This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Why it matters: For professionals in debt collection agencies, debt buying companies, fintechs, banks, creditunions, and consumer finance firms, these findings underscore a growing vulnerability among older borrowers.

But what about creditors? All creditor clients that use a third party agency should know about Regulation F. They talked about types of consent, data maintenance and consent best practices for both creditors and third party collection partners. Regulation F is now a reality. Implied Consent .

District Court for the Eastern District of Texas granted the CFPBs unopposed motion for a 90-day stay in the litigation filed by Cornerstone CreditUnion League and Consumer Data Industry Association (the Plaintiffs). In an alarming trend, we are seeing more consumer actions being brought for abandoned litigation.

The first consideration that lenders (banks and creditunions alike) often face is when, and if, to conclude that the account owner does not intend to, or is not able to, clear the negative balance or loan deficiency. Charging Off” Uncollectable Debt. 1.6050P-1(b)(2)(i). See IRS Info. 2005–0207, 2005 WL 3561135 (Dec.

Mountain America Federal CreditUnion , the plaintiff became delinquent on a credit card account with her creditunion. The creditunion then assigned the debt to a third-party collection agency. In Hansen v. A copy of the order is available here.

Anyway, back to our core topic of medical debts and credit reporting of medical bills, and here are our own thoughts on this. Reporting all unpaid bills, regardless of the balance, to credit bureaus as the final step does two main things. Wouldn’t this increase the risk of the bank/creditunion with whom he takes that mortgage?

The CFPB has the authority to stretch its long arm as far as the most remote corner of the United States and its territories in order to supervise and audit local banks, creditunions, payday lenders, debt collection agencies, and more. of the inhabitants unemployed. After the pandemic started, that number more than doubled.

Your attorney does this to ensure that the creditors listed as part of your bankruptcy are reporting your debts properly. We want to see for ourselves whether your credit report shows how your debts were treated in your bankruptcy case. We’re Making Sure Creditors Follow the Law. If They Break the Rules, You Can Make Them Pay.

There are 23 types of entities that are exempt from the reporting requirements, including many nonprofits (but not all), banks, creditunions, securities broker or dealer, money services businesses, insurance companies, accounting firms, and most inactive companies (but not all). Where do you file your BOI?

After New York Governor Andrew Cuomo signs the Consumer Credit Fairness Act (S.153/Thomas) 153/Thomas) into law, many creditors will need to provide significant documentation in order to file a debt collection action against their non-paying consumers. We have the experience that pays.

A District Court judge in Utah has denied a defendant’s motion to dismiss in a Fair Credit Reporting Act case, ruling that it did not conduct a reasonable investigation after the plaintiff disputed the debt because both the defendant — the original creditor — and a collection agency were reporting the debt to the credit […] (..)

The bureaus collect and store your credit information in your credit file for future reference. Businesses, such as auto loan lenders, banks, creditunions, credit card companies and insurance agencies—even employers—use your credit data from the credit bureaus to determine your risk level.

Trying to get approved for credit can be a sort of Catch-22: Creditors want proof that you’ve handled a credit card well before, but without a credit card already in hand it can be hard to show you’re a good risk. What Is A Credit Builder Loan.

That means there’s nothing the creditor can repossess and sell to make back some of its loss if you don’t pay the loan. They do tend to be lower than credit card rates, though. The National CreditUnion Administration publishes average rates for different types of investments and loans periodically.

On August 18, the American Financial Services Association, Consumer Bankers Association, CRE Finance Council, Equipment Leasing and Finance Association, Mortgage Bankers Association, National Association of Federally-Insured CreditUnions, Truck Renting and Leasing Association, and the U.S.

” The court held that Merrill Lynch was not a “trustee, receiver, or agent,” and was neither enforcing a lien nor acting for the benefit of the debtor’s creditors. in connection with a securities contract.” ” 11 U.S.C. § § 101(22)(A).

The DCLA exempts banks and creditunions from the licensure requirement while authorizing DBO to bring enforcement actions against such entities for violating existing fair debt collection laws to which they are already subject. The DCLA would also require the DBO to respond to consumer complaints and enforce violations.

When deciding whether to give you a loan or a credit card, lenders and credit card issuers look at your score and credit history. “A A credit score is a number that rates your credit risk. They may agree to a bigger loan or larger credit limit as a result. So what is a soft credit check?” 740 to 799.

The United States Bankruptcy Court for the Western District of Michigan recently issued an opinion in a case that involved mutual claims between the debtor and a creditor, and lifted the automatic stay to allow a creditor to exercise “setoff” rights provided by state law to recover its debt.

First, the CFPB adjusted the asset-size exemption threshold for banks, savings associations, and creditunions under Regulation C, which implements HMDA.

Using a pooled model in addition to bureau scores can help creditors make more precise, value-based decisions at the origination stage. This makes them an ideal solution for banks and creditunions that don’t have enough data to create their own custom models but still want the flexibility to grow their portfolios responsibly.

Banks, savings associations, and creditunions are not subject to HMDA for a calendar year if their assets as of December 31, of the prior calendar year did not exceed an asset threshold. There is an exception to the escrow account requirement for creditors with assets below a certain threshold that also meet additional criteria.

An Illinois federal district court recently denied a creditor-defendant’s motion for summary judgment in a Fair Credit Reporting Act (FCRA) case brought by a consumer who questioned why his debt was being reported twice — as both a tradeline with the original creditor and as a tradeline with a third-party collection agency.

This code means you don’t have any installment loans in your credit history or you haven’t had one active in a while. Creditors like to see that you can handle a mix of revolving and installment loan accounts, and a good credit mix can actually help improve your score. Recently opened bank revolving trades.

Pros: Because you are no longer overwhelmed with creditors and debts, you may be able to save money for secured loans or secured credit cards. Because filing for bankruptcy stops ongoing negative reporting for old delinquent debts, it provides you with a starting point so that you can start to reestablish credit.

In my last blog , we explored why lenders should use analytics beyond single credit scores when making originations decisions. Now, let’s explore another example to see how pooled models can improve bad capture rates across home equity, installment, and revolving credit lines. Bad Capture CreditUnion: BEFORE.

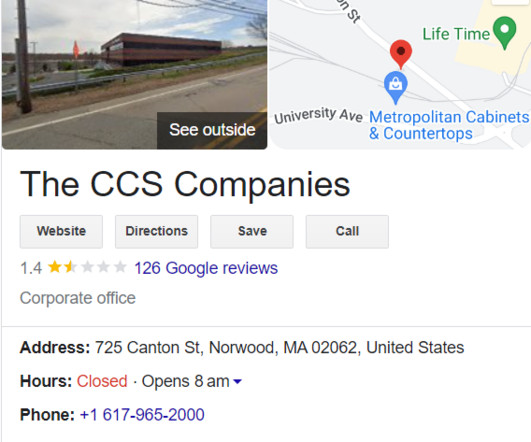

Debt collectors act on behalf of the creditor or a company that has taken on the debt. CCS Offices works as a third-party recovery service for clients seeking to collect unpaid debts from sources such as banks, financial institutions, and creditunions. Who are CCS Offices?

The preliminary injunction order entered by Judge Vyskocil originated out of a putative class action filed by three creditunions — the Greater Chautauqua Federal CreditUnion, the Boulevard Federal CreditUnion, and the Greater Niagara Federal CreditUnion — on April 4 against Chief Administrative Judge Lawrence K.

Cancellation of debt happens when a creditor discharges or forgives a debt you haven’t paid off. The IRS notes that cancellation can occur when the creditor gives up on collecting because it’s exhausted its resources and is unable to collect. In some cases, cancellation can come about as an agreement between you and the creditor.

The HPML provisions in Regulation Z require that a creditor establish an escrow account for certain first lien HPMLs. For applications received before April 1 of the current calendar year, this condition is met if the insured creditor’s assets do not exceed the threshold on December 31 st of either of the two preceding calendar years.

Collectors must provide a written notice explaining the debt—including the amount, the name of the original creditor, and your right to dispute the debt—within five days of contacting you the first time. Use that during negotiations with creditors. Collectors cannot lie to you, harass you, or threaten you. Negotiating Medical Debt.

The Consumer Credit Fairness Act will impact creditors and consumers in the transaction of and collection of New York debt collection and is a clear signal of things to follow. ” Some examples of consumer credit transactions are: Installment loans for the purchase of home furnishings and more. Creditunion loan.

Experian reports that the lowest FICO credit score is 300, but no one really stays at such a low score once some financial history has been established. Experian ’s website indicates that collections of unpaid debt “can stay on your credit report for up to 7 years from the date the debt first became delinquent and was not brought current”.

Owing money to several creditors and remembering when the monthly payments are due for all of them can be overwhelming. And worse, forgetting to pay on time will lower your credit score and cost you more in late payment fees. Consolidating your debt could mean your credit score goes down initially. Debt Consolidation Guide.

Also during the last year, the CFPB, federal banking agencies, and the National CreditUnion Administration (NCUA) cited 174 financial institutions for violations of ECOA and/or Regulation B. Notably, during 2022, the CFPB initiated 32 fair lending examinations or targeted reviews, which represents a 146% increase since 2020.

Exceptions to Credit Card Debt Credit card debt is generally dischargeable in bankruptcy. The Bankruptcy Code assumes this unless the creditor proves misuse. Contract Termination When you file for bankruptcy, it essentially cancels existing credit card agreements. Consider a credit builder loan.

To get a credit card consolidation loan, take the following steps: Step 1: Research lenders, such as creditunions, banks, or online lenders. Since creditunions are not-for-profit institutions, they typically offer the best rates, especially for individuals with poor credit, although you need to become a member to apply.

The three major credit bureaus include Chapter 13 bankruptcy on your report for up to seven years. Of the two options, Chapter 7 has the more negative impact on your creditors. So, financial institutions view you as a higher credit risk. These loans are specifically designed to help rebuild your credit.

No-credit-check lending, such as payday and title loans, often comes with unreasonable fees and annual percentage rates (APR). When seeking a new personal loan after bankruptcy, use legitimate lenders, such as major financial institutions, creditunions, or through Credit Karma. Unsecured loans don’t have collateral.

The court will then order a bankruptcy stay — also called an automatic stay — that prohibits creditors and lenders from collecting what you owe. This plan states that you’re committed to paying back something to creditors in monthly installments, and you detail the minimum amount you’ll pay as well as the duration of the plan.

They are a third-party debt collector, which means that they may be hired by your original creditor, or they may purchase your old debt on the chance that you pay them instead. They are notoriously difficult to work with, and their presence on your credit report can mean trouble for your score in the long run. Hire a Professional.

When a creditor or a government authority sues a business or individual for an unpaid debt, one of the options for settling is for the court to give the creditor the right to pull the funds from a bank account. This debt can include anything from credit cards to past due balances on office space. Writ of Garnishment.

The legislation would benefit banks and creditunions with assets under $15 billion. State Activities: On October 30, Virginia Governor Ralph Northam signed House Bill 568, which automatically exempts emergency relief payments, as defined in the bill, from the creditor process, including garnishments and liens.

CreditUnion , 46 So. This liability is capped at the amount of the amount of the undisbursed loan funds at the time the notice should have been given unless the failure to give notice was done for the purpose of defrauding the contractor. 713.3471(c). As the First District Court of Appeal noted in Whitehead v. Tyndall Fed.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content