This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you’re a creditor or collector working with financially distressed borrowers, considering consumer situations and preferences when attempting to collect and employing digital strategies to boost engagement are more important than ever. There were also a couple of notable court decisions impacting debt collectors last quarter.

When account owners have an account that reflects a negative balance, the lender is faced with a myriad of options and obligations with regard to the pursuit of that debt. Lenders that charge off a debt trigger issuance of the 1099-C when their defined policy leads the lender to discontinue collection activity and discharge a debt.

Providing inaccurate explanations to consumers as to why the creditor denied the consumers’ billing error claims in whole or part. The CFPB reports that this seems to happen most often with creditors’ acquisitions of pre-existing credit card accounts from other creditors. Debt Collection. Too many holds on mobile check deposits.

In that context, lenders need to have access to state-of-the-art technology to avoid major losses. A solution that will enable creditors to quickly do analyses of a vast amount of data from multiple sources; have access to insights about delinquency status, and ways to efficiently manage customers that default. The problem.

Providing inaccurate explanations to consumers as to why the creditor denied the consumers’ billing error claims in whole or part. The CFPB reports that this seems to happen most often with creditors’ acquisitions of pre-existing credit card accounts from other creditors. Debt Collection. Too many holds on mobile check deposits.

While creditors weren’t looking up someone’s history of debt and payments, many lenders did take risk-mitigation actions. Creditors want to know if a person is a good “bet.” It also impacted some people’s ability to get credit with new lenders. The concept of credit reporting may be almost as old.

Changing customer behavior due to the deterioration of their financial circumstances have led to an uptick in debt and collections activities as well. To navigate through uncertainty, creditors need to adapt their strategy quickly. In that context, analytics can bring true value for lenders. How can this be achieved in practice?

Changing customer behavior due to the deterioration of their financial circumstances have led to an uptick in debt and collections activities as well. To navigate through uncertainty, creditors need to adapt their strategy quickly. In that context, analytics can bring true value for lenders. How can this be achieved in practice?

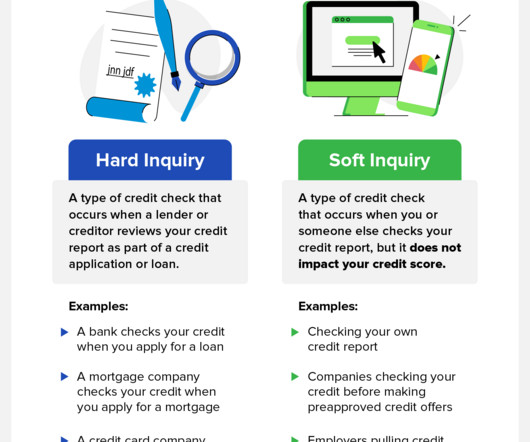

Your credit score is an important aspect of your financial health and is oftentimes used by lenders, landlords, and even employers to determine your creditworthiness. Hard inquiries , also known as hard pulls, are typically made by lenders and other financialinstitutions and can harm your credit score.

In which case, a Creditors’ Voluntary Liquidation (CVL) is preferable to a compulsory one. Once passed, the liquidator distributes company assets to creditors, fulfilling debts wherever possible. There is a set hierarchy dictating which creditor category receives repayment first, as per the Insolvency Act 1986.

Banks are accelerating their adoption of new digital debt collection tools in anticipation of a “tidal wave of consumer debt issues” when government stimulus programs end and financialinstitutions stop offering forbearance and loan deferral options. About TrueAccord.

Lenders face a myriad of challenges these days. Using a pooled model in addition to bureau scores can help creditors make more precise, value-based decisions at the origination stage. A pooled model is a scoring model built on “pools” of historical data from many financialinstitutions. What Is a Pooled Model?

These negative marks on your credit report indicate you might not pay your bills on time—or ever, which is why lenders don’t like to see them. Learning how to remove collections from your credit report can help you clean up your credit history and open better financial doors in the future. Do you recognize the listed lenders?

Customers are becoming more sophisticated and the same goes with the solutions they expect from financialinstitutions. Overall, customer analytics is the answer to the creditors quest to reach new heights since that will lead to refined customer experiences and ultimately, to higher debt collection rates. Increased cash flow.

Managing loan portfolios becomes a labyrinth for financialinstitutions in a financial ecosystem marked by unrelenting complexity and constant change. Consequently, financialinstitutions operate within an economy marked by contraction and sustained inflationary pressures.

One of the aspects of the proposed rule that changed dramatically when the Final Rule was issued was a series of new provisions and sections of the Official Commentary prohibiting small business lenders from discouraging applicants from providing the data required to be collected by the Final Rule.

In addition, he serves as the Atlanta Office Managing Partner while practicing in the firm’s Creditors’ Rights and Bankruptcy and Lending Practice Groups. Hall was named in the Bankruptcy & Creditors’ Rights, including Litigation specialty. Golden was named in the Bankruptcy & Commercial Litigation specialty.

By communicating at the right time in the right channel with payment options that meet consumer needs, TrueAccord provides exceptional recovery rates for top 10 financialinstitutions, debt buyers, lenders and technology companies.

The global economic turmoil over the past months has pushed the financial industry into uncharted waters. The number of customers likely to face distress constantly increases and creditors are at the crossroads. What do the EBA guidelines about EWS suggest? What are the challenges?

Financialinstitutions, for example banks, will normally seek some kind of security when lending money. What unifies these types of fixed charges is the control the lender has over them. Should a business want to sell a fixed asset, they will have to seek approval from the lender – or have already resolved all outstanding debts.

Additionally, lenders may hesitate to lend to you if there is a bankruptcy on your credit report. Of the two options, Chapter 7 has the more negative impact on your creditors. So, financialinstitutions view you as a higher credit risk. Yet, the end result will often still be a very low credit score.

Those were just two of more than 1,800 loans that went to debt collectors and high-interest lenders through the Paycheck Protection Program, according to an analysis by The Washington Post. Payday lenders, strip clubs vie for PPP loans. a group of strip clubs in Wisconsin, a lobbying group and a payday lender.

Secured credit cards are different because rather than borrowing from a financialinstitution, you borrow from yourself. When you have a cosigner with a good credit score, the lender sees loaning to you as less of a risk because the cosigner is also attached to the loan.

This section of your credit report tells potential lenders who you are. If you see an old phone number, chances are it is still on file with the financialinstitution that issued the loan or credit card. Your creditors will report on your credit accounts regularly. Contact the creditor directly. Credit Information.

Customers are becoming more sophisticated and the same goes with the solutions they expect from financialinstitutions. Overall, customer analytics is the answer to the creditors quest to reach new heights since that will lead to refined customer experiences and ultimately, to higher debt collection rates. Increased cash flow.

This article aims to shed light on what pre-screen firm offers entail, their significance, and how debt consolidation lenders acquire your information to send those enticing marketing mailers. Two entities that may send debt consolidation loan mailers are Symple Lending and Secure One Financial. How does the Pre-Screening Process Work?

The Saudi Credit Bureau (SIMAH) , a leader in credit bureau information management in the Middle East and North Africa (MENA), has administered the successful rollout and adoption of the FICO® Score by lenders in the country, enabling millions more Saudi customers to receive loans from banks. Analytics Tailored To The Market.

According to the CFPB, “[w]hile the nature of overdraft services, including how accounts can be overdrawn and how financialinstitutions determine whether to advance funds to pay the overdrawn amount, has significantly changed since 1969, the special rules [contained in Regulation Z] remain largely unchanged.”

Types of personal loans include: Installment Plan Payday Peer-to-Peer Lending Cosigner /Guarantor Debt Consolidation Variable Rate Fixed Rate During your bankruptcy proceeding, at least a portion of these loans will be discharged, whether you borrowed from brick-and-mortar or online lenders. Unsecured loans don’t have collateral.

A creditor with a claim must often take affirmative action by filing a “proof of claim” form in order to preserve and protect its rights to payment. Even when a claim is scheduled, and assuming there are no reasons not to (see below), a creditor may choose to file a claim to guard against a debtor modifying or removing its scheduled claim.

When youre late on payments or stop making payments on a loan, the lender can repossess or repo the item youre financing to settle your debt. Negotiate with Lender Step 5. When you fail to make payments on time or stop making payments altogether, the lender may demand that you surrender the item. Dispute Inaccuracies Step 4.

The COVID-19 pandemic cast a huge shadow on the financial services worldwide. The FICO Blog posts last year reflected that – we wrote about everything from the impact on collections, proactive lender communications with consumers, issues with fraud, and of course, how FICO® Scores were impacted.

We talked to finance and credit card experts to get their insight into why lenders care so much about credit, and what you can do to get a good credit score or fix a bad one. Simply put, lenders will use this number to make a determination about how likely you are to pay back a loan, based on your history of paying off your credit cards.

What happens to a business that enters into a financial transaction with another party? How can lenders feel confident in approving businesses for loans or leasing? The financialinstitution or lender would file for a UCC and place a lien against the party to which they are lending money.

The CFPB discovered that some mortgage lenders violated ECOA by discriminating against African American and female borrowers in the granting of pricing exceptions based on competitive offers. Some of the key findings in the Fall 2021 Supervisory Highlights include: Fair Lending. Prepaid Accounts. Payday Lending.

“Banks, credit unions, and financialinstitutions use credit scores and other factors of your credit history to determine the borrower’s ability to repay the loan,” says David Haas, co-founder of PowerPay , a financial technology company that provides loans for home improvement projects.

“Banks, credit unions, and financialinstitutions use credit scores and other factors of your credit history to determine the borrower’s ability to repay the loan,” says David Haas, co-founder of PowerPay , a financial technology company that provides loans for home improvement projects.

Establish connections with individuals and businesses that can refer clients to your agency, such as attorneys, financialinstitutions, credit bureaus, or other professionals in the debt recovery field. Networking and referrals: Build a strong professional network within the industry.

No matter what or when, contact your lender if you believe you will be unable to make a student loan debt payment. Lenders are usually very open to figuring out a payment plan. It’s a primary way lenders measure a consumer’s ability to manage any money they plan to borrow, whether for a mortgage, vehicle, or other.

When a creditor or a government authority sues a business or individual for an unpaid debt, one of the options for settling is for the court to give the creditor the right to pull the funds from a bank account. That means, even if the account is in the company’s name, a creditor or the IRS can place a levy on the assets.

When the Federal Reserve raises interest rates, financialinstitutions increase their rates accordingly, so those with variable interest rate loans may need to pay more interest than when they initially borrowed the money. Make On-Time Monthly Payments: You need good financial health to obtain lower interest rates.

Hard Inquiries When you apply for credit, you give the financialinstitution permission to pull your credit report so that it can decide whether or not to approve you. That means you’re less likely to be able to pay your bills on time and as agreed, so you’re a bigger risk to creditors.

Many bankers and lenders insist that fees they charge are related to specific types of work or services performed, and existing laws and regulations already prohibit excessive fees, so it isn’t clear what problem the inquiry is designed to solve.

A recent decision from a Louisiana district court should provide some comfort to banks and other financialinstitutions who acquire other entities by merger – at least in the Fifth Circuit, they are not debt collectors. As most know, Bank of America (BoA) acquired Countrywide Bank FSB and its mortgage portfolio in 2008. In Jackson v.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content