This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A New Jersey Appeals Court has affirmed a lower court’s ruling denying an individual’s motion to vacate a default judgment obtained in a collection lawsuit, agreeing that the individual chose to wait too long to file the motion to vacate. The background: The case at hand involves a collection action initiated by the plaintiff.

Is it possible for an individual to sue a debt collector for violating the Fair Credit Reporting Act and Fair Debt Collection Practices Act for allegedly attempting to collect a debt that the individual believes he did not owe, when the individual took no action against the originalcreditor for placing the allegedly illegitimate debt … The post (..)

The judge determined that it followed its procedures for investigating disputes, which included contacting the originalcreditor to confirm the debts validity. Thus, the court concluded that NCSs investigation was not unreasonable as a matter of law. Learn more.

A Magistrate Court judge in New York has awarded the attorneys representing a plaintiff in a Fair Debt Collection Practices Act $11,297 in fees, after the plaintiff accepted an offer of judgment in the amount of $1,050 over a $59 debt that was owed to the originalcreditor.

A District Court judge in Illinois has granted a defendant’s motion for summary judgment in a Fair Debt Collection Practices Act case involving how the defendant, and the originalcreditor, came to be in possession of the plaintiff’s husband’s Social Security number.

More bankruptcies mean higher charge-offs for creditors and increased reliance on third-party collection agencies. Translation: to CYA, you need better originalcreditor contracts.] WHAT THIS MEANS, FROM LAURIE NELSON OF PAYMENT VISION: The surge in bankruptcy filings in 2024 presents both challenges and strategic opportunities.

the creditor wins the lawsuit, you may face serious financial repercussions. Failing to respond can result in default judgment, allowing the creditor to take action by seizing your assets or withholding your wages. H3: Negotiate a Settlement Another option is to discuss a settlement with the creditor or debt collector.

WHAT THIS MEANS, FROM MITCH WILLIAMSON OF BARRON & NEWBURGER: There are two interesting aspects of this case which a debt buyer sought to enforce an arbitration agreement contained in the original cardholder agreement. The “merger principle merely extinguishes that specific claim that was adjudicated and replaces it with a final judgment.”

Legal Action : The creditor or collection agency may file a lawsuit against you to recover the debt. If you ignore this or fail to defend yourself in court, a default judgment may be issued against you. This can lead to wage garnishment, bank levies, or liens against your property. this can still lead to embarrassment or social stigma.

How to Open a Bank Account That No Creditor Can Touch. In truth, it’s fairly rare to have a bank account that no creditor can touch. Depending on the legal situation, that could protect funds in the accounts from your creditors. The originalcreditor takes some actions to collect, sending you bills and statements.

District Court for the Southern District of California, granting summary judgment in favor of a debt collector in a Fair Debt Collections Practices Act (FDCPA) case. Emphasis in the original). Krieger , No. 21-55275 (9th Cir. 24, 2022) , the Ninth Circuit partially reversed a decision by the U.S.

The Fair Debt Collection Practices Act (FDCPA) does not apply to originalcreditors or cover company obligations. It mandates that debt collectors post a bond to pay the amount owed to the creditor for whom they are collecting. Consumer debts include credit card debts, vehicle loans, medical costs, and school loans.

It does not come into play for creditors collecting their own debts. The name of the originalcreditor to whom the debt is owed. Sometimes, collectors may be allowed to make a claim if they have taken the consumer to court and received a court-approved judgment. State laws may provide additional protection.

An Illinois federal district court recently denied a creditor-defendant’s motion for summary judgment in a Fair Credit Reporting Act (FCRA) case brought by a consumer who questioned why his debt was being reported twice — as both a tradeline with the originalcreditor and as a tradeline with a third-party collection agency.

July 22, 2021), the Eastern District of Michigan granted summary judgment in favor of a debt collector, holding that it did not violate the Fair Debt Collections Practices Act (FDCPA) by failing to report that the plaintiff disputed the debt at issue. In Burns v. Keybridge Med. Revenue Care , No. 2:20-cv-12732 (E.D.

Here’s some bedrock—debt collectors can call numbers supplied by the consumer to an originalcreditor as part of a credit transaction. Things can get dicey where the consumer switches number or the collector doesn’t have access to the original data supplied to the creditor, so watch out if that’s the case.

The Act amends provisions of New York’s Civil Practice Law and Rules, commonly referred to as the CPLR, and the Judiciary Law to require originalcreditors and third-party debt collectors to include certain information and documents when filing and prosecuting debt collection actions.

July 22, 2021), the Eastern District of Michigan granted summary judgment in favor of a debt collector, holding that it did not violate the Fair Debt Collections Practices Act (FDCPA) by failing to report that the plaintiff disputed the debt at issue. Source: site. In Burns v. Keybridge Med. Revenue Care , No. 2:20-cv-12732 (E.D.

Write a letter to the originalcreditor or collection agency and ask them to remove the negative entry from your credit history as an act of goodwill. You will basically explain your situation to the creditor or collection agency. For this to work, be prepared to negotiate with the creditor or collection agency over the phone.

A recent federal district court opinion highlights the potential pitfalls associated with renewals of unsatisfied default judgments. serves as a reminder that judgmentcreditors must still tread carefully when seeking to collect on, or revive, judgments from yesteryear. The case, Sarah Pitera v. 2:22-cv-00255-TL (W.D.

Each state has a law referred to as a statute of limitations that spells out the time period during which a creditor or collector may sue borrowers to collect debts. But they also know that most borrowers who are sued for old debts won’t show up in court, and the judge will issue a default judgment. The creditor closes your account.

According to §809, “ If the consumer notifies the debt collector in writing within the thirty-day period described in subsection (a) that the debt, or any portion thereof, is disputed, or that the consumer requests the name and address of the originalcreditor, the debt collector shall cease collection of the debt, or any disputed portion thereof, (..)

If you notify this office in writing within THIRTY (30) days of receiving this notice that this debt, or any portion thereof, is disputed, this office will obtain verification of the debt, or a copy of a judgment against you, and mail you a copy of such verification or judgment. This timely appeal followed. Equifax A.R.S. ,

Because the sale of the car did not cover the full balance on the auto loan, Adams filed a lawsuit against Cheatham in state court to obtain a deficiency judgment on behalf of her client. The case began when Cheatham defaulted on a car loan and surrendered the vehicle, which was sold at auction. Cheatham was also awarded attorney’s fees.

The conduct provisions in the Stipulated Final Judgment and Order look substantially similar to those in the Hanna and Pressler cases previously entered into by the CFPB. Under the settlement agreement, the law firm agreed to obtain proper supporting documents before filing collection lawsuits and also to pay a $100,000 civil penalty.

A charge-off is when the creditor officially writes your debt off its books as a loss. Keep in mind that a creditor writing off your unpaid debt as a loss doesn’t mean you don’t owe the debt. Your creditor may sell your charged-off debt to a collection agency for pennies on the dollar.

In other words, when the originalcreditor has been unsuccessful in collecting on a debt, it will write off the debt as a loss. There’s a chance some details about your account got lost in the transfer from the originalcreditor. How Portfolio Recovery Associates Works. This is called a charge-off.

The letter must detail the specific information you require, such as proof of agreement with the originalcreditor, a final account statement issued by the creditor, and a breakdown of the debt (due dates, interest rate, and principal amount). There are many ways to request debt verification, such as writing a request letter.

The full name of the creditor. A statement that if the consumer notifies the debt collector in writing within the 30-day period that the debt, or a portion of the debt, is disputed, the debt collector will obtain proof of the debt of a copy of the judgment against the consumer.

(The court did not address whether or not the problematic envelope being inside another envelope has any impact on its decision, but that’s likely because they were reviewing a decision on a motion to dismiss rather than a motion for summary judgment.). Creditor ID Claims—A Mixed Bag. A judgment is a judgment.

Section 1788.206 provides that, in an action initiated by a private education lender or private education loan collector, no default or other judgment may be entered against a defendant unless documents are submitted by the plaintiff to the court to establish the facts required to be alleged. There are additional rules for class actions.

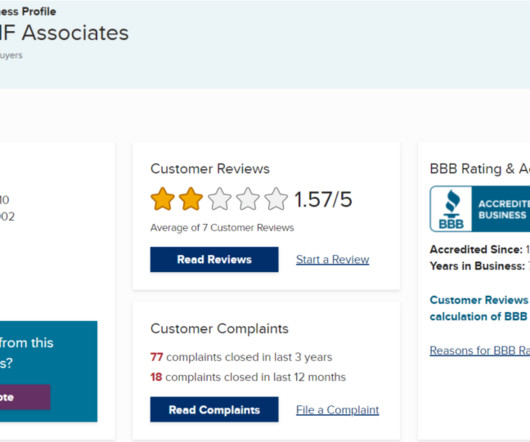

They can request a default judgment from the court if they contact you and you fail to respond within 20 days. A default judgment enables DNF Associates, LLC to seize your bank account, garnish your wages, and take other damaging legal actions against you. DNF Associates initiates legal proceedings against numerous individuals.

Capital Management Services, the collection agency sent a single letter which identified the original and current creditor, the account number as “5702” and the amount of the debt as $565.91. In Powers v.

The trial court granted summary judgment to the defendant on all claims finding that because the defendant was not a consumer lender it was not required to obtain the license at issue. Additionally, the appellate division found that the plaintiff had not suffered an ascertainable loss.

Section 1692g of the FDCPA says collectors must provide notice to consumers within five days of the initial communication regarding the debt, stating the amount of the debt, the name of the current creditor, and explaining the consumer’s right to dispute the debt and to obtain verification. See 15 U.S.C. 1692g(a)(1), (2). 1692g(a)(4).

For debt collectors choosing to use the last statement date, the Comments clarify that it is the date of the last statement provided by the creditor and may include those provided by a third party acting on the creditor’s behalf, such as a servicer. Section 1006.34(b) Section 1006.34(c) Section 1006.34(c)

A commercial debt collector works exclusively with B2B creditors that need to collect past due payments from other businesses. Negotiate payoff balances: In some cases, B2B creditors might authorize commercial debt collectors to make payment arrangements with their clients. What Do Commercial Debt Collection Agencies Do?

Make sure to follow through, because credit agencies can turn a simple collection into a judgment, legally garnishing wages or your bank account, you will be required to pay the full debt as well as legal fees. If you can, try to settle with the originalcreditor. The credit bureaus have 30 days to investigate the dispute.

If you notify this office in writing within 30 days of receiving this notice, this office will obtain verification of the debt or a copy of a judgment and mail a copy of it to you. IS THE CREDITOR'S ATTORNEY AND IS ATTEMPTING TO COLLECT A DEBT ON ITS BEHALF. Thank you for your attention to this matter. FABRIZIO & BROOK, P.C.

Because of their involvement in collecting money you owe a creditor, you may be contacted via a phone call or a letter from a debt collection attorney. It’s important to remember that the unpaid debt has passed through the originalcreditor to a debt collection attorney.

Even originalcreditors, who are not subject to the FDCPA, are being drawn into FDCPA litigation under various theories of recovery. For this reason, originalcreditors are not subject to the FDCPA (except in very limited circumstances). Retrieval Masters Creditor Bureau, Inc. , See, e.g., Perry v. Goodman , 200 F.3d

The debt collector may select one of five reference dates as the itemization date: 1) the last statement date; 2) the charge-off date; 3) the last payment date; 4) the transaction date; or 5) the judgment date; and. Importantly, the final rule revises the definition of “consumer” to include both living and deceased consumers.

As a debtor, you have the following rights: Right to Privacy: Debt collectors are not allowed to share information about your debts with anyone else except your attorney or the originalcreditor. The FOS can independently review your complaint and provide a judgment.

Creditors usually send several notices prior to filing a complaint with the court. In fact, the creditor will need to show the court its attempts at collecting the debt and its notice of intent to sue in order to prove its case. There are two other conditions that must be met for a creditor to serve papers on a debtor.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content