This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

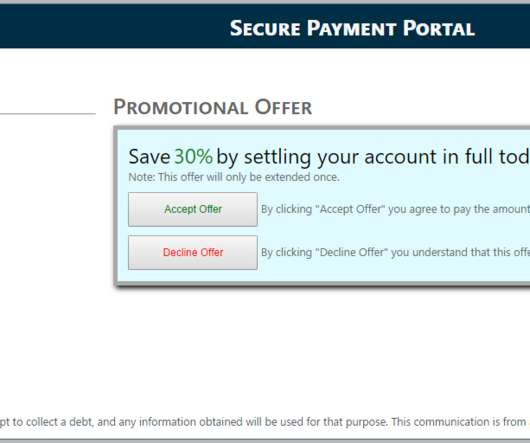

Simplicity Debt Collection Software is pleased to announce the roll out of its new Enterprise Debtor Payment Portal. This fully functional portal allows you to empower your debtors to make payments, settle accounts, set up payment plans, confirm their information and so much more. Use this application easily from your own website or direct them to our portal, either option is now available.

The CFPB continues to flex its muscle and expand its reach, this time punishing a prepaid card provider and its vendor for a conversion to a new system that did not go as planned. The consent order, which was entered into without any admission of liability, requires UniRush and its vendor/payment processor to pay an estimated $10 million in restitution to affected consumers and a civil monetary penalty of $3 million.

The CFPB has issued its monthly complaint report and is shining its spotlight on mortgage products. The Monthly Complaint Report provides a high level snap shot of trends in consumer complaints, using a three month rolling average of complaints. Each month, the report focuses on a category of consumer financial products. Here are the highlights of the most recent report: IN GENERAL · Student loans showed the greatest increase in complaints comparing October -December 2015 with October-December 2

The Ninth Circuit recently weighed in on the limitations of prior express consent and revocation under the Telephone Consumer Protection Act (the “TCPA”). In Van Patten v. Vertical Fitness Group, LLC, the consumer provided his cell number when meeting with a fitness gym about joining. Van Patten v. Vertical Fitness Group, LLC, 2017 U.S. App. LEXIS 1591 (9 th Cir.

AI is reshaping industries, yet finance remains one of the slowest adopters. Concerns over compliance, legacy systems, and data silos have made finance teams hesitant to embrace AI-driven transformation. But delaying adoption isn’t just about efficiency—it’s about staying competitive in a rapidly evolving landscape. How can finance leaders overcome these challenges and start leveraging AI effectively?

A district court out of Missouri has served up a reminder as to the limitations of a motion to dismiss based upon subject matter jurisdiction. In May v. Consumer Adjustment Co., the consumer filed an FDCPA complaint is state court alleging that the initial demand letter violated 15 U.S.C. §1692g. May v. Consumer Adjustment Co., 2017 U.S. Dist. LEXIS 7401 (E.D.

A Virginia bankruptcy court recently ruled that an objection to a proof of claim was not barred by the doctrine of res judicata when an order of confirmation was entered prior to the objection being filed. In re Haskins, No. 15-60644 (W.D. Va. Jan. 27, 2017) [Dkt No. 31]. The creditor, a debt buyer, filed its unsecured proof of claim prior to confirmation of the debtor’s Chapter 13 plan.

Sign up to get articles personalized to your interests!

Creditor Collections Today brings together the best content for creditors and collection professionals from the widest variety of industry thought leaders.

A Virginia bankruptcy court recently ruled that an objection to a proof of claim was not barred by the doctrine of res judicata when an order of confirmation was entered prior to the objection being filed. In re Haskins, No. 15-60644 (W.D. Va. Jan. 27, 2017) [Dkt No. 31]. The creditor, a debt buyer, filed its unsecured proof of claim prior to confirmation of the debtor’s Chapter 13 plan.

The CFPB recently entered into consent orders with several Citibank subsidiaries attacking their mortgage servicing practices during the early days of the Mortgage Servicing Rules despite the CFPB’s assurances that early examinations would focus on efforts to comply rather than the technical aspects of compliance. The consent orders require CitiMortgage to pay $17 million to affected consumers and a $3 million civil penalty and require CitiFinancial Services to pay $4.4 million to affected consu

Simplicity Debt Collection Software is pleased to announce the roll out of its new Enterprise Debtor Payment Portal. This fully functional portal allows you to empower your debtors to make payments, settle accounts, set up payment plans, confirm their information and so much more. Use this application easily from your own website or direct them to our portal, either option is now available.

A district court from New York recently ruled that even assuming a creditor’s initial TILA disclosures fell short under the statutory requirements, the plaintiff must show an injury in fact in order to have standing under Article III. In Kelen v. Nordstrom , the plaintiff sued the retailer alleging the retailer’s disclosures in connection with its credit card accounts violated the Truth in Lending Act.

A demand letter sent by a debt collector was not doomed by an incorrect statement of the creditor’s name. In Santibanez v. National Credit Systems, Inc., the debt collector’s initial letter stated as follows: Re: ENCOMPASS MANAGEMENT CONSULTANTS Account #: 3118797 Balance: $875.33 Dear CARLOS SANTIBANEZ, It is imperative that you give this matter your prompt attention.

Finance isn’t just about the numbers. It’s about the people behind them. In a world of constant disruption, resilient finance teams aren’t just operationally efficient. They are adaptable, engaged, and deeply connected to a strong organizational culture. Success lies at the intersection of people, culture, adaptability, and resilience. Finance leaders who master this balance will build teams that thrive through uncertainty and drive long-term business impact.

The D.C. Circuit has vacated its prior order in PHH Corporation v. Consumer Financial Protection Bureau and ordered the matter be reheard en banc. The parties have been specifically asked to address the following issues in their briefs: Is the CFPB's structure as a single-Director independent agency consistent with Article II of the Constitution and, if not, is the proper remedy to sever the for-cause provision of the statute?

40

40

Input your email to sign up, or if you already have an account, log in here!

Enter your email address to reset your password. A temporary password will be e‑mailed to you.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content