This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When filing for bankruptcy, you can discharge certain types of personalloans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personalloans you can discharge and which filing method best suits your financial situation.

Borrowing money costs more when you have bad credit — and your choices for a loan will be limited — which is why we have helped you narrow down your list by finding the top 6 best personalloans for bad credit. Use this time to fix your credit before applying for loans. 6 Best PersonalLoans for Bad Credit.

When filing for bankruptcy, you can discharge certain types of personalloans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personalloans you can discharge and which filing method suits your financial situation.

A personalloan enables you to borrow a lump sum of money and repay it in fixed installments. While personalloans can be a useful tool, there are important factors to consider before taking one out. According to recent statistics , millions of Americans have personalloan debt, with the average loan amount being $16,931.

Know How to Stop Creditor Harassment & Wage Garnishment Debt can be a heavy burden. Creditor harassment is any aggressive or threatening communication from a debt collector. Wage garnishment is a legal procedure where a creditor obtains a court order to withhold part of your earnings from your paycheck to repay a debt.

Your Chapter 13 bankruptcy plan creates an affordable route to satisfying your creditors and starting to rebuild your financial stability. The kinds of debt that can typically be eliminated are credit card debt, medical bills, utility bills, evictions, repossessions, and personalloans. It comes with some huge benefits.

For example, if you borrowed $12,000 for a personalloan and only paid back $6,000, you still received the original $12,000. Not paying back the other half of the loan means you got the benefit of that money without paying for it. The creditor that sent you the 1099-C also sent a copy to the IRS.

Pros: Because you are no longer overwhelmed with creditors and debts, you may be able to save money for secured loans or secured credit cards. How to obtain a personalloan: Get a copy of your credit reports (Equifax, Experian, and TransUnion). Apply for a Home Equity Loan or a Home Equity Line of Credit (HELOC).

It’s a common scenario: You apply for a personalloan or credit card and get denied. The reason seems shrouded in mystery, and you receive a letter with language such as “lack of recent installment loan information” or “proportion of balances to credit limits.”

You’ll also need to supply the bankruptcy court with a list of creditors, an income statement, and copies of your tax records. Filing Chapter 7 bankruptcy provides you with an automatic stay that prohibits creditors from being able to take any action to collect a debt against you, such as repossessions, wage garnishment, and legal action.

It works by getting one new loan and using that to pay off multiple existing creditors. You pay off multiple types of loans and credit card balances with your new consolidation loan, and you’re left with a single monthly payment to the new lender. It’s best to use home equity for consolidation as a last resort.

Most creditors still report to old scoring models, so it’s unlikely paying off the debt will improve your credit score. If you’ve gotten behind on payments to a creditor or lender, your debt could be sent to collections after around 120 days of missed payments. ® or VantageScore 4.0®. How Does Collections Debt Affect Your Credit Score?

Consider your income, assets, creditors, expenditures, and your ability to pass the means test while selecting between Chapter 13 and Chapter 7. Creditors are prohibited from contacting you after your petition is filed. Complete protection from creditors – This includes wage garnishment and debt collection.

If you file for Chapter 13 Bankruptcy in Indiana, you will still be obliged to pay something toward your debts; it’s just that you will be given a payment plan that reduces your unsecured debts based upon your ability to pay, that puts you on a manageable schedule, and that holds your creditors at bay while you work on making achievable payments.

When you miss too many payments, your creditor may charge off the debt. A charge-off occurs when you don’t pay the full minimum payment on a debt for several months and your creditor writes it off as a bad debt. When you start missing payments, creditors will first send letters reminding you of your past-due bill.

Here are 3 proven methods to remove a charge-off from your credit report: Negotiate A “Pay for Delete” & Pay The Creditor To Delete The Charge-Off. Offer To Pay The Creditor To Delete The Charge-Off. Some creditors will claim they can’t legally remove the charge-off. Creditor Name. This isn’t true.

That line of credit will then be reported to the credit reporting bureaus as a collection account—a collections account for a credit card, personalloan, etc.—and Therefore, this may earn you a bit of goodwill with future creditors. This is an escalation that means the creditor may take further action to collect the debt.

The Prime Rate Good Mortgage Interest Rates Good Car Loan Interest Rates Good Credit Card Interest Rates Good PersonalLoan Interest Rates Good Student Loan Interest Rates. What’s a Good Interest Rate on PersonalLoans? Personalloans are typically unsecured. In This Piece.

Bankruptcy can wipe out unsecured bills, leaving creditors with no way to recover the debt. Therefore, creditors of unsecured debt are often willing to accept less than the full balance owed if you are unable to pay off the balance in full. A growing stack of bills collects and grows bigger each week.

Tax Liens and Your Credit In many cases, if you fail to pay your bills or debts, creditors report that information to the credit bureaus. If You Pay Your Taxes with a PersonalLoan Some people take out a personalloan to pay off taxes. This method can impact your credit in a couple of ways: Hard inquiry.

These include transferring all your debt onto just one credit card as well as taking out a secured or unsecured personalloan—perhaps with the help of a professional debt consolidation company. Owing money to several creditors and remembering when the monthly payments are due for all of them can be overwhelming. Credit card 3.

Plaintiff obtained a personalloan that included an Arbitration Provision. Oliphant to whom Plaintiff’s loan had been transferred filed a collection action when Plaintiff defaulted. Defendant filed a Motion to Compel Arbitration and Plaintiff opposed. Defendant filed a motion to compel arbitration.

Bankruptcy will wipe out credit card debt, medical bills, and personalloans, but will not eliminate primary obligation debt; things like student loans, child and spousal support, and newer tax debt. In exchange of this discharge non-exempt assets are liquidated by a Chapter 7 trustee in order to pay creditors back something.

They then exercise control over the merchandise sold to satisfy creditors. They will sell them and use the revenues to pay for the bankruptcy’s fees , charges, and expenditures before paying creditors. ” The Trustee has the authority to seize and liquidate non-exempt property to benefit creditors.

In this plan, credit counseling agencies negotiate with your creditors for arranging a customized and budget-friendly repayment plan for you. The debt settlement companies negotiate with your creditors for a lower payoff amount in exchange for a lump sum payment. Based on your quote, they’ll negotiate with your creditors.

If you fail to pay, creditors cannot take your belongings. Credit cards, medical bills, and personalloans make up most unsecured debt that bankruptcy can eliminate. These debts have no collateral, so creditors cannot take your property without going to court first. This means there is no property tied to it.

Negotiating with creditors to lower your interest rates and waive fees. Under a DMP, a nonprofit credit counselor will work with your creditors on your behalf to consolidate your debts into a single monthly payment. Debt consolidation loans are another popular way to pay off credit card balances.

Your Creditor Could Sue You for Non-Payment of Dues. Your Creditor Could Take Possession of Your Assets at Your Home Country. If you have opted for a secured loan like a mortgage or a car loan, then make sure you pay your dues on time. You can look for lenders that provide credit building loans.

Debt consolidation might include a debt management repayment plan, credit card balance transfer, personalloan, or equity line of credit. You make one monthly payment to the program, and the agency pays your creditors based on an approved schedule. In many cases, the approved loan will come with a high rate of interest.

Economic stressors persist and are likely contributing to many consumers relying on credit to cover expenses, while the resumption of student loan payments adds another financial obligation to the mix. For consumers, the conundrum of balancing finances continues as the holiday spending season sneaks up.

Debt is the amount of money you owe to a lender or creditor. Some examples of debt are mortgages, credit card dues, and personalloans. Although accruing lots of debt isn’t ideal, it may sometimes be unavoidable, such as mortgage payments or student loans. They may still be responsible for paying a portion of the loan.

Obtaining PersonalLoans with a Cosigner Having a co-signer on a personalloan or credit card means that you associate another individual with your debt. Creditors can pursue reimbursement from the co-signer via repossessions, foreclosures, wage garnishment , and other aggressive actions.

There are many different types of installment loans that are reported on credit reports. These include auto loans, mortgage loans, student loans, credit builder loans, and personalloans. Creditors want to see whether you can handle different types of financing.

When a lender doesn’t receive payments for a line of credit, like a credit card or personalloan, they may choose to eventually sell that credit to a debt collection agency to get some of their money back. You can also contact the original creditor to get this information. How Does Debt End Up in Collections?

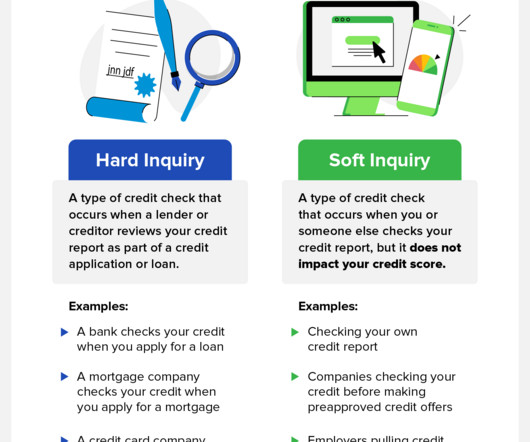

These are typically run by creditors who want to see if they can offer you potential products. For example, if you receive a mailing from a personalloan or credit card company stating you have been prequalified for potential credit, that company has probably run a soft check. Promotional soft credit checks.

However, if a lender or creditor checks your credit score as part of a credit application or loan, it is considered a “hard inquiry,” which can potentially lower your score by a few points. A hard inquiry is a credit check that occurs when a lender or creditor reviews your credit report as part of a credit application or loan.

With a deep commitment to personalized service, we take the time to understand your unique circumstances and tailor our approach to your specific needs. This powerful solution can immediately halt creditor harassment, wage garnishments, and lawsuits, allowing you to breathe a sigh of relief and regain control of your financial life.

As part of the deal, they must mediate with the creditors to get their payments back on track. Personalloans. Pay day loans. The break from payments can be cancelled if payments are made where possible and agreed, during the breathing space. Who is eligible? Store cards. Overdrafts.

With uncertainties about how the end of various pandemic-era benefits will impact consumers, it’s more important than ever for creditors and collectors to implement strategies that consider consumer situations and preferences when attempting to collect. Revolving credit utilization continues to slowly increase, as well.

typical Business borrowing, e.g. overdraft, bank loans, vehicle finance etc. Money invested in the business by directors or others, usually in the form of cash, personalloans, or personal guarantees. Informal Negotiation with creditors. The Small Business simply stops trading and informs creditors.

When you file for Chapter 7 bankruptcy, the Court will place an automatic stay upon filing, which stops creditors from collecting payments, garnishing wages, or repossessing property. They will then determine what, if any, non-exempt property they can seize and will use the proceeds from that property to repay a percentage to your creditors.

Through the bankruptcy, the debtor restructures and then creates and implements a plan to pay back creditors. In reality, they can take years and involve numerous legal proceedings on behalf of the person or business filing as well as the Trustee and creditors. The Trustee’s office then pays various creditors.

A debt management plan (DMP) is an agreement between a debtor (that’s you, the person in debt) and a creditor (think: your bank or your credit card company) that tackles your outstanding debt. Unsecured debts, such as credit cards, store cards and personalloans, can be part of your DMP. Will creditors still contact me?

They indicate serious delinquencies and tell creditors that you might be a risky bet. You Paid Off Debt If you recently paid off an installment loan—such as an auto loan, mortgage, personalloan, etc.—your Having a collection account appear on your credit reports will damage your scores. your score may drop a bit.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content