This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Skip tracing techniques allow agents to track down debtors that have “skipped” out on their debts and are no longer reachable. Debtors Are More Likely to Pay A Collection Agency. When a debt passes from the originalcreditor to a collection agency, this escalation often makes debtors pay attention.

Skip tracing techniques allow agents to track down debtors that have “skipped” out on their debts and are no longer reachable. Debtors Are More Likely to Pay A Collection Agency. When a debt passes from the originalcreditor to a collection agency, this escalation often makes debtors pay attention.

Several collection agencies have been using electronic mediums like emails, social media platforms, and SMS to contact debtors. To a standard person, it may appear that contacting a debtor either way (traditional or electronic) is the same, a contact made is a contact made regardless of the medium. In fact, many prefer it that way.

By law, all debt collectors are required to provide at least 30 days to the debtor/consumer to dispute the debt, after the consumer receives (or is assumed to receive) the validation information. I want you to send me the name and address of the originalcreditor. The amount is wrong.

Say you are a collection agency, and your client (the originalcreditor) contacts you to tell that they have received a complaint from the debtor telling that your debt collector was very rude over the phone or felt threatened. Such complaints from debtors can get your client to worry about their reputation.

Is there a law in NYC that protects consumers and debtors from debt collecting agencies, businesses, and their attorneys? Overview of NYC Law on Debt Collection Most people might not be aware of it, but New York has some of the strictest regulations and laws regarding debt collection and debtor protection.

The Fair Debt Collection Practices Act (FDCPA) does not apply to originalcreditors or cover company obligations. It mandates that debt collectors post a bond to pay the amount owed to the creditor for whom they are collecting. Under the UCCC, consumers can take legal action against debtors. Repeatedly call you.

It does not come into play for creditors collecting their own debts. The name of the originalcreditor to whom the debt is owed. The law: Collectors can call third parties such as family members, neighbors, friends, or co-workers only once to locate the debtor. State laws may provide additional protection.

While a debt collector contacting you can be stressful, it’s important to pause and remember your rights as a debtor. Debt Verification Letter Template + Sample How Long Does a Creditor Have to Respond to a Debt Verification Request? The creditor should send a debt validation within five days of their initial contact with you.

Request the following from the debt collector via certified mail: The amount and age of the alleged debt: Ask for a copy of the last billing statement sent by the originalcreditor, the amount of debt when the collector obtained it, and if there have been any payments or reductions since the original billing statement.

Due to this, the originalcreditors will reach out to you to obtain their due payments. A common and effective debt collection tactic, this type of lawsuit usually goes after commercial debtors to collect on commercial debt, the money you owe in addition to interest, as well as potential court and attorney fees.

Before someone makes a bankruptcy filing, it is not uncommon for debtors to feel as if they have to make some tough decisions. Which creditors can they pay? This typically occurs because the debtor doesn’t have the money to pay all of their creditors, so they feel they need to rank which ones are more important to pay first.

Equifax, one of the largest credit reporting agencies in the country, says creditors transfer or sell debt to collection agencies when they believe they are unlikely to collect the money. These sales are often done for a fraction of the amount owed so the creditor can recover some of the money.

Sometimes, such agencies act as intermediaries to collect delinquent debts from customers at least 60 days past and remit them to originalcreditors. Your collector will typically convey the following details to your debtors: Name of the originalcreditor Amount of debt What to do if your debtor thinks it is not a valid claim.

Courts apply the very pro-consumer “least sophisticated debtor” standard when evaluating a collector’s communications, and most violations of the Act are “strict liability” – meaning the debtor can win the case without proving the collector intended to violate the statute.

Therefore, if an agency works for an originalcreditor, the creditor pays off the debt collector a specific percentage of the collected debt. Debt collection agencies and debt collectors often use file information to contact your debtors. The amount debtors owe (including late fees and other charges).

In doing so, it held that a collection letter, which indicated that the debtor could only dispute the underlying debt in writing, violated the FDCPA. Emphasis in the original). On appeal, the Ninth Circuit held that a debt collection letter that expressly states that the debtor must dispute a debt in writing violates the FDCPA.

most people tend to think of a debt collector trying to contact debtors about some unresolved debts. It usually depends on the company collecting a debt, how much you owe your debtors, and the type of debt your business has. The name of the originalcreditor. They will contact your debtors only between 8 a.m.

The full name of the creditor. A statement that the debt collector will provide to the consumer, within 30 days, the name of the originalcreditor if different than the debt collector. If a company manages a large volume of consumer debt, it takes considerable resources to follow up with each debtor in writing.

Creditors give loans to millions of citizens, and thus credit companies are too busy to follow up on the debtors. For this reason, creditors are hiring debt collection agencies to collect debts that are 60 days past the agreed period. Debt collection agencies communicate to debtors via calls, letters, or emails.

Establishing Contact with the Debtor The first step in the debt collection process is establishing contact with the debtor. This often involves several key actions: Initial Communication: A business or a debt collection agency, like a debt collection agency in Derby, will send a letter of demand to the debtor.

Having debts in the collection primarily means that a third party is pursuing you to retrieve payments for your debts on behalf of your creditors. Debt collection is a process that gives debtors certain rights that debt collection agencies must respect. What does it mean to have debt in collections? Taurus Collections (UK) Ltd.

Overview of The Credit Card Debt Collection Process Credit card debt collection can be a stressful experience for both the debtor and the creditor. The process begins when the debtor stops making payments on their credit card and goes into default. The creditor then hires a debt collection agency to start the collection process.

Further, if you make a written request upon this office within THIRTY (30) days of receiving this notice, this office will provide you with the name and address of the originalcreditor, if different from the current creditor. This is an attempt to collect a debt and any information obtained will be used for that purpose.

Myths About Using a Collection Agency: Paying the OriginalCreditor to Bypass Agencies. Many people believe they can get around dealing with debt collection agencies by paying their originalcreditors directly. However, the FDCPA only protects consumer debtors.

If you’re a collection agency or creditor in New York, you need to be keeping an eye out for Senate Bill 3803. This bill was introduced to the state senate in February of this year, and the crux is that if approved, debt collectors would be prohibited from using social media to contact debtors. Who Does This Affect?

A commercial debt collector works exclusively with B2B creditors that need to collect past due payments from other businesses. Negotiate payoff balances: In some cases, B2B creditors might authorize commercial debt collectors to make payment arrangements with their clients. What Do Commercial Debt Collection Agencies Do?

Simply put, it’s an individual or a debt collection agency in the UK employed by a creditor to retrieve funds that are overdue. A debt collector is an entity, often a third-party agency, hired by creditors to recover funds that are past due or accounts that are in default. So, what exactly is a debt collector?

Under the Act, if you challenge an item on your credit report and the creditor or credit reporting agency can’t verify the item’s accuracy, the act requires the unverified item be confirmed or removed from your credit report. It may even appear twice on the report from the originaldebtor and the debt collector.

Section 1788.202 prohibits a private education lender or a private education loan collector from making any written statement to a debtor in an attempt to collect a private education loan unless the private education lender or private education loan collector possesses specified information, including 18 items.

If you previously had consent (for example to the phone number that was provided to the originalcreditor), and that consent is withdrawn, it was likely done in an attempt to set up an action under the Telephone Consumer Protection Act. 6) The resurrected debtor. 3) Withdrawal of consent. But, there are FDCPA implications.

Each state has a law referred to as a statute of limitations that spells out the time period during which a creditor or collector may sue borrowers to collect debts. It means the creditor or collector can’t use the legal system to force you to make good on the debt. The creditor closes your account.

Section 1692g of the FDCPA says collectors must provide notice to consumers within five days of the initial communication regarding the debt, stating the amount of the debt, the name of the current creditor, and explaining the consumer’s right to dispute the debt and to obtain verification. See 15 U.S.C. 1692g(a)(1), (2). 1692g(a)(5).

Creditors usually send several notices prior to filing a complaint with the court. In fact, the creditor will need to show the court its attempts at collecting the debt and its notice of intent to sue in order to prove its case. There are two other conditions that must be met for a creditor to serve papers on a debtor.

They should also provide information about the debtor’s right to dispute the debt. As a debtor, you have the following rights: Right to Privacy: Debt collectors are not allowed to share information about your debts with anyone else except your attorney or the originalcreditor.

Even originalcreditors, who are not subject to the FDCPA, are being drawn into FDCPA litigation under various theories of recovery. For this reason, originalcreditors are not subject to the FDCPA (except in very limited circumstances). Retrieval Masters Creditor Bureau, Inc. , See, e.g., Perry v. Goodman , 200 F.3d

Upon being hired by a client, Southwest Credit Systems acquires the debt at a discounted rate from the originalcreditor. Southwest Credit Systems Reviews Like many other debt collection agencies, Southwest Credit Systems employs forceful methods to persuade debtors to pay off their debts.

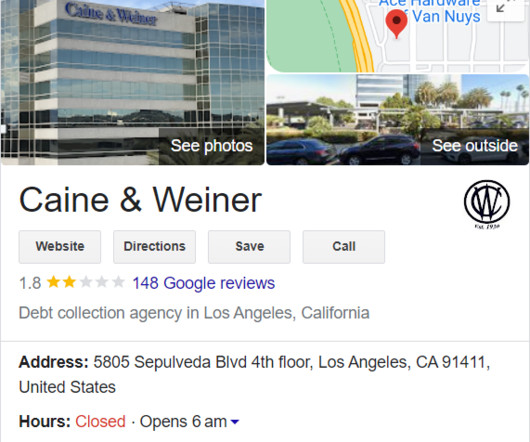

Caine and Weiner is a prominent debt collection firm that operates across various sectors, gathering debts from a range of industries, including: Personal loans Phone bills Student loans Credit cards To secure his debts, Caine and Weiner acquire them from the originalcreditors at a reduced price, then pursue the entire amount from the debtor.

For example, the following are still requirements to bring a lawsuit: The original account number, originalcreditor, the total amount claimed, an itemization of post charge?off off payments or credits (where applicable), the charge?off

Keep in mind, the FDCPA gives you the right to ask any collection agency to provide you with a detailed account of how the total debt amount was calculated and the name of the originalcreditor. You may still find the original law and the new regulation complicated and lengthy.

One method for identifying areas of potential concern, however, is to analyze the recent enforcement actions by the CFPB and other regulators filed against debt buyers and originalcreditors. Enforcement actions filed against originalcreditors can also provide guidance to debt buyers and other collectors about areas of CFPB concern.

The Court of Appeals held that this publication of notice “qualifies under the FDCPA as an ‘initial communication’ with the debtor.”. Both the text of the FDCPA and the applicable case law make it clear that Section 1692g does not provide a grace period.

You will also want to evaluate all third party interactions that your firm engages in, such as contacts with relatives of the debtor, co-workers, interactions with consumer reporting agencies, and the procedures of the vendors that your firm employs, such as process servers. Fulton, Friedman & Gullace, LLP, 825 F.3d 3d 317 (7th Cir.

The proposed amendments include changing the definition of medical debt, allowing medical debtors to initiate contact and make voluntary payments, and preventing certain written communications from being sent via certified mail. Previously, Khan served as a legal advisor to former FTC Commissioner Rohit Chopra.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content