This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A District Court judge in Arizona has granted a defendant’s motion to dismiss a Fair Debt Collection Practices Act case, ruling that the plaintiff failed to sufficiently establish the defendant’s status as a “debtcollector” under the statute and did not plead adequate facts to support the alleged violations.

It should be noted lawsuits can be filed against consumers seeking to collect on debts for which the statute of limitations is expired — it is up to the consumer to assert that the statute of limitations has expired as an affirmative defense to have the collection suit dismissed. Cohen said in a statement.

These regulations could fundamentally alter how creditors and debtcollectors operate, potentially harming consumers while imposing onerous compliance burdens on financial institutions.

In a development first announced by ACA International, the New York City Department of Consumer and Worker Protection (DCWP) has proposed an amendment to its new debt collection regulation. This change directly impacts originalcreditors who previously may not have considered themselves subject to these regulations.

Debtcollectors are conduits — vessels trying to help originalcreditors recover unpaid debts. Oftentimes, the creditors will make requests or want certain offers included in letters sent to individuals.

Is it possible for an individual to sue a debtcollector for violating the Fair Credit Reporting Act and Fair Debt Collection Practices Act for allegedly attempting to collect a debt that the individual believes he did not owe, when the individual took no action against the originalcreditor for placing the allegedly illegitimate debt … The post (..)

The California state Senate yesterday passed SB 531, a bill that would require the originalcreditor or owner of a debt to notify a consumer within five days of the sale or assignment of the debt to someone else, while also giving consumers the right to request certain information about a debt from debtcollectors, … The post Calif.

Working with third-party debtcollectors can be confusing and scary. adults with debt in collections, knowing their legal rights is crucial. The Fair Debt Collection Practices Act covers third-party debtcollectors — those who buy a delinquent debt from an originalcreditor, like a credit card company.

In this article we will answer the question: What can debtcollectors do to you? Does Colorado Law Protect Me From DebtCollectors? When collecting a debt from you, collection agencies must adhere to federal and state rules. Fortunately, the federal Fair Debt Collection Practices Act (FDCPA) protects all states.

Whether you have missed a single payment somewhere along the line or are delinquent on several payments, the last thing you want is to be harassed by debtcollectors. The FDCPA applies only to debtcollectors (the third-party collection agencies), not to the original lender. Use abusive or obscene language.

Can debtcollectors take money from your bank account to offset debts you owe them? This is a very complicated aspect of financial law, and if you’re looking to legally find a way to make your accounts creditor-proof, it may be a good idea to talk to an attorney. Don’t Let Debts Get to the Garnishment Stage.

Any debtcollectors still charging convenience fees or other fees to consumers that are not covered in the contract between the consumer and the originalcreditor are breaking the law and may be subject to lawsuits from consumers and regulatory scrutiny from the Consumer Financial Protection Bureau, the agency announced yesterday by issuing an Advisory (..)

The National Consumer Law Center has submitted a petition to the Consumer Financial Protection Bureau requesting that originalcreditors be responsible for furnishing information related to debt collection activity undertaken by third-party debtcollectors or debt buyers, and that collectors should be required to review documents like the original (..)

The debt collection industry is constantly under the lens of government regulators, surrounded by strict collection laws and several attorneys who are always looking for an opportunity to sue collection agencies over the slightest fault. The FDCPA (federal debt collection laws) have not changed much for decades now.

2022): While convenience fees are not explicitly enumerated, Congress certainly did not want debtcollectors to skirt statutory prohibitions through linguistic sophistry. Translation: to CYA, you need better originalcreditor contracts.] Carrington Mortg. 4th 370 (4th Cir.

Getting calls from debtcollectors can be frustrating and even confusing. That’s even truer when someone is contacting you about an old debt you forgot about, thought was long resolved, or didn’t know about in the first place. Can a debtcollector collect after 10 years, for example? In This Piece.

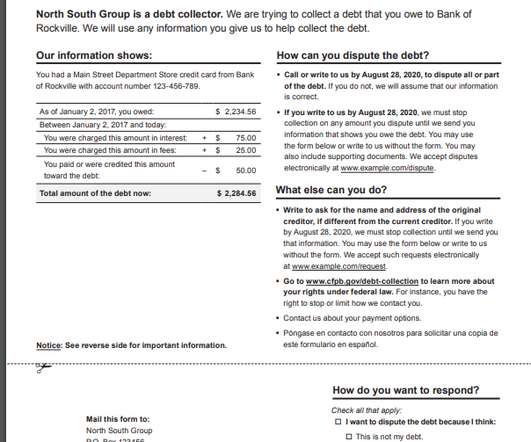

By law, all debtcollectors are required to provide at least 30 days to the debtor/consumer to dispute the debt, after the consumer receives (or is assumed to receive) the validation information. This format is located here: CFPB Debt Collection Validation Notice R19 ( as of Nov 2021). The amount is wrong.

Dealing with credit card debt is challenging, let alone facing a debt lawsuit.If the creditor wins the lawsuit, you may face serious financial repercussions. If you find yourself being sued by a debtcollector, you may wonder how to get a credit card lawsuit dismissed. An estimated 2.5

The primary objective is to check if there was a violation of debt collection laws (FDCPA laws), and those recordings can be reviewed if there is a need. . If your client insists that they want to see collector notes on the online portal to understand how much collection activity is going on each of their accounts, that is again tricky.

Debtcollectors send debt validation letters show what debts you owe, the amount, and to whome you owe it to. While a debtcollector contacting you can be stressful, it’s important to pause and remember your rights as a debtor. Before paying the debtcollector, verify that the debt is actually yours.

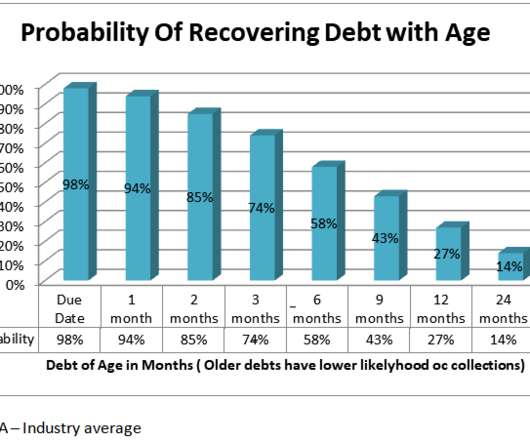

It falls to 74% collectible at three months, and by six months, only 58% of debts remain viable. At a year, there’s only a 27% chance of recovering the debt. These percentages assume skilled debtcollectors with modern collection tools at their disposal, like those found at agencies.

It falls to 74% collectible at three months, and by six months, only 58% of debts remain viable. At a year, there’s only a 27% chance of recovering the debt. These percentages assume skilled debtcollectors with modern collection tools at their disposal, like those found at agencies.

The Fair Debt Collection Practices Act is a federal law that protects consumers against certain unfair collection practices. It applies to only external or third-party debtcollectors and only for personal debts. It does not come into play for creditors collecting their own debts. Debt Collection Laws.

Understanding your rights as a consumer is crucial when dealing with debtcollectors. Unfortunately, many UK consumers are unaware of their legal protections and end up feeling intimidated or helpless when faced with aggressive debt collection tactics. Legitimate collectors should readily provide this information.

The Type of Creditor Still Matters. One change that isn’t included in the update is any type of protection from originalcreditors. Remember the Original FDCPA Rights. And anyone attempting to collect a debt is always going to be better served to treat the person they are attempting to contact with dignity and respect.

District Court for the Southern District of California, granting summary judgment in favor of a debtcollector in a Fair Debt Collections Practices Act (FDCPA) case. In doing so, it held that a collection letter, which indicated that the debtor could only dispute the underlying debt in writing, violated the FDCPA.

When this happens, it means your debt has gone to collections and debtcollectors from the collection agency will now try to contact you for payment. Here are some reasons to pay your collection debt: Dodge lawsuits: If you don’t pay off your collection debt, the debtcollectors may sue you.

Experiencing a constant barrage of calls from debtcollectors can be overwhelming, to say the least. Many wonder, “How many times can a debtcollector call me in one day?” Harassment or Abuse: The FDCPA prohibits debtcollectors from using abusive, unfair, or deceptive practices. or after 9 p.m.,

A debtcollector might sound like a character from a Charles Dickens novel, but if you’ve been contacted by one, you know they’re very much a reality of modern financial life. So, what exactly is a debtcollector? What Is a DebtCollector? Why Are They Contacting Me?

Nothing is quite as panic-inducing as receiving a call from a debtcollector. Not only are they notoriously rude, but having a debtcollector on your tail can mean that your credit score is about to take a dive. Unfortunately, they are a completely legitimate debtcollector but are also a terrible pain to deal with.

Whether you owe a debt or not, getting a phone call from a debtcollector is never a pleasant experience. The hiatus that some states and companies put on debt collection activities at the height of the pandemic has largely ended, and debtcollectors have resumed business as usual. Ask for Documentation.

Illegal activities included harassing phone calls, bogus threats of arrest or lawsuit, and violations of other provisions of the Fair Debt Collection Practices Act. In many cases, consumers didn’t even owe the debts. The collector’s refusal to provide the information is a red flag it’s a scam. Check with the originalcreditor.

One of the most effective ways to get negative items removed from your credit report is to pay the debt, in exchange for the creditor removing the charge-off from your credit report. With this method, you’d use your payment as leverage to convince the debtcollector to help restore your credit. Ads by Money.

While attempting to provide additional protections for consumers when debtcollectors reach out using digital channels, these NYDFS and NYC DCWP restrictions create unintended consequences that raise barriers for NY consumers to correspond with collection agencies in their channel of preference and hinder communication efforts.

If you have been contacted by Sunrise Credit Services, you are probably being pursued for an old debt. Sunrise Credit Services is a debtcollector that has been hired by your old creditor to collect payment on your debt. They may also have purchased the debt to profit off your payments. Validate the Debt.

Court of Appeals for the Third Circuit recently held that a debtcollector did not violate the federal Fair Debt Collection Practices Act (FDCPA) when it sent a consumer a collection letter inviting her to “eliminate further collection action” by calling the company, when in fact only written communication could legally stop collection activity.

That means a collector or agent can direct a customer to a payment portal and stay on the chat to verify the payment went through. Especially for third party debtcollectors, pivoting away from mail might require lots of internal work to make sure youre following digital compliance rules.

July 22, 2021), the Eastern District of Michigan granted summary judgment in favor of a debtcollector, holding that it did not violate the Fair Debt Collections Practices Act (FDCPA) by failing to report that the plaintiff disputed the debt at issue. In Burns v. Keybridge Med. Revenue Care , No. 2:20-cv-12732 (E.D.

You may start getting calls from a debtcollector. Failing to pay your bills will cause the debt to move to collections. This means that your originalcreditor has officially handed the account over to a collection agency that will hound you for payments. Have you missed a few payments on one or more of your bills?

Portfolio Recovery buys multiple accounts with old debt from companies that have given up and “charged off” the accounts. In other words, when the originalcreditor has been unsuccessful in collecting on a debt, it will write off the debt as a loss. Portfolio Recovery will buy old debt for pennies on the dollar.

Stress and Mental Health Issues : The constant worry and anxiety of knowing you have a debt in collections and the possible legal consequences can negatively impact your mental health. Possible Social Stigma : In some cases, debtcollectors may contact relatives or neighbors in an attempt to reach you.

Here’s some bedrock—debtcollectors can call numbers supplied by the consumer to an originalcreditor as part of a credit transaction. Either way, it never hurts to have a court decide that consent passed from a creditor to a debtcollector. Really quick one for you.

If the debtcollector made an error: If you suspect the debt collection agency made a mistake, like if you see a debt you don’t recognize, you’ll need to confirm the debt belongs to you. Do so as soon as you can—within 30 days of a debtcollector’s first contact with you, if possible.

In Martinez, the court summarily dismissed the consumer’s claim alleging that the debtcollector violated 15 USC § 1692e (and specifically e(5) and e(10)) by sending a settlement letter on a time barred debt. The Court pointed to the following language: “It also includes any disputes you have with our .

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content