This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Creditcarddebt took a nosedive in the early days of the pandemic in 2020 as consumers stayed home, lost work and received cash infusions from the government. Creditcarddebt increased 15% year over year — the largest one-year increase in more than two decades, according to the Federal.

Say goodbye to creditcard stresssee if Chapter 7 bankruptcy is your solution. Creditcarddebt relief often seems unattainable, but there is a way forward. Chapter 7 bankruptcy can help clear debt and give you a fresh start. Will it erase all your debt, or are there limits?

When Should You Consider a Debt Settlement Program ? Carrying large amounts of unsecured debt is a sign of financial stress, even if you are making regular monthly minimum payments on all your accounts. Personal loans, creditcarddebt, payday loans, or medical bills all fall into the category of unsecured personal debt.

If you have ever had to deal with creditcarddebt, you know it can be stressful. Debt collectors call at all hours of the day and pressure is put on borrowers to quickly make payments in full. The process begins when the debtor stops making payments on their creditcard and goes into default.

Each state gives creditors and collection agencies varying times to file suit on unpaid and delinquent creditcarddebt. Note that in all states, these limitations are governed by state laws – not federal. Most statute of limitations regarding creditcarddebt is between 3-10 years or longer.

Creditcarddebt is on the rise. trillion on their creditcards, the Federal Reserve Bank of New York reported Tuesday. year over year, according to a separate quarterly credit industry insights report from TransUnion. The post Average consumer now carries $6,329 in creditcarddebt.

Job gains showed up in health care, social assistance, transportation and warehousing, along with retail trade, which reflected the return of workers from a strike, while federal government employment declined as a result of wide-reaching layoffs. The Federal Reserve (Fed) held rates steady at 4.25-4.50% 4.50% in March.

The kinds of debt that can typically be eliminated are creditcarddebt, medical bills, utility bills, evictions, repossessions, and personal loans. You can also wipe out debts owed to gyms, clubs, and other personal services. Which Debts Cannot Be Discharged by Chapter 13 Bankruptcy?

Here are some reasons why consumers were more focused on reducing their creditcarddebt: Reduced spending because of pandemic-related restrictions on travel and entertainment, along with a more judicious mindset because of the economic uncertainty created by the pandemic. by Tommy Lee.

consumers took on $43 billion in additional creditcarddebt during the second quarter of this year, ending in June. That’s more than triple the average amount of new debt households have taken on in that period since after the Great Recession of 2007-08. Newly released data from WalletHub says U.S.

As the federal funds rate rose, the prime rate did, as well, and creditcard rates followed suit. Despite the steep cost, consumers often turn to creditcards, in part because they are more accessible than other types of loans, Schulz said. The post Creditcarddebt hits a ‘staggering’ $1.13

At the same time, you may have student loan and creditcarddebt that is more than you can afford. Debt has a way of growing. While struggling to make ends meet each month, the temptation to rack up even more debt can be great for people with unfinished degrees. Fewer job prospects without a degree.

consumers said they use digital installment payment services to avoid creditcarddebt. Consumers turning to BNPL services to avoid creditcarddebt is not surprising, given that both millennial and Gen Z shoppers have complicated relationships with creditcards. Eighty percent of U.S.

At the beginning of March, the federal government ended pandemic-era payments for low-income families on the Supplemental Nutrition Assistance Program (SNAP), causing nearly 30 million Americans to lose increased food stamp benefits. consumer creditcarddebt has increased to nearly $1 trillion.

Based on data from the New York Fed’s Consumer Credit Panel, a nationally representative sample drawn from anonymized Equifax credit data, the report provides a quarterly snapshot of household trends in borrowing and indebtedness, including data about mortgages, student loans, creditcards, auto loans and delinquencies.

This is a common scenario because the average American has $90,000 in total debt , about $20,000 of which is unsecured debt like medical bills and creditcarddebt. Take a moment to think about what happens if you simply use your government stimulus check to make a one-time payment toward your debt.

Collections agencies buy your unpaid creditcarddebt from your card issuer when your balance lingers too long — but that doesn’t mean it goes away. When a collections representative from your creditcard issuer calls you, it’s usually because you haven’t made at least the minimum payment for at least 30 days.

consumers have experienced disruption to their income since the onset of the pandemic, the combination of government stimulus programs such as the CARES Act and payment accommodation programs being offered by lenders continues to enable many consumers to avoid falling behind on their bills. Fewer consumers are actively seeking credit.

Unsecured debts refer to debts that don’t have collateral. Some examples of unsecured debts include, but are not limited to, repossessions deficiencies, old lease balances, medical bills, cash advance loans, and creditcarddebts. Will Bankruptcy Eliminate All of My Debts?

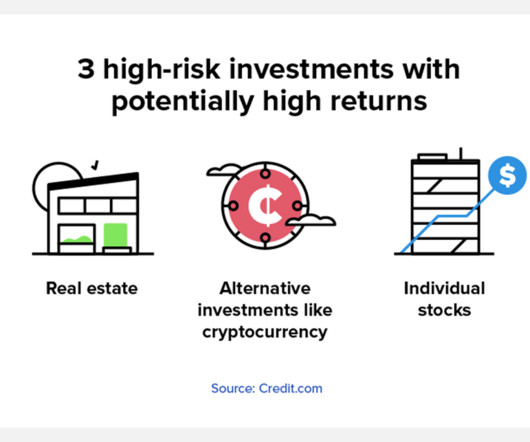

The best investments The best investments right now to grow your wealth include: High-yield Savings Accounts Short-term Certificates of Deposit (CDs) Government Bonds Corporate Bonds Real Estate and REITs Individual Stocks Index Funds Exchange-traded Funds (ETFs) Cryptocurrency 1.

It is prohibited for debt collectors to utilize unfair techniques, harass, or deceive consumers while seeking to collect consumer debts under the federal Fair Debt Collection Practices Act (FDCPA). The Fair Debt Collection Practices Act (FDCPA) applies to collection firms and debt collectors attempting to recover consumer debts.

Whether due to reined in spending in the face of the economic uncertainty wrought by the pandemic, or simply due to having fewer opportunities for spending on discretionary items such as restaurant, retail, and travel, consumer debt levels during the pandemic are down substantially. This is down from 8.1% pre-COVID (Jan 2020).

Consumer debt continues to accelerate at an alarming rate—particularly creditcarddebt—driven by a culture of consumption. Creditcarddebt is one of the most worrisome due to the high interest rates charged by creditcard companies, which can leave consumers with never-ending debt loads.

Creditcarddebt is a huge reason people end up filing for bankruptcy. The incredibly high interest rates alone plus the ease of procuring cards contribute to what can be a vicious cycle of maxing out limits, paying only minimums, and applying for more cards. But can you file for bankruptcy on creditcards only ?

Each year, we provide insight into the national average FICO® Score to help ensure consumers have a baseline measure of credit health standing. Government stimulus programs have been ramping down and payment accommodations reported in the credit bureau data have largely reverted to their pre-pandemic levels.

When government assistance is not providing enough income to cover job losses, should you file for bankruptcy or hold out for the economic recovery? Creditcard companies grant payment relief between one and three months without penalties or credit reporting. The Bankruptcy Option.

alone, the value of revolving credit outstanding in 2022 amounted to approximately $1.12 Additionally, Forbes reported that the average creditcarddebt per borrower was $5,474 in the third quarter of 2022—meaning that creditcarddebt can quickly stack up and overwhelm borrowers. In the U.S.

The report, “Financial conditions for renters before and during the COVID-19 Pandemic,” finds that some government relief efforts likely helped maintain the financial stability of renters and their families.

The United States Bankruptcy Code governs both chapter 7 and chapter 13 bankruptcy. Without having to repay it later, you may immediately begin rebuilding your credit. . If you have a large amount of creditcarddebt or high medical costs that you can’t pay, Chapter 7 may allow you to start again.

Regaining health insurance could mean extending the corporate plan, buying an individual policy, or relying on government insurance programs. As of now, the government has not universally reopened the ACA exchanges for all citizens. Are Government Health Care Programs Available and Under What Circumstances ?

Although the idea of liquidating your assets may sound stressful and undesirable, most of those who declare Chapter 7 can retain all of their possessions after filing.

We’ve seen FICO® Scores in Canada steadily increase throughout the pandemic due, at least in part, to strong performance of equity markets, sustained economic growth, a booming real estate market , payment accommodation programs by lenders , and government stimulus which helped boost household savings to unprecedented levels.

News & World Report shows that more than eight in 10 Americans who have creditcarddebt are experiencing anywhere from a little to a lot of anxiety about it. Nearly 31% have at least $6,000 of creditcarddebt. have creditcarddebt of $10,000 or more.

Based on data from the New York Fed’s Consumer Credit Panel, a nationally representative sample drawn from anonymized Equifax credit data, the report provides a quarterly snapshot of household trends in borrowing and indebtedness, including data about mortgages, student loans, creditcards, auto loans and delinquencies.

Have you ever felt in over your head with debt? According to a 2024 study, the average level of personal debt, not including mortgages, is over $22,000. Maybe youve been hit with unexpected medical bills or accrued creditcarddebt over time.

Director Chopra delivered remarks at the May 4, 2023, meeting of the American Association of Healthcare Administration Management's Government Relations Committee and Executive Board

Through this report, the Fed wishes to provide “ a quarterly snapshot of household trends in borrowing and indebtedness, including data about mortgages, student loans, creditcards, auto loans and delinquencies. trillion of auto loan debt in fourth quarter 2013, rising to $0.95 For comparison, there was $0.86 Auto loans: $0.95

This is why many people engage the services of a debt relief agency. TransUnion calculates that paying off $5,000 of creditcarddebt at the minimum rate costs $10,000 in interest. The fees you can expect to pay for Freedom Debt Relief’s services range from 15–25%. National Debt Relief vs. Freedom Debt Relief.

Whether due to reigned in spending in the face of the economic uncertainty wrought by the pandemic, or simply due to having fewer opportunities for spending on discretionary items such as restaurant, retail, and travel, consumer debt levels during the pandemic are down substantially. This is down from 8.1% pre-COVID (Jan 2020).

Consumer financial protection laws safeguard borrowers’ control over how and when they pay back debt, including creditcarddebt. For example, the Truth in Lending Act (TILA) contains important protections for consumers who have both a creditcard account and a savings or checking account with the same bank.

The findings in this report cover violations of law and consumer harm in the areas of auto and student loan servicing and debt collection, including creditcarddebt collections. This is the 34th edition of Supervisory Highlights.

Household Debt and Credit Developments as of Q2 2024 CATEGORY QUARTERLY CHANGE * (BILLIONS $) ANNUAL CHANGE** (BILLIONS $) TOTAL AS OF Q1 2024 (TRILLIONS $) MORTGAGE DEBT (+) $77 (+) $505 $12.519 HOME EQUITY LINE OF CREDIT (+) $4 (+) $40 $0.38

As the federal funds rate rose, the prime rate did, as well, and creditcard rates followed suit. Why creditcarddebt keeps rising Despite the steep cost, consumers often turn to creditcards, in part because they are more accessible than other types of loans, according to Matt Schulz, chief credit analyst at LendingTree.

Mail solicitations for cards plunged last year, hitting a new low of 61.6 Creditcarddebt levels also fell sharply, as many borrowers paid off or lowered their balances with savings they accumulated from staying at home more often and government relief payments.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content