This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With inflation proving more sticky than policymakers had hoped and uncertainty around how the new administrations policies might affect it, it may take longer for people to see lower interest rates on their mortgages, car loans and creditcard balances, which could prove challenging to household budgets.

Meanwhile, eyes are on the Big Apple as the New York Department of FinancialServices (DFS) and the New York City Department of Consumer and Worker Protection are simultaneously engaged in amending their consumer debt collection rules. consumer creditcarddebt has increased to nearly $1 trillion.

The report also showed that people are having more trouble paying off that debt, with creditcard balances increasing by $45 billion to $1.21 trillion and auto loan balances increased by $11 billion to $1.66 of outstanding debt now in some stage of delinquency. Delinquency rates ticked up 0.1%

On October 26, a House FinancialServices subcommittee drafted legislative proposals related to the buy now, pay later (BNPL) and earned wage access (EWA) market. On October 25, the CFPB released its biennial report to Congress on the consumer creditcard market. financial institutions.

The rise of interest in BNPL is also likely influenced by increased financial uncertainty, high-interest rates and a downward trend in creditcard approval. As consumers show preference for digital financialservices, BNPL continues to grow and become available at more retailers. . Why are BNPLs Popular with Gen Z?

On May 1, the CFPB proposed a rule to implement a congressional mandate to establish consumer protections for residential property assessed clean energy (PACE) loans. PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels.

On December 1, the CFPB, the Federal Reserve Board, and the Office of the Comptroller of the Currency announced that the 2022 threshold for exempting loans from special appraisal requirements for higher-priced mortgage loans will increase from $27,200 to $28,500. For more information, click here. For more information, click here.

Financial literacy is an essential life skill that benefits people throughout their lives, but is often overlooked when it comes to what happens if a payment is late or missed. Financial literacy during delinquency is just as important as planning for the future—and can even play a big part in financial future-planning.

Basically, credit scoring models want to see that you can manage different types of financing, most notably revolving accounts, such as a creditcard, and installment accounts, such as a mortgage or auto loan. The credit bureaus have determined that the types of accounts you have is predictive of your future credit risk.

According to the CFPB, on average, BNPL borrowers were much more likely to be highly indebted, revolve on their creditcards, have delinquencies in traditional credit products, have lower credit scores, and use high-interest financialservices such as payday, pawn, and overdraft compared to non-BNPL borrowers.

By revising the Telemarketing Sales Rule (TSR), the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC), along with state Attorneys General set forth a strict set of regulations that standardize the way all financialservices companies in the debt relief industry must operate.

The Arizona Court of Appeals and Arizona Supreme Court have issued numerous opinions over the last several years clarifying when a cause of action accrues for mortgages and creditcarddebt. In Velazquez v. FMZ Industries, Inc.

That’s because it can be easy to get discouraged or overwhelmed when looking at larger financial ambitions you may have. For example, you may have a significant amount of creditcarddebt. This goal is more attainable.

Whilst the new payment method originally took off in Europe, it has slowly sept into the US market as startups, like Affirm , have gone public and found success, and Square , the San Francisco based financialservices and digital payments company, bought Australia’s Afterpay in $29billion deal, to benefit off BNPL’s growth.

As background, the plaintiff filed suit after receiving a collection letter from SAS, stating the total due on her debt was $2,017.83 The debt stemmed from a 2014 judgment on a creditcarddebt for $1,015.20, which included pre-judgment interest of 9% and certain fees and costs.

Renters’ debt obligations also differed considerably from those of homeowners before the pandemic. In June 2019, renters were more to have student debt and to have used some form of alternative financialservice, such as payday lender, pawn shop, or auto-title loans.

A hike in the federal interest rate prompts a jump in the Bank Prime Loan Rate ( prime rate ), the credit rate that banks offer to their most credit-worthy customers and off of which they base other forms of consumer credit like mortgages and consumer loans. Missed payments on certain loans are already on the rise.

The fourth quarter marked the resumption of student loan payments for 22 million Americans, but repayment results were low. million borrowers missed their student loan payment —that’s 40% of loan holders. Breaking it down, creditcard balances increased by $48 billion to $1.08 trillion in Q3 2023, showing a 4.7%

After your birthday, Social Security number, and cell phone number, your credit score is the most important number in your life. Your credit score, known in the financialservices industry as a Fico Score, is a snapshot of your financial history. You’ll be taken to websites that try to sell you financialservices.

Preparing for a future that would need to include litigating collections from a diverse portfolio of creditor sources (creditcard, medical, bankruptcy, student loan, subrogation, commercial – just to name a few) became more and more pragmatic as the years of the recession marched forward.

Americredit FinancialServices, Inc. , 29, 2006), the plaintiff had made multiple late payments on her car loan before paying the loan off entirely. Plaintiff made the payments as agreed and the debt was discharged. In Moulton v. C 04-02485 JW, 2006 WL 8459731 (N.D. Barclays Bank Delaware , No. Grossman , at *2.

The COVID-19 pandemic cast a huge shadow on the financialservices worldwide. We hope that what readers learned helped instill confidence in keeping credit flowing during uncertain times. Many lenders are offering multiple options to consumers, including temporary deferred payment plans and/or placing loans in forbearance. “We

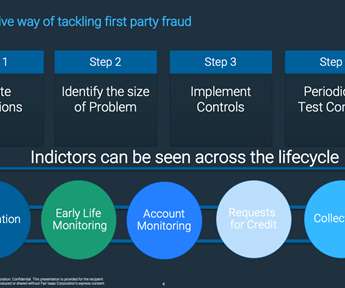

Or they may unintentionally sell it to criminal gangs, which then rack up thousands of pounds of fraudulent creditcarddebt. Furthermore, you might automatically assume that first-party fraud only affects banks, but as telcos evolve into payment processing and handset financiers, they also are now feeling the pinch.

In 2021, the financialservices world continued to grapple with the uncertainty brought on by year two of the COVID-19 pandemic. The next natural question is: how much of this data is available at the three nationwide credit bureaus? FICO® Scores use data from the three main credit bureaus.

Customers couldn’t be faulted when they heavily offset the drop in purchasing power and disposable income by leveraging a higher utilization of credit products that they have at their disposal towards staying afloat in these perilous times. You might raise credit lines and limits, for instance, on customers likely to pay.

The key is how these macrolevel measures impact individuals’ finances – all consumers are paying higher prices at the grocery store and gas station, but not all cash strapped consumers are shopping for loans or carrying large amounts of debt. This is only a 3.6% decrease year-over-year, but is still ~18.2%

automobiles, 35% of them with a car loan. creditcards for 27% of all transactions with average creditcarddebt of $3352. On average, they pay $95,000 in homeowners insurance over their home-owning lifetimes. Purchases 9.4 And they pay about $94,000 for auto insurance over their driving lifetime.

Some lawmakers and regulators are calling for interest rate caps and lower fees on creditcards as debt levels march higher. Total creditcarddebt topped $1 trillion in the second quarter of 2023 for the first time ever. proposed a 36% cap on consumer loans in 2021. Alexandria Ocasio-Cortez, D-N.Y.,

Department of Health and Human Services (HHS), and the U.S. Department of the Treasury (Treasury) launched an inquiry into specialty financial products, such as medical creditcards and installment loans, that consumers can use to pay for medical care. Abusive Telemarketing Acts or Practices).

Our bank and loanservicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. In reviewing the market for potential consumer harm, the report presents the latest research on consumer card use, cost, and availability.

Chicago Federal Reserve President Austan Goolsbee said Friday that while consumer debt levels aren’t yet “especially” high, the Fed is concerned about the rate of consumer delinquencies, or missed or late payments on expenses such as auto loans, creditcard bills and rent. “If

Our bank and loanservicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. million, to people who lost money to creditcarddebt relief schemes. For more information, click here.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content