiring a Credit Repair Company How Collection Accounts Impact Your Credit Collection accounts have a significantly damaging impact on your credit score because they’re negative marks that indicate to lenders you may not pay your bills on time—or ever.

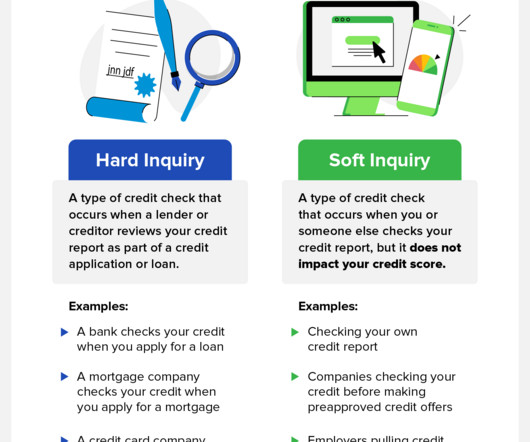

Promotional inquiries and account review inquiries are nothing to worry about, because they’re preapproved credit offer inquiries or inquiries by companies you already do business with. Tip: Sometimes, the name of a financial institution doesn’t precisely match the name of the company checking your credit. Learn More about ExtraCredit.

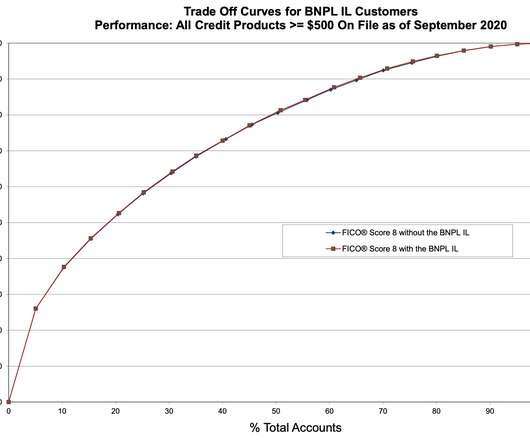

To the extent that BNPL loans are reported to the CRAs and incorporated into the core consumer creditbureau file, they will be factored into all existing versions of the FICO Score. But what might be the impact to the FICO ® Score of BNPL accounts being included in the credit report?

Promotional soft credit checks. For example, if you receive a mailing from a personalloan or credit card company stating you have been prequalified for potential credit, that company has probably run a soft check. Soft vs. Hard Credit Checks. Soft credit checks are different from hard inquiries.

To further enhance flexibility and predictive power, the addition of FICO® Score 10 T incorporates trended creditbureau data. These in-depth insights can help lenders expertly manage credit risk in these uncertain times, while continuing to make competitive credit offers to consumers. .

Alternative credit sources that do not report to the creditbureaus can include payments for rent, utilities, service accounts, and personalloans. Rent Bureau , now owned by the creditbureau Experian, electronically compiles rental data from property management companies and individual landlords.

Creditbureaus measure variables related to your debt like the total amount of your debt, if you make your debt payments on time, how long you have been paying on debt obligations and how much debt you are servicing relative to how much potential debt has been extended to you. Reporting occurs only if the account goes into default.

Stringent data protection laws are another reason why credit organizations don’t share your credit report with creditbureaus outside the country. This gap in communication between two creditbureaus from different nations creates a barrier to transfer your credit score abroad.

How much debt does the average person owe? . According to creditbureau Experian’s 2019 Consumer Credit Review , we are accumulating debt at an average of 3% per year.

These include transferring all your debt onto just one credit card as well as taking out a secured or unsecured personalloan—perhaps with the help of a professional debt consolidation company. HELOC loans are similar, except that you can continue to draw money from them—up to a set amount. Credit card 3.

Credit card balances reached a record-setting $866 billion in the third quarter of last year, which represents a year-over-year increase of 19%. Credit balances reached a record-setting $866 billion in the third quarter of last year – and they are expected to keep climbing, the report from TransUnion said.

A hard inquiry is a credit check that occurs when a lender or creditor reviews your credit report as part of a credit application or loan. Hard inquiries are sometimes called “hard pulls,” and they typically occur when you apply for a new credit card, a personalloan, a mortgage, or other types of credit.

While it doesn’t usually affect your credit score , you may want to correct information with the creditbureau if an employer you’ve never worked for is listed. Phone Numbers: You’ll see phone numbers associated with your credit accounts. Student Loans. Auto Loans. Credit Cards.

There isn’t a right or wrong answer regarding how many credit cards somebody should have — it all depends on your money management skills and finances. Some people may be able to manage two credit cards, while others may be comfortable with 10 or more. Find a way to increase your credit mix.

These levels refer to the total amount of money owed by individuals to creditors and encompass various forms of credit, including credit card debt, personalloans, mortgages, and auto loans which can significantly impact financial stability and economic conditions. increase compared to the fourth quarter of 2023.

Finding a way to score millions without credit history. Círculo de Crédito , the fastest-growing creditbureau in Mexico, has used unique credit risk scores from FICO to boost financial inclusion in Mexico and help an additional 20 million citizens access credit.

Interest rates in Canada increased notably in 2018, impacting consumers across the board, but particularly those with interest rate-sensitive products such as lines of credit, and variable rate personalloans and mortgages.

In our last blog post , we discussed key considerations in the impact to the FICO® Score of Buy Now, Pay Later (BNPL) accounts being included in the consumer credit file based on our research on data from a major BNPL provider in the U.S. personalloans and credit cards) reported in the credit file.

If you find an inaccuracy, dispute the entry with the creditbureau that’s reporting inaccurate information. The bureau will have 30 days to verify its information is accurate. If it’s inaccurate, the bureau will need to either correct the data or remove the entry in accordance with the Fair Credit Reporting Act.

You probably hear all the time about how important a good credit score is. You’ve likely also heard that a good credit score is essential to getting a mortgage, or a good deal on a personalloan for a car. But what exactly is your credit score, anyway? And what even constitutes a “good” credit score range?

The three-digit numbers called credit scores are how the scoring institutions break down your credit profile. That number is calculated based on the information in your credit report at a creditbureau. Your file is a picture of how you’ve used credit to date. credit score for free for life.

The Fair Credit Reporting Act (FCRA) requires credit reporting agencies to show only accurate information about your credit history. If you can find inaccurate information, the creditbureau will have to fix the information. When you apply for new credit, lenders know your old lenders lost money on your accounts.

Find out about the origin of the debt, such as credit cards, medical bills , or personalloans. This documentation can be helpful if you need to dispute charges or escalate a dispute to a creditbureau or a consumer protection agency.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content