This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Borrowing money costs more when you have bad credit — and your choices for a loan will be limited — which is why we have helped you narrow down your list by finding the top 6 best personal loans for bad credit. Use this time to fix your credit before applying for loans. 6 Best Personal Loans for Bad Credit.

When you miss too many payments, your creditor may charge off the debt. According to the Federal Reserve, consumer loans had a charge-off rate of around 2.3% A charge-off occurs when you don’t pay the full minimum payment on a debt for several months and your creditor writes it off as a bad debt.

Your credit score is an important aspect of your financial health and is oftentimes used by lenders, landlords, and even employers to determine your creditworthiness. Whether you’re applying for a loan or simply want to stay on top of your credit score, these tips will help you access your credit information without causing any harm.

Similar to a consumer’s credit score, a business’s credit score represents its creditworthiness. Trade credits are loans extended in B2B agreements between a supplier and a business, based on a buy-now-pay-later arrangement. Even if you pay off a loan or a business credit card, keep it there. Maintain old accounts.

Consumer debts include credit card debts, vehicle loans, medical costs, and school loans. The Fair Debt Collection Practices Act (FDCPA) does not apply to original creditors or cover company obligations. It mandates that debt collectors post a bond to pay the amount owed to the creditor for whom they are collecting.

Governments, charities, and even creditors scrambled to put programs in place to support people during this time while also mitigating future economic fallout. And this isn’t the first time creditors have found themselves working to support borrowers while worrying about their own bottom lines. What Is the FICO Resilience Index?

Can you pay a loan with a credit card? Yes, paying a loan with a credit card is sometimes possible. Yet, whether or not you can do so depends on factors such as the lender’s policies or the type of loan you want to pay off. However, this does not influence our evaluations.

When you have a great credit score , you can get lower interest rates on car loans, credit cards and mortgages. This data is supplied by lenders, creditors and businesses where you have accounts. Higher credit scores are more attractive to lenders and creditors. Get a Loan. Make Payments on Time.

There is life after bankruptcy, and you can open new lines of credit and take out loans again after you get back on your feet. Though it can be a challenge to open new credit cards or take out new loans after a bankruptcy, it is not impossible, and this is essential to rebuilding your credit. Open new lines of credit.

When you have a great credit score , you can get lower interest rates on car loans, credit cards and mortgages. This data is supplied by lenders, creditors and businesses where you have accounts. Higher credit scores are more attractive to lenders and creditors. Get a Loan. Make Payments on Time. Keep It Simple for Now.

These include transferring all your debt onto just one credit card as well as taking out a secured or unsecured personal loan—perhaps with the help of a professional debt consolidation company. Owing money to several creditors and remembering when the monthly payments are due for all of them can be overwhelming.

For example, Danny needs a high credit score within the month to be approved for a mortgage loan. Danny is now eligible to apply for a loan because his score is high enough. FICO were feeling that any consumer was able to boost his or her credit, regardless of their creditworthiness. How Is It Done?

I couldn’t get a credit card, let alone a mortgage loan. Good Credit (680 – 719): This is a good credit range to be in, but you won’t get the very best rates on loans or credit cards. You can still qualify for most FHA mortgage loans, for example. You Need a Mortgage Loan. Pay Down All Installment Loans.

Co-signers are beneficial for those seeking to obtain loans and credit cards. Obtaining Personal Loans with a Cosigner Having a co-signer on a personal loan or credit card means that you associate another individual with your debt. Additionally, having a co-signer may enable you to secure more favorable interest rates.

Plus, these bankruptcy options also provide protection from creditors. Although bankruptcy can help you overcome debt, it will negatively impact your credit score, making it more challenging to obtain credit cards, loans, and other financial products. An unsecured credit card does not require collateral to obtain approval.

Lenders use a multitude of scoring methods to determine your creditworthiness and make decisions about whether or not to give you credit. Your score may also differ across the credit bureaus because your creditors aren’t required to report to all three. Understanding the Scoring Models. Variations in Scoring Requirements.

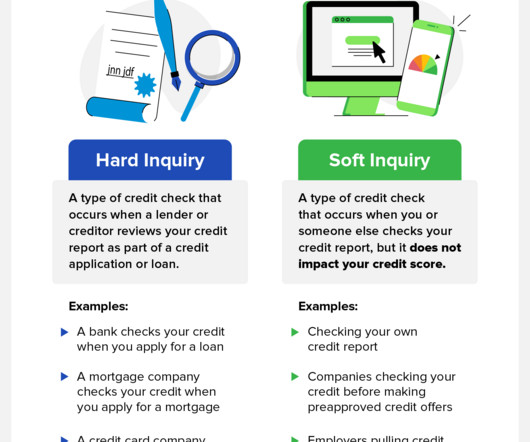

Creditors want to see that you can manage different types of accounts, such as revolving and installment accounts. Only those that evaluate your financial creditworthiness do—these are hard credit checks. Research the creditor that authorized the hard inquiry. Credit age accounts for around 15% of your score.

This includes credit card balances, student loans, medical bills, and other outstanding obligations. You gain a complete picture of your economic landscape by documenting each debt, including the creditor, outstanding balance, interest rate, and minimum monthly payment. Of course, implementing this step is easier said than done.

Second, business credit can refer to the creditworthiness of the business as an organization. They’re certainly less likely to loan your business money. First, if you take out personal loans to pay for business expenses, you’re wholly liable for the debt. That’s right. Business Credit Agencies.

If you’re having trouble getting a car loan, using a cosigner could help. Before you take this step, it’s important to understand what a cosigner is and how having one on your car loan works. A cosigner is a person, usually a close friend or family member, who agrees to be responsible for repaying your car loan if you fail to do so.

When you apply for a mortgage, your credit history will play a major role in deciding the type and amount of home loan you’re eligible for. The majority of lenders use your FICO score when you apply for a loan, but a small percentage of lenders use a different model, like the VantageScore.

Having good credit can help you secure better loans. Credit.com’s free credit report card tool can help you better understand your current creditworthiness and which factors you need to work on to help you improve your standing. On the other hand, adding a loan or credit card to your credit history could improve your credit mix.

This matters because creditors use this information to determine whether to do business with the U.S. Failure to calculate an organization’s DSCR, rather than relying on income statements, can lead a creditor holding the bag when a company collapses and defaults on its obligations. For perspective, the U.S. Treasury Department.

Since payment history is the most important factor that influences your creditworthiness, not making payments on time can damage your credit score. Generally speaking, you will take out a loan or credit card with a lower interest rate and pay off all current balances with money from the new account.

Examiners also discovered that some servicers incorrectly disclosed transaction and payment information in borrowers’ online mortgage loan accounts. The Bureau also discovered that credit card issuers misled consumers who responded to advertisements offering incentives for opening a new account and spending a minimum amount.

NQMs use non-traditional methods of income verification and are frequently used by those with unusual income scenarios, are self-employed or have credit issues that make it difficult to get a qualified mortgage loan. Today’s NQMs are largely considered safer bets than the ultra-risky loans that helped fuel the 2008 meltdown.

On May 1, the CFPB proposed a rule to implement a congressional mandate to establish consumer protections for residential property assessed clean energy (PACE) loans. PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels.

Do not let the weight of post-bankruptcy credit challenges stop you from financial freedom Filing for bankruptcy is undoubtedly a challenging decision, one that can have a significant impact on your financial stability and creditworthiness. Community banks and credit unions frequently offer credit-builder loans at reasonable interest rates.

There’s little difference between an 800 and 850 in the eyes of a lender when determining your creditworthiness. You can always ask if the creditor can increase your limit without that step. Most lenders, though, don’t offer lower rates for having the highest credit score on a scoring model. How Your Credit Score Is Calculated.

Installment loans. If a creditor, retailer, or service provider is unable to collect on your debts, they may either sell it to an agency like ARI or hire them for assistance. In addition to diminishing your creditworthiness, having debt in collections can make your everyday life pretty stressful. Credit card debt. Retail debt.

Installment loans. If a creditor, retailer, or service provider is unable to collect on your debts, they may either sell it to an agency like ARI or hire them for assistance. In addition to diminishing your creditworthiness, having debt in collections can make your everyday life pretty stressful. Credit card debt. Retail debt.

The statute of limitations also depends on the type of debt that is owed—here’s a breakdown of the different types of debt : Written contracts: These are repayment term agreements that are signed by the borrower, like mortgages and loans. Debt consolidation lets you combine them into one loan with (hopefully) a lower interest rate.

One of their key proposals is that the government and FCA introduce clear limits on the number of times that creditors can contact people in debt. The MMHPI paper can be found here. FCA shares update on debt packager proposals. The FCA has provided an update on its debt packager proposals, which it consulted on in November 2021.

In a statement, the CFPB said medical bills “have little to no predictive value when it comes to repaying other loans.“ Medical debt can still have significant financial consequences, though, leaving you with fewer options for housing, loans and credit cards. The following year, they stopped including outstanding balances under $500.

No matter what the balance is, there’s a reason it hasn’t been paid and it’s probably smart to talk to the potential client and see if there might have been other circumstances interfering with their ability to pay back their creditor.

No matter what the balance is, there’s a reason it hasn’t been paid and it’s probably smart to talk to the potential client and see if there might have been other circumstances interfering with their ability to pay back their creditor.

Lenders can access reportswith consumer permissionto evaluate someone for a loan or other financial opportunity. Tradelines include credit cards, bank accounts, mortgage lenders, and other creditors. Hard inquiries occur when a lender checks your credit report as part of the process of evaluating you for a loan or other credit.

In February 2022, the DOJ joined the Consumer Financial Protection Bureau (CFPB), the Department of Housing and Urban Development, and prudential regulators in an interagency statement encouraging creditors to explore opportunities to develop special purpose credit programs (SPCPs) to better expand access to credit.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content