This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Sometimes it’s a foreclosure, increasingly often it’s due to large medical bills,” Pinsky notes. And unlike traditional loans, consumers with poor or slim credit histories may find that their creditworthiness gets judged in part by how they have handled utility bills or rent – transactions that usually don’t appear on credit reports.

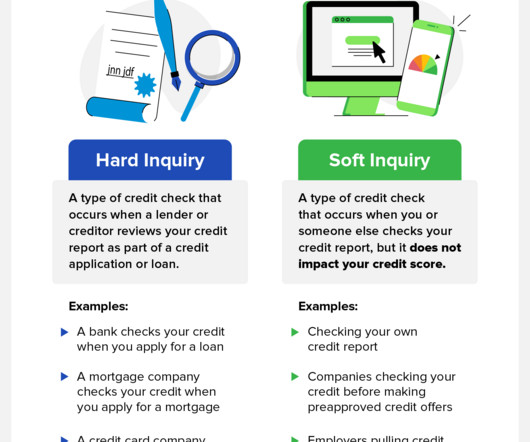

Your credit score is an important aspect of your financial health and is oftentimes used by lenders, landlords, and even employers to determine your creditworthiness. Hard inquiries , also known as hard pulls, are typically made by lenders and other financial institutions and can harm your credit score. What’s a Hard Inquiry?

While consumer groups praised the bill for its recourse for consumers harassed by debt collectors, CUNA and NAFCU saw the bill as complicating the legal relationship between consumers, members and lenders. In the letter, Nussle stated, “Lenders rely on complete and accurate credit reports when underwriting loans.

When a borrower applies for a loan or credit card, the lender will assess their creditworthiness by looking at their income, credit score, and debt-to-income ratio. If the lender is concerned about the borrower’s ability to repay the debt, they may require a co-signer. Considering Filing for Bankruptcy?

They let lenders access your complete credit report, which they use to assess your creditworthiness. While some lenders only look at one report, others may access all of them to get a clearer picture of your credit history. Foreclosure. Whether your credit issues are simple or more challenging, they can handle them.

Since payment history is the most important factor that influences your creditworthiness, not making payments on time can damage your credit score. Keep in mind that some lenders charge an up-front, one-time origination fee ranging from 1% to 10% of the total loan amount. Step 2: Get prequalified with a couple of lenders.

The consumer system is set up so that most purchases depend on applicant creditworthiness and a focus on being in debt responsibly. Although mortgage lenders offer mortgages ranging from 15 to 30 years, you are better off taking out a shorter mortgage and paying it off as fast as you can. Pay Off Your Mortgage Early.

The proposed rule would require lenders to assess a borrower’s ability to repay a PACE loan and would provide a framework for how these loans will be treated under the Truth in Lending Act. PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels.

The extensive network of loan-broker channels and increased involvement of nonbank lenders have resulted in growth in the availability of loans for purchase. On July 27, B25-0363, the Foreclosure Moratorium and Homeowner Assistance Fund Coordination Emergency Amendment Act of 2023, was signed by Mayor Muriel Bowser (D).

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. While the CFPB’s analysis is preliminary, the report shows some differences in lending patterns for lenders above and below the threshold.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content