This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And her bank wouldn’t give her and her husband Larry a loan to buy a replacement home. Brenda’s still tending her garden, though, thanks to a second-chance loan from the New Hampshire Community Loan Fund-a Community Development FinancialInstitution (CDFI). Flexible loan amounts. Flexible loan amounts.

On Tuesday, March 23, 2021, four of our partners presented Properly Handling Mortgage Foreclosures. This presentation was moderated by the firm’s managing partner, and is geared towards special asset departments of banks and financialinstitutions. The borrower filed for bankruptcy during the foreclosure lawsuit.

The six month pause on payments instituted by Australian Banks was certainly not designed to accommodate the situation we now find ourselves in. Further assistance was announced in July offering customers a further four month deferral or the option to restructure their loan. This also has implications for the property market.

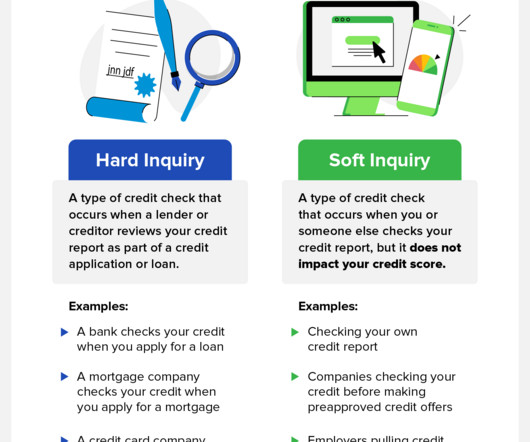

Whether you’re applying for a loan or simply want to stay on top of your credit score, these tips will help you access your credit information without causing any harm. Hard inquiries , also known as hard pulls, are typically made by lenders and other financialinstitutions and can harm your credit score. What’s a Hard Inquiry?

Raising interest rates typically slows down the economy as well as the rate of inflation, but these rates have a direct impact on people’s ability to obtain new loans. Here’s what you need to know about getting a new loan and interest rate after bankruptcy. Usually, this is cents on the dollar.

A lender must enforce the debt through foreclosure or a lawsuit within six years after the cause of action accrues. A recent decision provides further guidance for lenders and loan servicers enforcing land sale contracts where title to the property does not transfer until the loan is paid in full. In Velazquez v.

Hard inquiries are often the result of a credit card or a loan application, and COAF is no exception. COAF may appear on your report after you apply for an auto loan or buy a car with funding from Capital One. Your report may also show a hard inquiry from COAF if you agreed to be a cosigner for someone else’s car loan application.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The rules cover loans on principal residences, generally exclude small servicers, and will take effect on August 31.

The first consideration that lenders (banks and credit unions alike) often face is when, and if, to conclude that the account owner does not intend to, or is not able to, clear the negative balance or loan deficiency. As a result, a loan that is charged off is written off and deemed a loss of principal and interest. See Caplinger v.

Prohibiting servicers of private education loans from reporting an adverse item of information relating to the nonpayment of the loan for an established period of time. Prohibiting servicers of private education loans from reporting an adverse item of information relating to the nonpayment of the loan for an established period of time.

During the 2008 financial crisis downturn, banks were giving loans to anyone to make more and more money while selling mortgages to poor credit individuals. Their greed eventually reached a point where many homeowners could not make their mortgage payments causing foreclosures, and eventually, a recession.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. Among other provisions, S.B. For more information, click here and here. For more information, click here. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. State Activities. Privacy and Cybersecurity Activities. Federal Activities: On September 1, the U.S.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. Current provisions in federal law will allow federal borrowers to seek cancellation if their institution engaged in certain misconduct.

A recent decision from a Louisiana district court should provide some comfort to banks and other financialinstitutions who acquire other entities by merger – at least in the Fifth Circuit, they are not debt collectors. As most know, Bank of America (BoA) acquired Countrywide Bank FSB and its mortgage portfolio in 2008. In Jackson v.

An entry from CBCInnovis could be the result of several types of loan applications. While you may have applied for a loan from a popular lender or bank, their name isn’t necessarily the one that will appear on your credit report. Soft pulls happen when you check your score with a credit monitoring app or pre-qualify for loan offers.

He represents various financialinstitutions, creditors, landlords, and other parties in all aspects of loan modifications and restructuring, commercial foreclosures, enforcement of security interests and domestic and foreign judgments, Chapter 7 and 11 bankruptcies, and creditors’ rights litigation.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. On March 24, the Consumer Financial Protection Bureau (CFPB) provided Congress its Consumer Response Annual Report for 2020.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. On October 4, the CFPB announced that the deadline to request initial forbearance for loans backed by the U.S.

The court found that the defendants falsely promised to reduce homeowners’ mortgage payments and prevent foreclosures, defrauding distressed homeowners out of millions of dollars. On February 15, the CFPB published a blog recounting its action against a student loan debt relief business and a debt-settlement company.

If you see an old phone number, chances are it is still on file with the financialinstitution that issued the loan or credit card. The types of credit accounts you can expect to see in this section include: Mortgages , home equity loans, and home equity lines of credit. Student Loans. Auto Loans.

Citibank is a major financialinstitution that offers credit cards in partnership with numerous retailers, including: Best Buy. Soft inquiries happen when you pre-qualify for a credit card or loan, compare quotes, check your score, or get vetted for a job or apartment application. Foreclosure. Brooks Brothers.

Employers interested in creating an automatic savings program as a way for employees to build emergency savings and increase their financial resiliency would be able to use the CAST Template as the basis for an application. The SBA has prohibited banks from favoring a PPP loan application from a director or equity holder.

On July 27, the Senate passed its version of the National Defense Authorization Act (NDAA) bill, which includes a provision that tightens oversight over financialinstitutions engaged in crypto trading and takes aim at crypto mixers and “anonymity-enhancing” crypto assets. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The PPP will open to all participating lenders shortly thereafter.

On October 11, an automotive management company settled claims by the Department of Justice (DOJ) alleging that the company had violated the False Claims Act by knowingly providing false information in support of its Paycheck Protection Program (PPP) loan forgiveness application. For more information, click here.

It involves qualifying and applying for a revolving credit line through a lender, usually a bank or other financialinstitution. Lenders grant a card with a specific credit limit based on a consumer’s credit rating, credit history, financial situation, as well as their relationship with the customer.

On May 1, the CFPB proposed a rule to implement a congressional mandate to establish consumer protections for residential property assessed clean energy (PACE) loans. PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels.

That’s because applying for a credit card, loan, or in this case a Mastercard, often results in banks and lenders checking your credit report. When you shop for online quotes or seek to get pre-approved for loan rates, the process should only involve a soft credit check, which simply verifies your credit score without lowering it.

In the areas of banking, commercial, construction and real estate litigation, he represents lenders, contractors and owners on construction-related claims, and lenders and borrowers in commercial and residential foreclosure matters, large loan defaults and collections, lien priority disputes, and title insurance company liability.

are part of this program, where FICO Scores used by financialinstitutions are shared with consumers for free. Then, again, with our FICO ® Score Open Access program that we launched in 2013. Hundreds of lenders in the U.S.

Attorneys who collect for national banks, debt buyers or other financialinstitutions have been regular targets in FDCPA class actions. Countrywide Home Loans, Inc., 2014) (collection complaints violated the FDCPA where they identified incorrect “original” creditor that had made the loans to class members); McCollough v.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. Borrowers deserve and desperately need relief from their Federal student loan burden, and they need that relief immediately.”

Department of Education announced an extension of its pause on student loan repayment, interest, and collections through August 31, 2022. Instead of using the payment plans, borrowers continue to pay for costly loan rollovers. On April 6, the U.S. For more information, click here. For more information, click here.

Financialinstitutions, servicers, lenders, and debt collectors must stay up-to-date on evolving federal and state laws stemming from the COVID-19 pandemic, as such laws impact all facets of consumer loan servicing and debt collection.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The 2020 review found that credit risk for large, syndicated loans has increased over the last year. On February 25, U.S.

On October 23, the Federal Reserve and Financial Crimes Enforcement Network (FinCEN) invited comment on a proposed rule change, requiring financialinstitutions to keep more records on hand related to smaller-value international fund transfers. For more information, click here. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The seven rescissions provide guidance to financialinstitutions on complying with their legal and regulatory obligations.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. On April 13, U.S. The company was operating without registering as a debt settlement service provider as required by Minnesota law.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. Currently, any student loan debt canceled by the government can be considered taxable and levied at the borrower’s normal income tax rate.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. House of Representatives that would extend the payment pause and interest waiver for government-held federal student loans.

The FTC alleged that the defendants pretended to be affiliated with the Department of Education, charged illegal junk fees, and offered students loan forgiveness promises that were not fulfilled. For more information, click here. An emergency amendment, B25-0449, was also introduced by Councilmember White on the same day.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. For more information, click here. On May 13, the U.S. For more information, click here.

On December 1, the House of Representatives approved a resolution to repeal a Consumer Financial Protection Bureau (CFPB) rule that mandated banks to gather data on loan applications from women-owned, minority-owned, and small businesses to help lenders identify business development needs and opportunities.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content