This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Axiom Acquisition Ventures, LLC (“Axiom”) bought Robert Valenzuela’s consumer debt from a bank after he allegedly defaulted on his personalloan payments. The post District Court Holds Letter Notifying Debtor of Change in Debt Ownership Can Fall Under FDCPA appeared first on Collection Industry News.

Axiom Acquisition Ventures, LLC (“Axiom”) bought Robert Valenzuela’s consumer debt from a bank after he allegedly defaulted on his personalloan payments. Axiom sent Valenzuela a letter informing him that his debt had been reassigned and instructing him to remit future payments to Axiom.

If you have a co-signer associated with your debt or if you are a co-signer, you need to be aware of how financial liability works and what happens when the primary debtor declares bankruptcy. For example, a parent or another family member may become a co-signer for a low-credit borrower so that the primary debtor can obtain a desirable loan.

In Chapter 7 bankruptcy proceedings, the phrase “non-exempt property” refers to a debtor’s estate property that does not qualify for a statutory exemption. Additionally, creditors may take such property if a judgement against the debtor is entered. portion of the debtor’s home’s equity.

A CHANGING CREDIT LANDSCAPE Over the past five years, there has been a significant increase in the usage of unsecured credit products, such as personalloans and credit cards, particularly following COVID- 19 and the rising cost of living.

Bankruptcy will wipe out credit card debt, medical bills, and personalloans, but will not eliminate primary obligation debt; things like student loans, child and spousal support, and newer tax debt. Chapter 13 Bankruptcy: Chapter 13 bankruptcy is a reorganization of debts for debtors with regular income.

BEST CREDIT CARD CONSOLIDATION LOANS. While credit counseling may be the preferred option for debtors with fair or bad credit, consumers with good credit can consider alternative debt repayment methods like credit card balance transfers. Debt consolidation loans are another popular way to pay off credit card balances.

People who are in debt from credit cards, loans and other personal debt sources could be given ‘breathing space’ under new temporary measures the government has announced. During the current pandemic, debt charity Stepchange has warned of a impending “personal debt tsunami” of £6Bn. Personalloans.

Consumer Debt Collection Basics Consumer debt collection describes debts that are owed by individuals, which can include anything from credit card balances and old utility bills to personalloans, medical debt, and mortgages. Should things fail to work out from there, a court judgment is usually the next step.

Dealing with difficult debtors for debt collection can be challenging and burdensome. While it is reasonable for you to wait for your debtors to have enough funds to pay you, it gradually hampers your business’s growth and productivity in the long run. Most people think that all debt collectors are the same. Skip tracing system.

Certain debts—such as credit card debt, medical bills, and personalloans—can be discharged. Many personal assets may be exempt. This enables debtors to keep important items while addressing their debts. However, eligibility requires debtors to pass a means test. However, not all debts can be discharged.

In the case of a Chapter 7 bankruptcy , the court appoints a trustee who is in charge of selling off (liquidating) a debtor’s non-exempt assets. Laws called exemption statutes determine what a person or married couple can keep through the Chapter 7 process. If a debt is unsecured, no collateral is put up as a guarantee to pay.

Chapter 7 bankruptcy is appropriate for unsecured debtors. personalloans, personalloans, delinquent income tax obligations, . It’s a relatively straightforward technique to eliminate the majority of your debt. . Without having to repay it later, you may immediately begin rebuilding your credit. .

With Chapter 7 bankruptcy, you as the debtor can discharge most unsecured obligations after liquidating nonexempt assets. In this blog, we discuss what assets and property a debtor may lose in Chapter 7 bankruptcy. Bankruptcy Code requires debtors to complete credit counseling courses 180 days before filing.

Creditors give loans to millions of citizens, and thus credit companies are too busy to follow up on the debtors. Therefore, the agencies act as middlemen collecting any delinquent loans. Debt collection agencies communicate to debtors via calls, letters, or emails. government collection agency.

How Debt Consolidation Loans Work. A debt consolidation loan is a personalloan that can be used to pay off all of your debts, so instead of owing money to multiple sources, you will just have to pay back one lender with a monthly payment. That’s because you’ll be able to qualify with more providers at lower rates.”

Chapter 7 is also known as liquidation bankruptcy because in exchange for receiving a discharge of most kinds of debts, the debtor has to give up non-exempt assets. Debtors have rights and protections under these laws to prevent harassment, false representations, or unfair practices by debt collectors.

Most Debtors, however keep everything they have. With Chapter 7 bankruptcy, you’ll be able to eliminate most unsecured debts, which includes: Credit card debt Medical debt Personalloans Payday loans Utility bills It’s important to keep in mind, though, that Chapter 7 will not eliminate all kinds of debt.

However, many debtors have questions regarding how filing for bankruptcy impacts child support payments and debts. In this blog, we unpack what happens to child support income and obligations when a debtor files in Indiana. Can You File Bankruptcy on Child Support?

If you qualify for Chapter 7 bankruptcy, our attorneys can guide you through the process of eliminating unsecured debts, such as credit card balances, medical expenses, and personalloans, within a matter of months. Bankruptcy law was created to give debtors a true fresh start and pathway to rebuilding wealth.

Indiana allows debtors to exempt assets when filing for bankruptcy up to a certain monetary amount, and that amount recently increased. When filing, you are allowed to exempt a portion of your home’s equity, tangible personal property, and intangible personal property.

Credit cards, medical bills, and personalloans make up most unsecured debt that bankruptcy can eliminate. To qualify for Chapter 7 bankruptcy, debtors must pass a means test that compares their income to their state’s median income. PersonalLoansPersonalloans are borrowed money that you agree to pay back over time.

This includes debts such as credit card balances, medical bills, personalloans, utility bills, back rent, mortgages, and car payments. Also, if you have a debt that is a lien against collateral (a car loan, a mortgage loan), the creditor can force a return of that collateral to try and partially satisfy their debt.

A reaffirmation agreement is a document that re-obligates a debtor to repay a particular debt, such as a car loan, mortgage, or other loan type. It basically serves as a legally binding promise that the person filing for bankruptcy will resume making payments in full and on time to the creditor.

Debt elimination is typically one of the primary reasons a debtor will pursue bankruptcy. The more common types of debts that many debtors hold that cannot be eliminated include: Child Support and Alimony. Student loans can be particularly challenging. A total of 19 categories are listed by the U.S.

For debtors who want to pay their balances down, the best approach is to take matters into their own hands, said Matt Schulz, chief credit analyst at LendingTree. Or they may consider a personalloan to help consolidate their debts for a lower rate.

A debt management plan (DMP) is an agreement between a debtor (that’s you, the person in debt) and a creditor (think: your bank or your credit card company) that tackles your outstanding debt. Unsecured debts, such as credit cards, store cards and personalloans, can be part of your DMP.

These technologies enable debt collectors to automate repetitive tasks, streamline workflows, analyze data more effectively, and personalize communication with debtors. Analyzing vast amounts of data allows agencies to identify trends, assess debtor creditworthiness, and predict repayment probabilities.

Through the bankruptcy, the debtor restructures and then creates and implements a plan to pay back creditors. You typically can’t apply for most types of credit, including a mortgage, auto loan or significant personalloan, without getting the court’s approval if you’re in the middle of a Chapter 13 bankruptcy, for example.

The number of new loans originated has also fallen across a variety of debt types, with the most precipitous drop in bank card originations. The economic downturn has not yet translated into elevated delinquency rates for consumer loans.

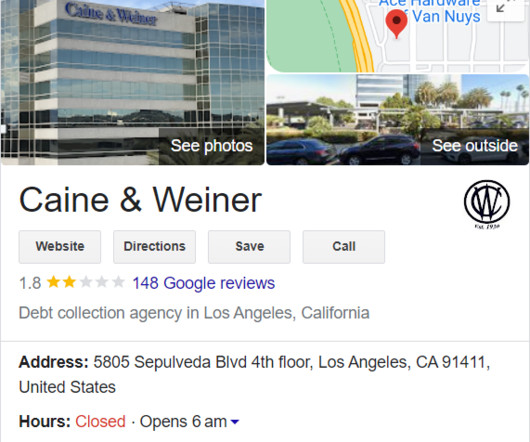

Caine and Weiner is a prominent debt collection firm that operates across various sectors, gathering debts from a range of industries, including: Personalloans Phone bills Student loans Credit cards To secure his debts, Caine and Weiner acquire them from the original creditors at a reduced price, then pursue the entire amount from the debtor.

Instead, when a debtor fails to pay, the lender must first file a lawsuit in order to collect what is owed. If an agreement cannot be reached between the debtor and the debt collector, the lender will likely file a lawsuit against you. With unsecured debt, there is no lien or security interest agreed upon. Examples of Unsecured Debts.

typical Business borrowing, e.g. overdraft, bank loans, vehicle finance etc. Money invested in the business by directors or others, usually in the form of cash, personalloans, or personal guarantees. For self employed and sole traders, there is no legal separation between personal and business debts.

Unsecured debt includes things like credit card debt, medical debt, and personalloans. The above descriptions provide a very broad overview of these two types of bankruptcy filings, but debtors should discuss these options at length with a lawyer who has experience in bankruptcy.) When Should I Contact an Attorney?

Common types of dischargeable debt include: Credit card debt Medical debt Judgements Utility bills Back rent Personalloans Repossession balances While Chapter 13 helps you repay certain debts and discharge remaining balances, not all forms of debt are dischargeable.

Unsecured debt includes things like credit card debt, medical debt, and personalloans. In most cases, Chapter 7 rules protect assets that are classified as exempt at the time you file versus unsecured debt which is not protected.

When a lender doesn’t receive payments for a line of credit, like a credit card or personalloan, they may choose to eventually sell that credit to a debt collection agency to get some of their money back. FAQ Still have questions about how to remove collections from credit reports? We’ve answered some frequently asked questions below.

One line of cases creates a duty to disclose to the debtor that the amount of the debt may be increasing due to accruing interest, fees or other charges. To avoid confusion to the debtor, the Avila Court held that use of the “safe harbor” language from the Miller case would be sufficient. Riexinger & Associates, LLC , 817 F.3d

1992) (emphasis added, citation and quotation marks omitted) (personalloan from friend used to start software business not a “debt” under the Act: “Neither the lender's motives nor the fashion in which the loan is memorialized are dispositive of this inquiry.”). 2012) (intent of debtor at time of purchase controls).

The debt came from high-interest personalloans, payday loans, credit cards, and other sources. In 2019, Attorney General James announced a $60 million judgment against debt collection kingpin, Douglas MacKinnon , who engaged debtors using similar deceptive and illegal tactics.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content