This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this article we will answer the question: What can debtcollectors do to you? Does Colorado Law Protect Me From DebtCollectors? When collecting a debt from you, collection agencies must adhere to federal and state rules. Fortunately, the federal Fair Debt Collection Practices Act (FDCPA) protects all states.

Several collection agencies have been using electronic mediums like emails, social media platforms, and SMS to contact debtors. To a standard person, it may appear that contacting a debtor either way (traditional or electronic) is the same, a contact made is a contact made regardless of the medium. In fact, many prefer it that way.

The primary objective is to check if there was a violation of debt collection laws (FDCPA laws), and those recordings can be reviewed if there is a need. . Such complaints from debtors can get your client to worry about their reputation. This includes if the debtor was skip traced and how often you attempted to reach the debtor.

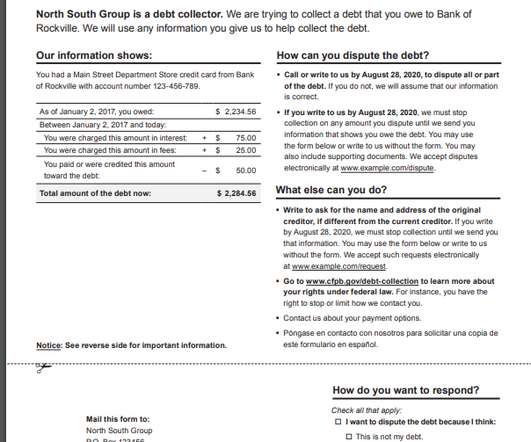

By law, all debtcollectors are required to provide at least 30 days to the debtor/consumer to dispute the debt, after the consumer receives (or is assumed to receive) the validation information. This format is located here: CFPB Debt Collection Validation Notice R19 ( as of Nov 2021). The amount is wrong.

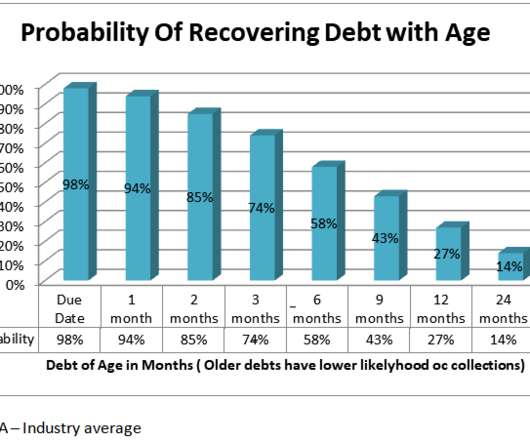

It falls to 74% collectible at three months, and by six months, only 58% of debts remain viable. At a year, there’s only a 27% chance of recovering the debt. These percentages assume skilled debtcollectors with modern collection tools at their disposal, like those found at agencies. Most creditors are unaware of these.

It falls to 74% collectible at three months, and by six months, only 58% of debts remain viable. At a year, there’s only a 27% chance of recovering the debt. These percentages assume skilled debtcollectors with modern collection tools at their disposal, like those found at agencies. Most creditors are unaware of these.

Getting calls from debtcollectors can be frustrating and even confusing. That’s even truer when someone is contacting you about an old debt you forgot about, thought was long resolved, or didn’t know about in the first place. Can a debtcollector collect after 10 years, for example? In This Piece.

Is there a law in NYC that protects consumers and debtors from debt collecting agencies, businesses, and their attorneys? Suppose you are under constant pressure from these agencies and their legal representatives to settle your debt. Consumers must be aware that the debt they are being collected for is valid.

Debtcollectors send debt validation letters show what debts you owe, the amount, and to whome you owe it to. While a debtcollector contacting you can be stressful, it’s important to pause and remember your rights as a debtor. Before paying the debtcollector, verify that the debt is actually yours.

District Court for the Southern District of California, granting summary judgment in favor of a debtcollector in a Fair Debt Collections Practices Act (FDCPA) case. In doing so, it held that a collection letter, which indicated that the debtor could only dispute the underlying debt in writing, violated the FDCPA.

The Fair Debt Collection Practices Act is a federal law that protects consumers against certain unfair collection practices. It applies to only external or third-party debtcollectors and only for personal debts. It does not come into play for creditors collecting their own debts. or after 9 p.m.

A debtcollector might sound like a character from a Charles Dickens novel, but if you’ve been contacted by one, you know they’re very much a reality of modern financial life. So, what exactly is a debtcollector? What Is a DebtCollector? Why Are They Contacting Me?

Experiencing a constant barrage of calls from debtcollectors can be overwhelming, to say the least. Many wonder, “How many times can a debtcollector call me in one day?” Harassment or Abuse: The FDCPA prohibits debtcollectors from using abusive, unfair, or deceptive practices. or after 9 p.m.,

Court of Appeals for the Third Circuit recently held that a debtcollector did not violate the federal Fair Debt Collection Practices Act (FDCPA) when it sent a consumer a collection letter inviting her to “eliminate further collection action” by calling the company, when in fact only written communication could legally stop collection activity.

Debt collection is a legitimate business that can involve challenging & confusing issues. Debtcollectors typically work with debt-collection agencies, though some may operate independently. Below mentioned are some of the typical debt collection queries that we aim to answer for you.

Courts apply the very pro-consumer “least sophisticated debtor” standard when evaluating a collector’s communications, and most violations of the Act are “strict liability” – meaning the debtor can win the case without proving the collector intended to violate the statute. Hollins Law Firm , _F.3d

It occurs when a collection agency or a company attempts to collect past-due debts from borrowers. Hiring debtcollectors are often a cost-effective alternative for businesses as it prevents you from investing your time and resources to manage your debts. How do debtcollectors work?

The debt collection process involves recovering debts from the borrower who has initially failed to repay or recover payments on accounts that are past their due date. most people tend to think of a debtcollector trying to contact debtors about some unresolved debts. The name of the originalcreditor.

If the debtcollector made an error: If you suspect the debt collection agency made a mistake, like if you see a debt you don’t recognize, you’ll need to confirm the debt belongs to you. Do so as soon as you can—within 30 days of a debtcollector’s first contact with you, if possible.

A statement that unless the consumer disputes the debt within 30 days of receipt it will be assumed to be valid by the debtcollector. A statement that the debtcollector will provide to the consumer, within 30 days, the name of the originalcreditor if different than the debtcollector.

Read on to discover all you need to know about debt collection agencies. Myths About Using a Collection Agency: Paying the OriginalCreditor to Bypass Agencies. Many people believe they can get around dealing with debt collection agencies by paying their originalcreditors directly.

Debt collection is a process that gives debtors certain rights that debt collection agencies must respect. While the debt shown in the collection can negatively impact your credit score, the severity of the impact reduces over time. What does it mean to have debt in collections? They will call at unofficial hours.

This is the federal law that protects consumers from being harassed by debtcollectors. As we’ve mentioned before, the law applies only to consumer debt, not businesses. The law also only applies to outside debtcollectors, not companies who are owed the money for product or services they provided.

Train your collectors to identify disputes early according to the guidelines your agency has in place. If you previously had consent (for example to the phone number that was provided to the originalcreditor), and that consent is withdrawn, it was likely done in an attempt to set up an action under the Telephone Consumer Protection Act.

It’s not uncommon for businesses to take on debt. Sometimes, that debt gets out of hand and businesses find themselves on the receiving end of calls from commercial debt collection agencies. Calls from a commercial debtcollector can create an enormous amount of stress for many business owners.

If you have ever had to deal with credit card debt, you know it can be stressful. Debtcollectors call at all hours of the day and pressure is put on borrowers to quickly make payments in full. The process begins when the debtor stops making payments on their credit card and goes into default.

If you’re a collection agency or creditor in New York, you need to be keeping an eye out for Senate Bill 3803. This bill was introduced to the state senate in February of this year, and the crux is that if approved, debtcollectors would be prohibited from using social media to contact debtors. Who Does This Affect?

Creditors give loans to millions of citizens, and thus credit companies are too busy to follow up on the debtors. For this reason, creditors are hiring debt collection agencies to collect debts that are 60 days past the agreed period. Debt collection agencies communicate to debtors via calls, letters, or emails.

Establishing Contact with the Debtor The first step in the debt collection process is establishing contact with the debtor. This often involves several key actions: Initial Communication: A business or a debt collection agency, like a debt collection agency in Derby, will send a letter of demand to the debtor.

The claim: It is illegal for collection agencies to buy debt and ‘come after you’ if you send a cease-and-desist letter A March 27 Facebook post (direct link, archive link) offers advice for consumers facing debt collection. “It The post also misrepresents the protections in place to prevent harassment by debtcollectors.

A debtcollector is free to collect during the thirty-day period as long as it does not overshadow or contradict the consumer’s thirty-day rights. But what if the debtcollector initiates a process that is not readily stopped if the consumer makes a timely request for validation? In Scott v. Trott Law, P.C. ,

Lawyers and agency owners are being sued based on the conduct of their clients and their collectors. Even originalcreditors, who are not subject to the FDCPA, are being drawn into FDCPA litigation under various theories of recovery. How can debtcollectors avoid liability for the conduct of others?

In 2009, the North Carolina legislature passed Senate Bill (SB) 974, which governed the requirements surrounding debt collection and asset buying in the state. For example, the following are still requirements to bring a lawsuit: The original account number, originalcreditor, the total amount claimed, an itemization of post charge?off

It is impossible to catalogue the manifold ways, some subtle and some not, in which a debtcollector may attempt to circumnavigate section 1692g.” 1989) (“The statute is not satisfied merely by inclusion of the required debt validation notice; the notice Congress required must be conveyed effectively to the debtor.

trillion worth of debt. When faced with mounting debt, it’s inevitable that someone will come to collect. Many people are facing a debtcollector threatening to serve papers. When courts get involved, debt collection gets serious. Of course, ignoring a process server doesn’t make the debt or lawsuit go away.

Furnishers are banks, debtcollectors, and others that report the information that shows up on your credit report. Re-aging can occur when a debt is sold to a third-party collector and the start date on the debt’s clock is muddied and appears to be a new debt. Furnisher errors.

One method for identifying areas of potential concern, however, is to analyze the recent enforcement actions by the CFPB and other regulators filed against debt buyers and originalcreditors. The most comprehensive enforcement action against a debt buyer in recent years was brought by the FTC, not the CFPB.

248, which limits a collection agency’s ability to collect on medical debt. The proposed amendments include changing the definition of medical debt, allowing medical debtors to initiate contact and make voluntary payments, and preventing certain written communications from being sent via certified mail.

THE Fair Debt Collection Practices Act (FDCPA) is a federal law that was enacted in 1978 by the United States Congress to protect consumers from abusive debtcollectors. Note, however, that the FDCPA applies only to third party collectors who collect debt for originalcreditors. Trump $45,000.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content