This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Is it possible for an individual to sue a debtcollector for violating the Fair Credit Reporting Act and Fair Debt Collection Practices Act for allegedly attempting to collect a debt that the individual believes he did not owe, when the individual took no action against the originalcreditor for placing the allegedly illegitimate debt … The post (..)

In this article we will answer the question: What can debtcollectors do to you? Does Colorado Law Protect Me From DebtCollectors? When collecting a debt from you, collection agencies must adhere to federal and state rules. Fortunately, the federal Fair Debt Collection Practices Act (FDCPA) protects all states.

2022): While convenience fees are not explicitly enumerated, Congress certainly did not want debtcollectors to skirt statutory prohibitions through linguistic sophistry. Translation: to CYA, you need better originalcreditor contracts.] Carrington Mortg. 4th 370 (4th Cir. See this vivid sinkhole video from July 2024.

Can debtcollectors take money from your bank account to offset debts you owe them? This is a very complicated aspect of financial law, and if you’re looking to legally find a way to make your accounts creditor-proof, it may be a good idea to talk to an attorney. Don’t Let Debts Get to the Garnishment Stage.

Dealing with credit card debt is challenging, let alone facing a debt lawsuit.If the creditor wins the lawsuit, you may face serious financial repercussions. If you find yourself being sued by a debtcollector, you may wonder how to get a credit card lawsuit dismissed. An estimated 2.5

District Court for the Southern District of California, granting summary judgment in favor of a debtcollector in a Fair Debt Collections Practices Act (FDCPA) case. In doing so, it held that a collection letter, which indicated that the debtor could only dispute the underlying debt in writing, violated the FDCPA.

Getting calls from debtcollectors can be frustrating and even confusing. That’s even truer when someone is contacting you about an old debt you forgot about, thought was long resolved, or didn’t know about in the first place. Can a debtcollector collect after 10 years, for example? In This Piece.

In Martinez, the court summarily dismissed the consumer’s claim alleging that the debtcollector violated 15 USC § 1692e (and specifically e(5) and e(10)) by sending a settlement letter on a time barred debt. The “merger principle merely extinguishes that specific claim that was adjudicated and replaces it with a final judgment.”

July 22, 2021), the Eastern District of Michigan granted summary judgment in favor of a debtcollector, holding that it did not violate the Fair Debt Collections Practices Act (FDCPA) by failing to report that the plaintiff disputed the debt at issue. In Burns v. Keybridge Med. Revenue Care , No.

The Fair Debt Collection Practices Act is a federal law that protects consumers against certain unfair collection practices. It applies to only external or third-party debtcollectors and only for personal debts. It does not come into play for creditors collecting their own debts. or after 9 p.m.

Legal Action : The creditor or collection agency may file a lawsuit against you to recover the debt. If you ignore this or fail to defend yourself in court, a default judgment may be issued against you. Possible Social Stigma : In some cases, debtcollectors may contact relatives or neighbors in an attempt to reach you.

July 22, 2021), the Eastern District of Michigan granted summary judgment in favor of a debtcollector, holding that it did not violate the Fair Debt Collections Practices Act (FDCPA) by failing to report that the plaintiff disputed the debt at issue. Source: site. In Burns v. Keybridge Med. Revenue Care , No.

Experiencing a constant barrage of calls from debtcollectors can be overwhelming, to say the least. Many wonder, “How many times can a debtcollector call me in one day?” Harassment or Abuse: The FDCPA prohibits debtcollectors from using abusive, unfair, or deceptive practices. or after 9 p.m.,

Court of Appeals for the Third Circuit recently held that a debtcollector did not violate the federal Fair Debt Collection Practices Act (FDCPA) when it sent a consumer a collection letter inviting her to “eliminate further collection action” by calling the company, when in fact only written communication could legally stop collection activity.

Here’s some bedrock—debtcollectors can call numbers supplied by the consumer to an originalcreditor as part of a credit transaction. Defendant moved for summary judgment and court granted. Either way, it never hurts to have a court decide that consent passed from a creditor to a debtcollector.

The Act amends provisions of New York’s Civil Practice Law and Rules, commonly referred to as the CPLR, and the Judiciary Law to require originalcreditors and third-party debtcollectors to include certain information and documents when filing and prosecuting debt collection actions.

Portfolio Recovery buys multiple accounts with old debt from companies that have given up and “charged off” the accounts. In other words, when the originalcreditor has been unsuccessful in collecting on a debt, it will write off the debt as a loss. Portfolio Recovery will buy old debt for pennies on the dollar.

Here is an overview of the NYC law on debt collection: The consumer or debtor can ask the debtcollector or attorney to verify the debt or show proof of verification upon collection. Consumers must be aware that the debt they are being collected for is valid. You must inform consumers about the debt specifics.

Because the sale of the car did not cover the full balance on the auto loan, Adams filed a lawsuit against Cheatham in state court to obtain a deficiency judgment on behalf of her client. Cheatham won the state court suit, and the debt was deemed to be unenforceable because notice was deficient under Arkansas law.

A statement that unless the consumer disputes the debt within 30 days of receipt it will be assumed to be valid by the debtcollector. A statement that the debtcollector will provide to the consumer, within 30 days, the name of the originalcreditor if different than the debtcollector.

Section 1692e prohibits false, deceptive or misleading representations in connection with the collection of a debt. Where interest is not accruing on a debt, the debtcollector does not need to state that no interest is accruing.

Write a letter to the originalcreditor or collection agency and ask them to remove the negative entry from your credit history as an act of goodwill. If disputing the negative entry doesn’t work because you couldn’t find errors, or because the credit bureaus fixed them, your next step should be asking for a goodwill adjustment.

The letter informed the consumer that she may dispute the debt or request verification, but did not specify that this must be done in writing. The panel found that the consumer lacked standing because she failed to allege that the debtcollector’s actions harmed her or posed any risk to her. Creditor ID Claims—A Mixed Bag.

Communications in Connection with Debt Collection) to allow debtcollectors to communicate with the deceased consumer’s spouse, parent (if the consumer is a minor), legal guardian, executor or administrator, and confirmed successor in interest (as defined Regulation X). Section 1006.2(c) This definition dovetails with 1006.6

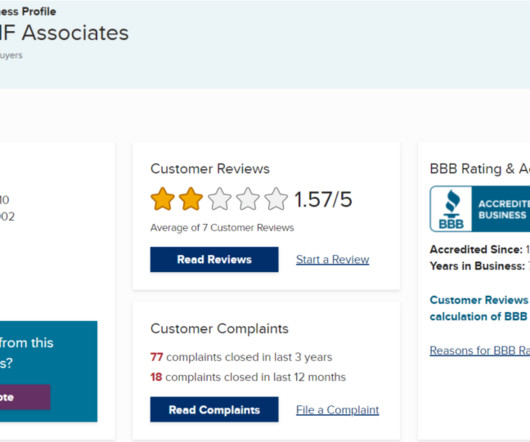

Like all other debtcollectors, DNF Associates, LLC depends on multiple sources of information to pursue debt collection. This involves gathering all relevant information and evidence regarding the purported debt. Typically, DNF Associates purchase these debts for as low as 10% of the original amount owed.

Under the final rule, debtcollectors must provide the consumer with certain information relating to the debt and the consumer’s rights (Validation Notice). consumer response information, such as prepared statements and prompts that the consumer may use to take certain actions, including disputing the debt.

Make sure to follow through, because credit agencies can turn a simple collection into a judgment, legally garnishing wages or your bank account, you will be required to pay the full debt as well as legal fees. Debt Validation. If you can, try to settle with the originalcreditor. Calling you before 8:00 A.M

It’s not uncommon for businesses to take on debt. Sometimes, that debt gets out of hand and businesses find themselves on the receiving end of calls from commercial debt collection agencies. Calls from a commercial debtcollector can create an enormous amount of stress for many business owners.

A debtcollector is free to collect during the thirty-day period as long as it does not overshadow or contradict the consumer’s thirty-day rights. But what if the debtcollector initiates a process that is not readily stopped if the consumer makes a timely request for validation? In Scott v. Trott Law, P.C. ,

Lawyers and agency owners are being sued based on the conduct of their clients and their collectors. Even originalcreditors, who are not subject to the FDCPA, are being drawn into FDCPA litigation under various theories of recovery. How can debtcollectors avoid liability for the conduct of others?

This article will examine the decision, its immediate impacts, and considerations for the industry as it moves toward implementation of the debt collection rule. A Quick Summary In Hunstein , the debtcollector engaged a third-party vendor to prepare and send its demand letter. LEXIS 11648 at *4.

It is impossible to catalogue the manifold ways, some subtle and some not, in which a debtcollector may attempt to circumnavigate section 1692g.” 1989) (“The statute is not satisfied merely by inclusion of the required debt validation notice; the notice Congress required must be conveyed effectively to the debtor. 1692g(a)(3).

There, the collection law firm defendant communicated with plaintiff on a number of occasions, and each time the firm identified itself as a “debtcollector,” as required by section 1692e(11) of the FDCPA. Thank You,” without specifically reciting he was a “debtcollector.” Hollins Law Firm , _F.3d iii] See Wahl , 556 F.3d

Your creditor may sell your charged-off debt to a collection agency for pennies on the dollar. The collection agency may then attempt to collect the debt anew. Pro tip: Even if a debt has been charged off, consider contacting the originalcreditor to negotiate a settlement.

trillion worth of debt. When faced with mounting debt, it’s inevitable that someone will come to collect. Many people are facing a debtcollector threatening to serve papers. When courts get involved, debt collection gets serious. Of course, ignoring a process server doesn’t make the debt or lawsuit go away.

One method for identifying areas of potential concern, however, is to analyze the recent enforcement actions by the CFPB and other regulators filed against debt buyers and originalcreditors. The most comprehensive enforcement action against a debt buyer in recent years was brought by the FTC, not the CFPB.

The knowing failure to communicate that a "disputed" debt is disputed is a violation of section 1692e(8). 1998) (section 1692e(8) "requires a debtcollector who knows or should know that a given debt is disputed to disclose its disputed status to persons inquiring about a consumer's credit history.") (emphasis added); Sunga v.

Zombie Debts and Judgments. If the originalcreditor went to court and obtained a judgment against you for a debt, the zombie debt cycle can be more complicated. First, judgments provide the creditor with the legal means to collect via actions such as wage garnishments or bank account liens.

The plaintiff incurred a debt to a medical provider who placed the debt with a debtcollector. The collection letter from the debtcollector included a request for repayment of principal and interest. The district court agreed and granted summary judgment to the defendant.

Dealing with zombie debt can be extremely complicated as debtcollectors may repeatedly contact you about an account that belonged to you years ago. Much like the characters in a post-apocalyptic story, it’s possible to overcome zombie debt with the right know-how. How Does Zombie Debt Work?

NYC Amends Collection Regulation to Clarify Debt Collection Definition Includes Creditors In a development first announced by ACA International, the New York City Department of Consumer and Worker Protection (DCWP) has proposed an amendment to its new debt collection regulation. More details here.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content