This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Why it matters: If passed, these bills could significantly weaken the CFPBs ability to regulate financialinstitutions and enforce consumer protection laws. This would be a major win for lenders, debt collectors, and financial service providers, while consumer advocates warn it could reduce oversight of abusive practices.

Credit card lenders and financialinstitutions are apparently a little leery of the state of the economy and consumer’s ability to meet their financial obligations and are keeping balance limits largely stationary for the time being, except for one group of consumers — and it’s probably not the group you would guess — according (..)

The Consumer Financial Protection Bureau has officially signaled it plans to rewrite its small business lending data collection rule, known as Section 1071, following major leadership changes earlier this year.

Updates to the Gramm-Leach-Bliley Act (GLBA), the Safeguards Rule , provide financialinstitutions, including those in the accounts receivable management industry, with requirements on how to safeguard customer information, went into effect on June 9. Cost-effective customer communications at scale. Online payment portals.

Brenda’s still tending her garden, though, thanks to a second-chance loan from the New Hampshire Community Loan Fund-a Community Development FinancialInstitution (CDFI). Small loans like these are typically not attractive to larger financialinstitutions, who may not find them profitable enough. Better loan terms.

The good news for lenders and debt collectors is that a reported 72% of consumers have a New Years resolution to pay off debt in 2025. CFPB Looks at Medical Debt, Student Loans and So Much Data Medical debt wasnt the only focus for the Consumer Financial Protection Bureau in Q4.

On October 27, the Federal Trade Commission (FTC) announced a final rule (Final Rule), amending the Standards for Safeguarding Customer Information (Safeguards Rule) under the Gramm-Leach-Bliley Act (GLBA) as it applies to covered financialinstitutions. Expanded Definition of “FinancialInstitution”.

A trade group representing non-bank financialinstitutions that provide sales-based financing to businesses has filed a lawsuit against the Consumer Financial Protection Bureau claiming it has overstepped its authority by issuing a rule regulating how lenders must collect and submit data related to small business lending activities.

Most SBA loans are issued by banks, credit unions and other financialinstitutions, not the government. The best lenders have substantial experience with these small-business loans, so you get effective help during the application process and hopefully increase your chances of approval. Randa Kriss writes for NerdWallet.

When account owners have an account that reflects a negative balance, the lender is faced with a myriad of options and obligations with regard to the pursuit of that debt. Lenders that charge off a debt trigger issuance of the 1099-C when their defined policy leads the lender to discontinue collection activity and discharge a debt.

One area the CFPB identified as a consumer harm is when financialinstitutions charge a consumer overdraft fees because the institutions failed to lift the initial automatic holds on the amounts of mobile check deposits after an additional suspicious deposit hold was placed on the account. Prepaid Accounts.

Banks, lenders, and other financial players are accelerating their digital transformation roadmaps, shortening years’ worth of development into mere months, in an attempt to service consumers at scale while managing the complexities of our new normal and the limitations of outdated infrastructure.

One area the CFPB identified as a consumer harm is when financialinstitutions charge a consumer overdraft fees because the institutions failed to lift the initial automatic holds on the amounts of mobile check deposits after an additional suspicious deposit hold was placed on the account. Prepaid Accounts.

In recent years, the rise of digital lenders like SoFi and Ally has transformed the lending landscape, offering borrowers new options for obtaining loans quickly and conveniently. But what sets these digital lenders apart from traditional banks and credit unions? And how can you navigate the process of shopping for a loan with them?

While a “C” average may feel middle-of-the-road on an academic scale, nailing the five C’s of credit is the key to getting business funding from banks and other financialinstitutions. Jackie Zimmermann is a writer at NerdWallet. Email: articles@nerdwallet.com.

THE NEW ERA OF CONSUMER LENDING In today ’ s rapidly evolving financial landscape, the significant increase in consumer lending presents new challenges for financialinstitutions, particularly in managing collections. INTRODUCING QCR ACCELERATOR The QCR Accelerator is a collections solution developed by QUALCO.

CFS Partner Lori Sommerfield brings more than two decades of experience in representing a wide range of banks, financialinstitutions, and financial services companies in fair lending and responsible banking regulatory compliance.

Banks are accelerating their adoption of new digital debt collection tools in anticipation of a “tidal wave of consumer debt issues” when government stimulus programs end and financialinstitutions stop offering forbearance and loan deferral options. About TrueAccord.

While creditors weren’t looking up someone’s history of debt and payments, many lenders did take risk-mitigation actions. 1960s: Credit reporting bureaus “sponsored” by banks or other financialinstitutions didn’t share information outside of their networks. The concept of credit reporting may be almost as old.

Worries from the credit card processor and/or their lender that they won’t be repaid. The laundry list of situations that constitute a default makes it far easier for a buyer to “default,” which enables the lender to accelerate payment, penalties, and the like. That is unless you are put out of business by the lender.

Eng, and Chenxi Jiao Lenders, mortgage servicers, and other financialinstitutions should take note that the New York State legislature has extended the COVID-19 Emergency Eviction and Foreclosure Prevention Act (“CEEFPA”) and the COVID-19 Emergency Protect Our Small Businesses … Continue reading →

Minority business loans are available from many lenders. But getting funding from a traditional financialinstitution may be tougher for minority business owners due to issues like unconscious bias, insufficient credit and limited banking history. In fact, a 2019 report.

When financialinstitutions enact this fine print tactic to try to trick consumers into believing they have given up certain legal rights or protections, they now risk violating the Consumer Financial Protection Act. “The Its reputation as the “Consumer Watchdog” continues to be well-earned as the economic landscape evolves.

Lenders face a myriad of challenges these days. A pooled model is a scoring model built on “pools” of historical data from many financialinstitutions. No data is required from the customer because it’s built on pools of historical data from other financialinstitutions. What Is a Pooled Model?

That makes clear the need for financialinstitutions to apply different recovery strategies according to the segment a customer is included. In that context, analytics can bring true value for lenders. By using state-of-the-art technology to segment their customers, lenders will be armored to make better-informed decisions.

That makes clear the need for financialinstitutions to apply different recovery strategies according to the segment a customer is included. In that context, analytics can bring true value for lenders. By using state-of-the-art technology to segment their customers, lenders will be armored to make better-informed decisions.

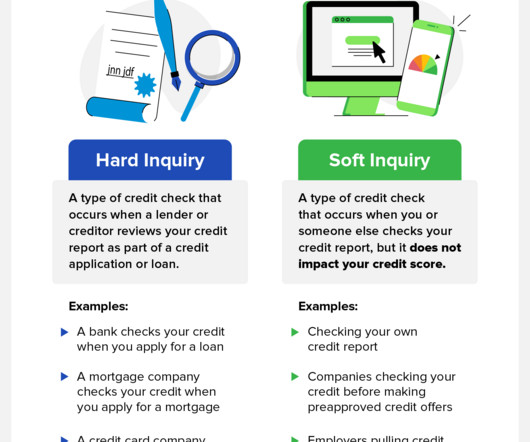

Your credit score is an important aspect of your financial health and is oftentimes used by lenders, landlords, and even employers to determine your creditworthiness. Hard inquiries , also known as hard pulls, are typically made by lenders and other financialinstitutions and can harm your credit score.

DeFi decreases the barrier of entry to financial products and services for people who are unbanked from traditional financial services because of significant reasons, such as lack of credit history, weak banking infrastructure, or limited banking hours. What is so special about DeFi?

In a major victory for small business lenders, yesterday the U.S. Supreme Court reverses the Fifth Circuit in Community Financial Services Association v CFPB (CFSA case), which found the CFPB’s funding structure unconstitutional. A discussion of the preliminary injunction issued by that Texas federal court on July 31 can be found here.

The UK’s Financial Conduct Authority (FCA) has handed out a £26m fine following poor treatment of more than 1.5 It marks the highest fine ever issued to a lender for what it deemed a breach of consumer credit rules. As we pass the first anniversary of the pandemic’s outbreak, where does this leave lenders?

According to the Federal Reserve’s 2021 Small Business Credit Survey, banks remain the most common source of credit for small businesses — compared with options such as online lenders, community development financialinstitutions or credit unions. Randa Kriss writes for NerdWallet.

Online lenders make it easy to compare rates and terms and find the right online personal loan for your situation. That is, the lender advances you money that you pay back with interest over a predetermined period of time. This often allows digital lenders to streamline the applications. Benefits of Online Personal Loans.

In that context, lenders need to have access to state-of-the-art technology to avoid major losses. What is vital in this part, is that ML can adapt when conditions change, meaning it can add new data and re-run the analysis in real-time so that lenders can form a new strategy in a blink of an eye. The problem.

Synthetic identity fraud is so dangerous because it tends to go undetected for long periods of time, as there is no individual who has had their identity stolen to realize what is happening and alert financialinstitutions. This post is the first in a series looking at the issues around both first-party and synthetic identity fraud.

22-(R22-011) , concluding earned wage access (EWA) products that are fully non-recourse and no-interest are not “consumer lender loans” under Arizona law. Thus, those who make, procure, or advertise EWA products are not required to be licensed as a “consumer lender” by Arizona’s Department of Insurance and FinancialInstitutions.

Customers are becoming more sophisticated and the same goes with the solutions they expect from financialinstitutions. External events like the pandemic will continue to transform customer behavior in a permanent manner. Luckily, customer data are flowing like an ocean around us. That is where customer analytics comes in.

Incorrect Personal Information Lender Inquiries You Don’t Recognize Accounts You Never Opened Credit Utilization Goes Up Credit Score Goes Up or Down Unexpectedly Public Records You Don’t Recognize. Warning Sign 2: Lender Inquiries You Don’t Recognize. Warning Signs of Identity Theft. How Do I Check My Credit for Identity Theft?

Origination is just the initial phase of the long and complex mortgage lifecycle, which begins with a lender qualifying a borrower and then providing the funds used to purchase a new property or refinance an existing property. The lender then holds the mortgage on its balance sheet or sells the mortgage on the secondary market to investors.

In its recent blog post, the CFPB is clearly signaling that the practice of withholding transcripts as a debt collection tactic does not make much sense to the Bureau, stating: “It is particularly perplexing, as it can undermine rather than enhance a student’s likelihood of repaying.”

This partnership will undoubtedly enhance the impact SpringFour has on improving financial well-being for individuals and families across the nation.” About CORA GroupCORA Group is a collective organization redefining advancement through the acquisition, strengthening, and growth of over 30 independent software brands worldwide.

Whether you're a financialinstitution, a private lender, you can't be too careful when it comes to verifying the identity of your customers. We all love the convenience of making purchases, opening accounts, and applying for jobs from our computers or smartphones.

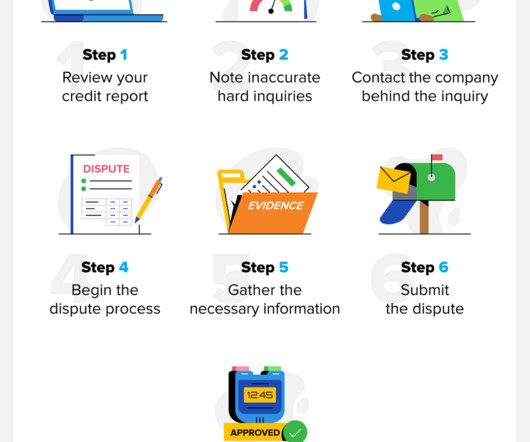

Whether you’re looking to buy a house, lease a car, or get a loan, lenders need to check your credit. In some cases, these lenders will remove the reports without conducting a formal dispute. Step 4: Begin the Dispute Process You can file a formal dispute if the lender doesn’t remove the inquiry from your informal request.

By communicating at the right time in the right channel with payment options that meet consumer needs, TrueAccord provides exceptional recovery rates for top 10 financialinstitutions, debt buyers, lenders, and technology companies.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content