This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Eng, and Chenxi Jiao Lenders, mortgage servicers, and other financialinstitutions should take note that the New York State legislature has extended the COVID-19 Emergency Eviction and Foreclosure Prevention Act (“CEEFPA”) and the COVID-19 Emergency Protect Our Small Businesses … Continue reading →

On Tuesday, March 23, 2021, four of our partners presented Properly Handling Mortgage Foreclosures. This presentation was moderated by the firm’s managing partner, and is geared towards special asset departments of banks and financialinstitutions. The borrower filed for bankruptcy during the foreclosure lawsuit.

Eng, and Chenxi Jiao Financialinstitutions, lenders, and servicers should take note that the United States Supreme Court (“SCOTUS”) granted an injunction filed by plaintiffs-landlords seeking to prevent the enforcement of New York’s COVID-19 Emergency Eviction and Foreclosure … Continue reading →

Eng, and Alina Levi Lenders, mortgage servicers, and other financialinstitutions should take note that New York State passed legislation extending the protections set forth in the COVID-19 Emergency Eviction and Foreclosure Prevention Act of 2020 … Continue reading → Wayne Streibich, Diana M.

Chase was one of 13 financialinstitution censured for robo-signing documents in support of debt collection suits and foreclosure. The investigation was settled and Chase was to adhere to an order demanding an end to the practice. But robo-signing wasn’t just happening within Chase.

Brenda’s still tending her garden, though, thanks to a second-chance loan from the New Hampshire Community Loan Fund-a Community Development FinancialInstitution (CDFI). Sometimes it’s a foreclosure, increasingly often it’s due to large medical bills,” Pinsky notes. Virtually all the folks we see have low credit scores.

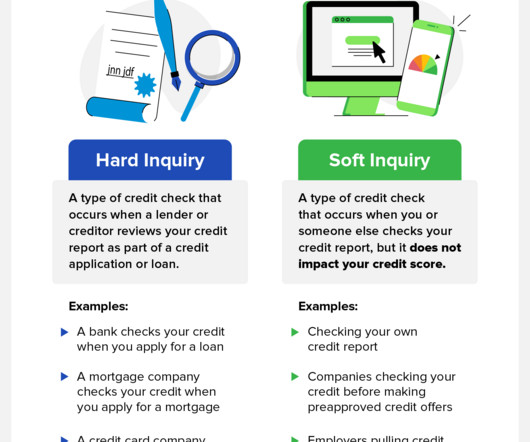

Hard inquiries , also known as hard pulls, are typically made by lenders and other financialinstitutions and can harm your credit score. Check with your financialinstitution to see if they offer this service and how you can access your score. What’s a Hard Inquiry? Credit inquiries can be found on your credit report.

At the beginning of the lockdowns a former colleague described the problem facing financialinstitutions as a ‘portfolio of good quality customers facing a temporary shock to their income, all they need is a bit of immediate assistance’. This however creates another problem for bank balance sheets.

A lender must enforce the debt through foreclosure or a lawsuit within six years after the cause of action accrues. The third party filed suit against FMZ for quiet title, claiming the six-year statute of limitations barred foreclosure and FMZ’s ability to enforce its title to the property.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. For more information, click here. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. For more information, click here. For more information, click here.

During the 2008 financial crisis downturn, banks were giving loans to anyone to make more and more money while selling mortgages to poor credit individuals. Their greed eventually reached a point where many homeowners could not make their mortgage payments causing foreclosures, and eventually, a recession.

When the Federal Reserve raises interest rates, financialinstitutions increase their rates accordingly, so those with variable interest rate loans may need to pay more interest than when they initially borrowed the money. Filing for Chapter 13 bankruptcy is also critically important if you’re at risk of home foreclosure.

Still, it appears the court discharged the creditor’s debt primarily because the court considered it to be inequitable to require a debtor to claim cancellation of debt income as gross income while still allowing the creditor to then collect it from the debtor.

Overall, the CDCIA’s proposed changes to consumer finance laws tend to support pro-consumer policies and will require financialinstitutions, debt collectors, and loan servicers to re-evaluate their business practices if the bill is ultimately passed.

COAF is the auto financing arm of the popular financialinstitution Capital One. Foreclosures. We’ll also give you a few pointers on getting COAF off your credit report if you didn’t apply for an auto loan with the company. What Is COAF? It offers loans for new and used vehicles, along with refinancing options. Charge offs.

The Nevada FinancialInstitutions Division is reminding licensed collection agencies that collect residential debt for unit-owners’ associations of common-interest communities to file their report required by Senate Bill 186 by Jan. Source- site.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. State Activities. Privacy and Cybersecurity Activities.

He represents various financialinstitutions, creditors, landlords, and other parties in all aspects of loan modifications and restructuring, commercial foreclosures, enforcement of security interests and domestic and foreign judgments, Chapter 7 and 11 bankruptcies, and creditors’ rights litigation.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. According to the FOMC, inflation continues to run below 2%. For more information, click here.

A recent decision from a Louisiana district court should provide some comfort to banks and other financialinstitutions who acquire other entities by merger – at least in the Fifth Circuit, they are not debt collectors. As most know, Bank of America (BoA) acquired Countrywide Bank FSB and its mortgage portfolio in 2008. In Jackson v.

On July 27, the Senate passed its version of the National Defense Authorization Act (NDAA) bill, which includes a provision that tightens oversight over financialinstitutions engaged in crypto trading and takes aim at crypto mixers and “anonymity-enhancing” crypto assets. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. On October 26, the Nevada’s FinancialInstitutions Division is holding a workshop on regulations pertaining to medical debt collections and S.B.

The court found that the defendants falsely promised to reduce homeowners’ mortgage payments and prevent foreclosures, defrauding distressed homeowners out of millions of dollars. Hsu discussed the importance of eliminating appraisal bias in the financial industry in remarks at an Appraisal Subcommittee (ASC) Hearing.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. Specifically, the bill included a requirement that the Nevada FinancialInstitutions Division license the app.

Instead, banks, lenders, and other financialinstitutions turn to consumer credit reporting companies like CBCInnovis to vet applicants. Foreclosures. While you may have applied for a loan from a popular lender or bank, their name isn’t necessarily the one that will appear on your credit report. Charge offs. Debt in collections.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. The PPP will open to all participating lenders shortly thereafter.

Financialinstitution. Foreclosure. Headquartered in Beachwood, Ohio, the agency has been operating since 1970. Over the past 50 years, FFCC has collected debts in the following industries: Business to business. Healthcare. If you carry debt in any of those industries, the entry featured on your report could be legitimate.

Citibank is a major financialinstitution that offers credit cards in partnership with numerous retailers, including: Best Buy. Foreclosure. In the article below, we’ll break down the details of the NTB/CBNA credit card, how a hard inquiry works, and what you can do to get an inaccurate inquiry off your report. Brooks Brothers.

Employers interested in creating an automatic savings program as a way for employees to build emergency savings and increase their financial resiliency would be able to use the CAST Template as the basis for an application. For more information, click here. For more information, click here.

On the other hand, when you complete an application for some form of credit or other financial product, your report may undergo a hard inquiry. That’s where the lender or financialinstitution requests your full credit report from one or all of the major credit bureaus to vet you and assess the risk involved in approving your application.

In the areas of banking, commercial, construction and real estate litigation, he represents lenders, contractors and owners on construction-related claims, and lenders and borrowers in commercial and residential foreclosure matters, large loan defaults and collections, lien priority disputes, and title insurance company liability.

are part of this program, where FICO Scores used by financialinstitutions are shared with consumers for free. Then, again, with our FICO ® Score Open Access program that we launched in 2013. Hundreds of lenders in the U.S.

It involves qualifying and applying for a revolving credit line through a lender, usually a bank or other financialinstitution. Lenders grant a card with a specific credit limit based on a consumer’s credit rating, credit history, financial situation, as well as their relationship with the customer. trillion.

If you see an old phone number, chances are it is still on file with the financialinstitution that issued the loan or credit card. The public records section will include any type of financial, or legal action against you. Foreclosure. Phone Numbers: You’ll see phone numbers associated with your credit accounts.

The first of its kind, the strategy examines the phenomenon of financialinstitutions de-risking and its causes, and it identifies those greatest impacted. Department of the Treasury issued the 2023 De-Risking Strategy, as mandated by Congress in the Anti-Money Laundering Act of 2020. For more information, click here.

Attorneys who collect for national banks, debt buyers or other financialinstitutions have been regular targets in FDCPA class actions. Attorneys who engage in collection work for community associations, however, have managed to remain off of the FDCPA class action radar. JQD, LLC , 2014 WL 3404945 (N.D.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link].

Financialinstitutions, servicers, lenders, and debt collectors must stay up-to-date on evolving federal and state laws stemming from the COVID-19 pandemic, as such laws impact all facets of consumer loan servicing and debt collection.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The eviction moratorium law is part of New York state’s COVID-19 Emergency Eviction and Foreclosure Prevention Act of 2020.

On October 23, the Federal Reserve and Financial Crimes Enforcement Network (FinCEN) invited comment on a proposed rule change, requiring financialinstitutions to keep more records on hand related to smaller-value international fund transfers. For more information, click here. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The seven rescissions provide guidance to financialinstitutions on complying with their legal and regulatory obligations.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. On April 13, U.S.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The program will invest $9 billion in community development financialinstitutions and minority depository institutions.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content