This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Everything is online these days—including personalloans. Online lenders make it easy to compare rates and terms and find the right online personalloan for your situation. Personalloans were the fastest-growing category of consumer debt in 2019 , according to a survey from J.D.

A personalloan is money borrowed from a lender that can be used for almost any purpose, from debt consolidation to home improvement projects. Most people don’t have $5,000+ sitting in their bank accounts—that’s where personalloans come in. What Is a PersonalLoan? Why Would I Need a PersonalLoan?

Each year, tens of millions of Americans facing similar situations turn to personalloans to help ease the financial burden. With low interest for borrowers with strong credit scores, fixed rates, and a variety of lending sources to choose from, it’s easy to see why personalloans are so enticing. How PersonalLoans Work.

Borrowing money costs more when you have bad credit — and your choices for a loan will be limited — which is why we have helped you narrow down your list by finding the top 6 best personalloans for bad credit. Use this time to fix your credit before applying for loans. 6 Best PersonalLoans for Bad Credit.

The best personalloans charge low fees and low fixed interest rates, have flexible loan amounts and terms, and have no prepayment penalties. A personalloan could let you access cash for any purpose. Since personalloans are unsecured, you’ll need an excellent credit score to get the best deal.

And her bank wouldn’t give her and her husband Larry a loan to buy a replacement home. Brenda’s still tending her garden, though, thanks to a second-chance loan from the New Hampshire Community Loan Fund-a Community Development Financial Institution (CDFI). Flexible loan amounts. Support beyond the loan.

A signature loan is a fixed-rate, unsecured personalloan offered by an online lender, bank or credit union. It’s called a signature loan because it’s secured by your signature instead of collateral, like a car or an investment account. Getting approved for a signature loan will likely depend on your creditworthiness.

Vacation loans can help you cover all expenses, from transportation costs to accommodations and food. But these loans aren’t as perfect as they seem. These kinds of loans come with potentially high interest rates and fees. What Is a Vacation Loan? How Much Could the Vacation Loan Cost?

You might take out a small personalloan to cover new band equipment, for example, or use a credit card to buy school supplies. Research student loan options. It’s likely that you or your child will need to take out student loans to pay for their education. Funding a College Education. Talk to the financial aid office.

Use the same formula that lenders rely on when evaluating a loan application. The result is a percentage that determines your creditworthiness – in short, if lenders believe you’ll be able to repay the loan. Keep in mind that your ratio typically excludes mortgage and student loans.

Your credit score is an important aspect of your financial health and is oftentimes used by lenders, landlords, and even employers to determine your creditworthiness. Whether you’re applying for a loan or simply want to stay on top of your credit score, these tips will help you access your credit information without causing any harm.

Identity thieves are almost always opportunistic—but the crimes they commit feel very personal. Unauthorized credit card charges, bogus loan applications, missing money, and other financial violations make fraud a major nightmare. Negative public records can substantially impact your creditworthiness.

According to the Federal Reserve, consumer loans had a charge-off rate of around 2.3% The creditor closes your account, which could be a personalloan, credit card, revolving charge account or another debt you’ve failed to pay as promised, and it’s charged off as a bad debt. in the final quarter of 2019.

Alternative credit sources that do not report to the credit bureaus can include payments for rent, utilities, service accounts, and personalloans. We work with consumers seeking debt consolidation loans, or who may be considering options like debt negotiation or bankruptcy.

If you’re ready to open a new type of account to increase your account mix, consider a small personalloan. Ongoing Apr: 12.99%, 17.99% or 22.99%, based on your creditworthiness. Instead of getting a second card, focus on using your current cards more effectively. Already Have Multiple Cards? Review Your Payments. Card Details.

These include transferring all your debt onto just one credit card as well as taking out a secured or unsecured personalloan—perhaps with the help of a professional debt consolidation company. You can combine credit card debt, car finance, personalloans, student loans, medical bills, payday loans, and other types of unsecured debt.

Credit cards can take several days, loans can range from days to weeks, and mortgages can take weeks to a month. Lenders consider multiple factors when you apply for loans and credit cards , including your credit score and current finances. How Do I Apply for a Loan? How Do I Apply for a Loan?

Co-signers are beneficial for those seeking to obtain loans and credit cards. Obtaining PersonalLoans with a Cosigner Having a co-signer on a personalloan or credit card means that you associate another individual with your debt. Plus, being a co-signer can help a debtor build credit. What’s a Guarantor?

If you’re having trouble getting a car loan, using a cosigner could help. Before you take this step, it’s important to understand what a cosigner is and how having one on your car loan works. A cosigner is a person, usually a close friend or family member, who agrees to be responsible for repaying your car loan if you fail to do so.

I couldn’t get a credit card, let alone a mortgage loan. Good Credit (680 – 719): This is a good credit range to be in, but you won’t get the very best rates on loans or credit cards. You can still qualify for most FHA mortgage loans, for example. You Need a Mortgage Loan. Pay Down All Installment Loans.

Consider Taking Out a PersonalLoan to Consolidate Debt. If you’re dealing with high-interest debt or payments that simply add up to more than you can handle every month, you might consider a personalloan to consolidate debt. A debt consolidation loan doesn’t get rid of your debt, but it might make it more manageable.

This includes credit card balances, student loans, medical bills, and other outstanding obligations. Avoid the temptation to rely on credit cards or take out additional loans. Building an emergency fund: This is a crucial step to prevent relying on credit or loans during unexpected expenses or financial setbacks.

It shows lenders that you have a history of responsibly managing credit and can qualify you for better loan terms and lower interest rates. Lenders use them to determine if you qualify for auto loans, home loans, credit cards and other products. Few numbers are as important as your credit scores.

First, it can mean the credit extended to a business as opposed to a person. Second, business credit can refer to the creditworthiness of the business as an organization. They’re certainly less likely to loan your business money. Why can’t you just use your personal credit? That’s right.

Prosper also proactively mitigates credit risk and meets the increasing credit demand for creditworthy customers based on their monthly updated FICO® Scores. Managing Lending Risk with FICO Scores Throughout the almost twenty-year history of the Prosper personalloan platform, anticipating macro-economic downturns is a core principle.

Since payment history is the most important factor that influences your creditworthiness, not making payments on time can damage your credit score. Generally speaking, you will take out a loan or credit card with a lower interest rate and pay off all current balances with money from the new account.

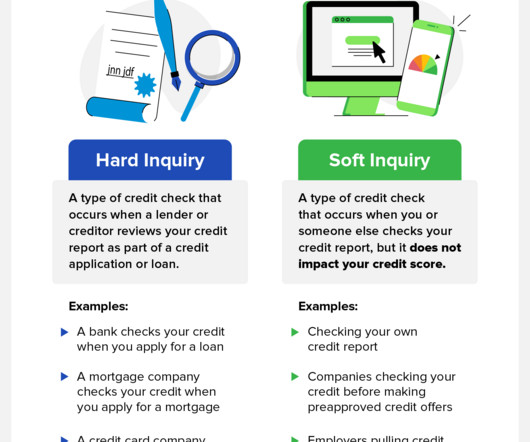

Only those that evaluate your financial creditworthiness do—these are hard credit checks. It’s important to remember that you will always authorize hard credit checks, so be mindful of how you space them out and what loans you need at what times. This is the number of recent hard inquiries on your report.

Making mistakes regarding how you use your credit cards can lower your score, raise your interest rates, and make it difficult to get a loan. Your credit score is an indicator of your creditworthiness and financial health. Debt Consolidation A debt consolidation loan is similar to a balance transfer card, but its a personalloan.

The growing complexity of financial products, such as credit cards, mortgages, and student loans, has led to a surge in outstanding debts. Analyzing vast amounts of data allows agencies to identify trends, assess debtor creditworthiness, and predict repayment probabilities.

Nearly all lenders conduct thorough credit checks prior to approving a loan. If you don’t have at least a good credit rating, you’re apt to have trouble securing a loan. Most lenders use either FICO scores or VantageScore scores when determining approval for a loan or credit card. FAQs What Is a Good Credit Score?

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content