This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

How to Rehabilitate a Debtor and Save a Profitable Customer By David Schmidt courtesy of Your Virtual Credit Manager Business customers pay for the goods and services they purchase from other companies. After all, a sale isn’t truly complete until it has been paid. Good customer purchases generate a profit for the seller, and I’m not just talking about gross margin.

Summons and complaints are the most important pleadings filed in debt collection litigation, which makes properly drafting summons and complaints incredibly important. A summons is a notice to the debtor that the creditor is filing a lawsuit against them. The complaint is the meat. It is where the creditor outlines the “legal cause of action” for the claim(s) the creditor has.

The answer could be different in an individual situation, but in commercial situations generally? The earlier the better. As soon as your ordinary, reasonable debt collection efforts have failed. Ballpark, a substantial receivable that is over 60 days late requires immediate action. That action needs to be more than just hiring a collections agency.

We spoke to the Chartered Institute of Credit Management’s North West Branch Chair, Chris Hardman MCICM, about his career in Credit. Chris started out in college, studying engineering, and fell into finance. When Chris was approached by the operations director at his organisation about the trouble with their collections, his chance to ‘have a go’ at a role, turned into his lifelong career.

AI is reshaping industries, yet finance remains one of the slowest adopters. Concerns over compliance, legacy systems, and data silos have made finance teams hesitant to embrace AI-driven transformation. But delaying adoption isn’t just about efficiency—it’s about staying competitive in a rapidly evolving landscape. How can finance leaders overcome these challenges and start leveraging AI effectively?

It appears as though the data breach at NCB Management Services has expanded and now involves more than 1 million consumers, after originally indicating that 500,000 consumers were affected when details were first released back in March.

When you're growing a business, a late-paying client can be frustrating. You have to dedicate time and resources to figure out what happened and why. You have to pull yourself together enough to have a conversation about money - something that's not easy for many people. The most important thing to remember is that your business fulfilled its part of the deal, and now your client owes your business.

Sign up to get articles personalized to your interests!

Creditor Collections Today brings together the best content for creditors and collection professionals from the widest variety of industry thought leaders.

When you're growing a business, a late-paying client can be frustrating. You have to dedicate time and resources to figure out what happened and why. You have to pull yourself together enough to have a conversation about money - something that's not easy for many people. The most important thing to remember is that your business fulfilled its part of the deal, and now your client owes your business.

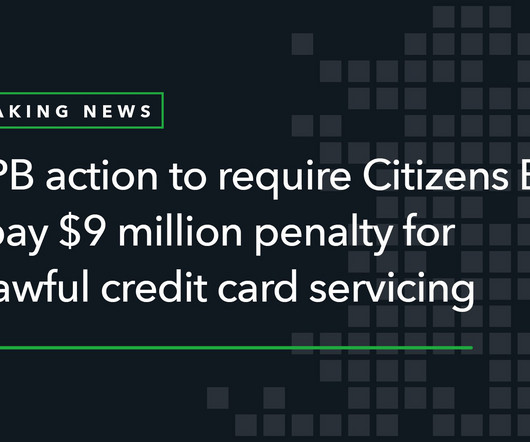

Today, the Consumer Financial Protection Bureau (CFPB) reached a settlement to resolve CFPB’s allegations that Citizens Bank violated consumer financial protection laws and rules that protect individuals when they dispute credit card transactions.

EDITOR’S NOTE: This article is part of a series that is sponsored by WebRecon. WebRecon identifies serial plaintiffs lurking in your database BEFORE you contact them and expose yourself to a likely lawsuit. Protect your company from as many as one in three new consumer lawsuits by scrubbing your consumers through WebRecon first. Want to learn more?

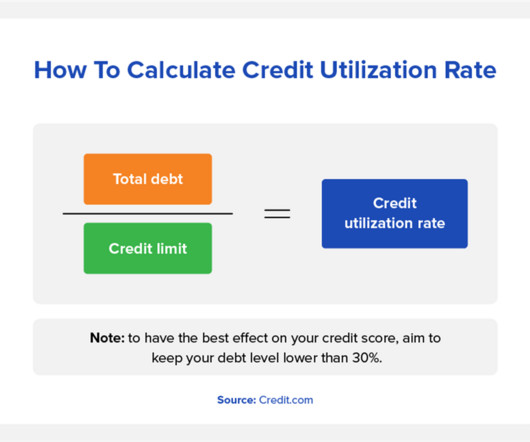

Your credit score may have dropped if you applied for a new card or line of credit or were late on payments or there was fraudulent behavior on your account, among other reasons. You check your credit score routinely, but one day, surprised, yougasp at the number, wondering, “Why has my credit score suddenly dropped!?” Don’t panic—there are a multitude of reasons why.

Finance isn’t just about the numbers. It’s about the people behind them. In a world of constant disruption, resilient finance teams aren’t just operationally efficient. They are adaptable, engaged, and deeply connected to a strong organizational culture. Success lies at the intersection of people, culture, adaptability, and resilience. Finance leaders who master this balance will build teams that thrive through uncertainty and drive long-term business impact.

Many individuals and businesses face financial challenges in today’s fast-paced and unpredictable economy. When debt becomes overwhelming and difficult to manage, filing for bankruptcy can provide a fresh start and relief from mounting financial burdens. However, despite its potential benefits, some people hesitate to consider bankruptcy a viable solution.

Obtaining a settlement in a Fair Debt Collection Practices Act case does not necessarily make you the prevailing party and entitle you to attorney’s fees, a District Court judge in Texas has ruled in a case that was remanded back from the Court of Appeals for the Fifth Circuit.

Predicting the future credit landscape is always difficult for companies, even in the best of times. However, it is clear that the quality of available data and the way it is delivered and used will determine this future picture. Live and up-to-date data are therefore crucial for financial professionals who want to make the right choices and minimise risks.

Your past-due accounts are growing, cash flow is tightening, and the pressure is on. The big question: Do you handle the collections internally or outsource to experts? Both strategies come with advantages and risks - but which one delivers the best impact for your business? In this session we’ll dive deep into the in-house vs. outsourcing debate, examining cost-effectiveness, efficiency, compliance risks, and overall recovery success rates.

Financial hardship is not an easy thing for anyone to face. Sadly, the reality is that millions of people in the United States are struggling just to cover their household bills. When debt becomes insurmountable, it can feel like there are no options available. However, there are strategies that can help to provide debt relief. One option is to file for bankruptcy.

Chapter 7 bankruptcy (the most common form of bankruptcy ) essentially wipes away a large portion of your unsecured debts and protects certain assets you may possess. Briefly, unsecured debts are not backed by any collateral. Unlike car and home loans, unsecured debt means that creditors aren’t able to reclaim property if you default. Credit card and medical debt are examples of unsecured debt.

The New York State Department of Financial Services has fined OneMain Financial $4.25 million for violating the state’s cybersecurity regulations by failing to manage third-party service provider risk, access privileges, and for failing to maintain a formal application security development methodology. A copy of the consent order can be accessed by clicking here.

Predicting the future credit landscape is always difficult for companies, even in the best of times. However, it is clear that the quality of available data and the way it is delivered and used will determine this future picture. Live and up-to-date data are therefore crucial for financial professionals who want to make the right choices and minimise risks.

Speaker: Brian Muse-McKenney, Chief Revenue Officer & Matt Simester, Cards and Payments Expert

In today’s world of social media, dating apps, and remote work, businesses risk becoming irrelevant (or getting "ghosted") if they fail to meet the evolving needs of Gen Z consumers. Credit cards with flexible payment options, especially for young adults with little-to-no credit history, are a particularly important and valuable solution for this generation.

We spoke to the Chartered Institute of Credit Management’s North West Branch Chair, Chris Hardman MCICM, about his career in Credit. Chris started out in college, studying engineering, and fell into finance. When Chris was approached by the operations director at his organisation about the trouble with their collections, his chance to ‘have a go’ at a role, turned into his lifelong career.

To help you keep abreast of relevant activities, below find a breakdown of some of the biggest events at the federal and state levels to impact the Consumer Finance Services industry this past week: Federal Activities State Activities Federal Activities: On May 19, the Federal Reserve Bank of New York’s New York Innovation Center (NYIC) and the Monetary Authority of Singapore (MAS) published a joint research report of Phase II of Project Cedar and the MAS’ Ubin+ Project, both of which seek to un

Getting most of the state Attorneys General to agree on anything is like herding cats, so when most of them come together, it’s likely to be something big. Forty-nine AGs announced earlier this week that they were filing a joint lawsuit against a telecom company accused of facilitating billion of robocalls to consumers nationwide.

Predicting the future credit landscape is always difficult for companies, even in the best of times. However, it is clear that the quality of available data and the way it is delivered and used will determine this future picture. Live and up-to-date data are therefore crucial for financial professionals who want to make the right choices and minimise risks.

Navigating collections in the dynamic financial landscape presents multifaceted challenges. Organizations face pressures to maintain standards alongside software challenges like regulatory adaptations, data integration, security, workflow optimization, and automation. Finding the right software can save time and money. BEAM offers a comprehensive solution with specialized modules to streamline debt collection effortlessly.

Florida law allows for a private cause of action for a party’s violation of the Florida Building Code (the “Code”). See 553.84 of the Florida Statutes. There is no requirement for a party to have contact in order to bring a claim for a building code violation, thus, allowing a subsequent purchaser to bring a claim against the party that committed that violation.

CLASS-ACTION ACCUSES COLLECTOR OF USING INCORRECT ITEMIZATION, VALIDATION DATES IN MVN Regulation F requires collectors to give consumers 30 days to request validation of a debt with the clock starting to tick five days — excluding legal holidays, Saturdays, and Sundays — after a notice is sent.

October is security month at Visma, but online safety should happen all year round. We are discussing Red Teams and how they help to make the internet a safer place for everyone. With the high increase in cyber crime all over the world, many people and organisations are worried about becoming the next victim. In order to protect yourself, you’ll need to ask a fundamental question: how exactly can cyber criminals attack you?

CPAs know the drill: taxes, compliance, rinse, repeat. But what about the sneaky cash flow that’s quietly messing with your organization’s success? It’s time to step into the spotlight and expose the “dirty little secrets” of cash flow to fuel strategic growth. By upskilling your accounting practices and shifting focus from tax compliance to the strategic movement of money, you can transform your role from reactive accountant to proactive financial strategist.

Input your email to sign up, or if you already have an account, log in here!

Enter your email address to reset your password. A temporary password will be e‑mailed to you.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content