This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

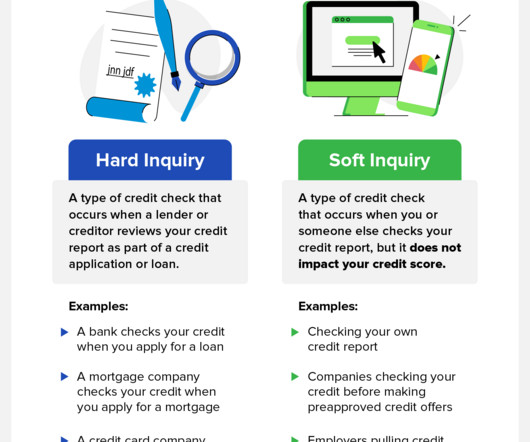

Your credit score is an important aspect of your financial health and is oftentimes used by lenders, landlords, and even employers to determine your creditworthiness. Hard inquiries , also known as hard pulls, are typically made by lenders and other financial institutions and can harm your credit score. What’s a Hard Inquiry?

Governments, charities, and even creditors scrambled to put programs in place to support people during this time while also mitigating future economic fallout. And this isn’t the first time creditors have found themselves working to support borrowers while worrying about their own bottom lines. What Is the FICO Resilience Index?

The Fair Debt Collection Practices Act (FDCPA) does not apply to original creditors or cover company obligations. It mandates that debt collectors post a bond to pay the amount owed to the creditor for whom they are collecting. The federal Fair Debt Collection Practices Act (FDCPA) does not apply to the actual lender.

Similar to a consumer’s credit score, a business’s credit score represents its creditworthiness. Each has its own way of gathering data and scoring your business, but they all look for information from investors, lenders, banks, and credit card issuers. The way this can backfire is that lenders, in general, frown upon this practice.

Yet, whether or not you can do so depends on factors such as the lender’s policies or the type of loan you want to pay off. By now, you probably know that keeping track of your creditworthiness is essential for financial health, and regularly monitoring your credit report can help ensure your credit score is accurate.

And now we can add mortgage lender bankruptcies — and the rise (and fall) of “non-qualified mortgages” — to the factors aggravating an already uncertain market. They’ve previously been touted as an option for creditworthy borrowers who can’t otherwise qualify for traditional mortgage loan programs. Probably not.

This data is supplied by lenders, creditors and businesses where you have accounts. Higher credit scores are more attractive to lenders and creditors. This card offers a process that presents you with a credit line based on your creditworthiness before you apply.

While your score will not drop simply from switching careers or employers, lenders will look at this when determining if you are eligible for opening a new line of credit—and new lines of credit will help you rebuild your score. Maintain a “reliable” income. Moving from one job to the next can indirectly affect your credit score.

Here are the top 6 lenders for the best personal loans with bad credit: PersonalLoans.com. First things first: Do not visit a payday or title lender. PersonalLoans.com is not a lender. It’s a marketplace where you can compare lenders. Access to multiple lenders with one application. BadCreditLoans.com. CashUSA.com.

Plus, these bankruptcy options also provide protection from creditors. Bankruptcies can impact your credit, but you can take steps today to rebuild your creditworthiness. With an unsecured credit card, the lender assumes the risk of lending money to the borrower without any collateral in case the borrower defaults on their payments.

If you fail to pay back your creditor or lender or miss out on instalments regularly, they may resort to a debt collection agency or sell your account to a debt buyer. In fact, once the lender has hired a debt collection agency, you will make payment directly to the agency instead of the original creditor.

A hard credit inquiry is when a credit card issuer or another lender reviews a credit report as part of your credit application. It happens when the lender or bank associated with your credit card company checks your credit report to see if you are eligible for acceptance. They’re also not usually visible to lenders or banks—only you.

This data is supplied by lenders, creditors and businesses where you have accounts. Higher credit scores are more attractive to lenders and creditors. This card offers a process that presents you with a credit line based on your creditworthiness before you apply.

Mortgage lenders will take a look at more than just your credit score, utilizing what’s known as a tri-merge credit report to gauge your credibility. In the guide below, we’ll provide you with all the details you need to know about your tri-merge credit report, how lenders use it, and how you can access the information it contains.

Second, business credit can refer to the creditworthiness of the business as an organization. Lenders, business partners and others can evaluate this worthiness by looking at the business’s credit report and score. And if your business fails, the creditor could come after your personal assets, such as your home.

When a borrower applies for a loan or credit card, the lender will assess their creditworthiness by looking at their income, credit score, and debt-to-income ratio. If the lender is concerned about the borrower’s ability to repay the debt, they may require a co-signer.

Lenders use a multitude of scoring methods to determine your creditworthiness and make decisions about whether or not to give you credit. Having numerical ranges that are somewhat consistent helps make the credit score process less confusing for consumers and lenders. Understanding the Scoring Models.

Owing money to several creditors and remembering when the monthly payments are due for all of them can be overwhelming. Although it doesn’t erase what you owe, debt consolidation allows you to pay off your existing debts to your various creditors immediately. Debt Consolidation Guide. What is Debt Consolidation? Get Some Relief!

Your only job now will be to keep doing what you’re doing to maintain stellar creditworthiness. If you don’t have a card with a high enough limit to keep you comfortably under 25% utilization, give the creditor a call and request that they up the credit limit. Keep reading to learn ways to fine-tune your credit life.

It’s how lenders measure an organization’s available cash flow to pay off debt obligations, essentially a credit score for a business. This matters because creditors use this information to determine whether to do business with the U.S. Like personal credit scores, DSCR ratios are calculated differently by different creditors.

The CFPB discovered that some mortgage lenders violated ECOA by discriminating against African American and female borrowers in the granting of pricing exceptions based on competitive offers. Some of the key findings in the Fall 2021 Supervisory Highlights include: Fair Lending. Payday Lending.

Lenders are more willing to approve a car loan with a cosigner because it reduces the risk of nonpayment. The lender uses this information to check their creditworthiness when considering the loan. This may help you get the car you want by lowering the risk to the lender. This step could be less risky for the lender.

of specific reasons for denying credit applications, even if they use complex algorithms to determine creditworthiness. The Consumer Financial Protection Bureau recently warned companies that, under federal anti-discrimination laws, they still owe consumers an explanation.

Since payment history is the most important factor that influences your creditworthiness, not making payments on time can damage your credit score. Keep in mind that some lenders charge an up-front, one-time origination fee ranging from 1% to 10% of the total loan amount. Step 2: Get prequalified with a couple of lenders.

You gain a complete picture of your economic landscape by documenting each debt, including the creditor, outstanding balance, interest rate, and minimum monthly payment. Reach out to your creditors and explore the possibility of negotiating a lower interest rate.

Most lenders, though, don’t offer lower rates for having the highest credit score on a scoring model. There’s little difference between an 800 and 850 in the eyes of a lender when determining your creditworthiness. You can always ask if the creditor can increase your limit without that step. Limit Your Credit Use.

Credit.com’s free credit report card tool can help you better understand your current creditworthiness and which factors you need to work on to help you improve your standing. You make one monthly payment to that agency, and the agency disburses that payment among your creditors.

The proposed rule would require lenders to assess a borrower’s ability to repay a PACE loan and would provide a framework for how these loans will be treated under the Truth in Lending Act. PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels.

If you can get approved for credit, you might face higher interest rates, loan denials, or even higher security deposits for rentals since you’ll be seen as less creditworthy to lenders. They can help you get out of debt , create a budget, negotiate with creditors, and develop a strategy to repay your debts.

It finalized, it would: Remove exceptions that let lenders use information about medical debt to make determinations about someone’s creditworthiness. Prohibit credit reporting agencies from including medical debt on credit reports sent to creditors if the creditor is prohibited from considering it.

As 2023 begins, it is clear many lenders are at a metaphorical fork in the road when it comes to devising smart, agile collections strategies that will safeguard their customers and cement long-term loyalty, simply by helping them ride out the impact of the ongoing squeeze on household incomes.

She further highlighted two common trends the DOJ is seeing in redlining enforcement actions: lenders’ awareness of redlining risks, sometimes for years, without taking corrective action; and evidence of discrimination in employee or manager emails, i.e., disparaging descriptions of certain neighborhoods or overt animus towards protected groups.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content