This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Everything is online these days—including personalloans. Online lenders make it easy to compare rates and terms and find the right online personalloan for your situation. Personalloans were the fastest-growing category of consumer debt in 2019 , according to a survey from J.D.

A personalloan is money borrowed from a lender that can be used for almost any purpose, from debt consolidation to home improvement projects. Most people don’t have $5,000+ sitting in their bank accounts—that’s where personalloans come in. What Is a PersonalLoan? Why Would I Need a PersonalLoan?

Whether you’re making a big purchase or just refinancing some existing debt, a personalloan could help. But comparing loan options could take days — unless you use an online marketplace like Fiona which lets you compare personalloan offers side by side within minutes. How Fiona Loans Work.

Each year, tens of millions of Americans facing similar situations turn to personalloans to help ease the financial burden. With low interest for borrowers with strong credit scores, fixed rates, and a variety of lending sources to choose from, it’s easy to see why personalloans are so enticing. Rates & Fees.

And her bank wouldn’t give her and her husband Larry a loan to buy a replacement home. Brenda’s still tending her garden, though, thanks to a second-chance loan from the New Hampshire Community Loan Fund-a Community Development FinancialInstitution (CDFI). Support beyond the loan. Better loan terms.

The best personalloans charge low fees and low fixed interest rates, have flexible loan amounts and terms, and have no prepayment penalties. A personalloan could let you access cash for any purpose. Since personalloans are unsecured, you’ll need an excellent credit score to get the best deal.

When filing for bankruptcy, you can discharge certain types of personalloans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personalloans you can discharge and which filing method suits your financial situation.

Updates to the Gramm-Leach-Bliley Act (GLBA), the Safeguards Rule , provide financialinstitutions, including those in the accounts receivable management industry, with requirements on how to safeguard customer information, went into effect on June 9. Indicators show that delinquency is here to stay. increase month over month in May.

If you need money now, an online personalloan can be a fast and easy way to secure funds. Whether they’re for debt consolidation, a home improvement project, or other expenses, these loans often come with low-interest rates and flexible repayment options. Ad If you're struggling to make ends meet, a PersonalLoan can help.

THE NEW ERA OF CONSUMER LENDING In today ’ s rapidly evolving financial landscape, the significant increase in consumer lending presents new challenges for financialinstitutions, particularly in managing collections. INTRODUCING QCR ACCELERATOR The QCR Accelerator is a collections solution developed by QUALCO.

These loans often have low interest rates and are accessible to those with poor or nonexistent credit. That’s because you provide all of the collateral for the loan in cash, so it’s not a risk for the lender. Interest rates are typically much lower than credit cards or unsecured personalloans as well.

In recent years, the rise of digital lenders like SoFi and Ally has transformed the lending landscape, offering borrowers new options for obtaining loans quickly and conveniently. But what sets these digital lenders apart from traditional banks and credit unions?

What is a Personal Line of Credit? For the unaware, a personal line of credit is a set amount of money you can withdraw from whenever you need it. They’re basically a loan—a lender provides you with the money, and you can choose to repay it either right away or over a specific period of time.

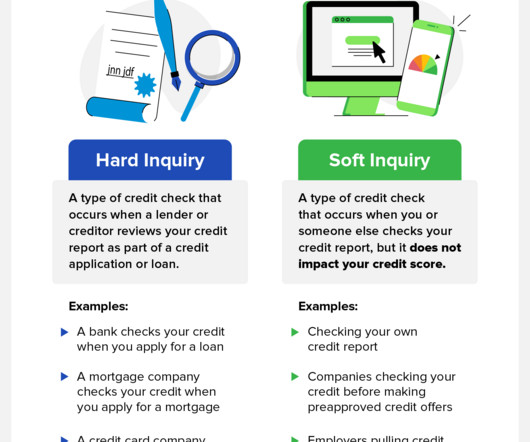

Your credit score is an important aspect of your financial health and is oftentimes used by lenders, landlords, and even employers to determine your creditworthiness. Hard inquiries , also known as hard pulls, are typically made by lenders and other financialinstitutions and can harm your credit score.

Incorrect Personal Information Lender Inquiries You Don’t Recognize Accounts You Never Opened Credit Utilization Goes Up Credit Score Goes Up or Down Unexpectedly Public Records You Don’t Recognize. Warning Sign 2: Lender Inquiries You Don’t Recognize. Warning Signs of Identity Theft. How Do I Check My Credit for Identity Theft?

One reason that lenders look at credit mix is to make sure that you can be responsible with multiple types of credit. Showing that you can handle different types of credit—and multiple credit accounts at once—indicates financial reliability to potential lenders. You are not required to pay the loan in full each month.

Both savings accounts and money market accounts are insured by the Federal Deposit Insurance Corporation (FDIC ) with certain financialinstitutions, and in both cases, you generally get instant access to your cash. Lenders scrutinize your credit report—and they look for a good mix of account types.

If you don’t have a credit history to show that you know how to manage credit or have derogatory marks on your report, credit card companies may be reluctant to loan you money via a credit card. Secured credit cards are different because rather than borrowing from a financialinstitution, you borrow from yourself.

These negative marks on your credit report indicate you might not pay your bills on time—or ever, which is why lenders don’t like to see them. Learning how to remove collections from your credit report can help you clean up your credit history and open better financial doors in the future. Do you recognize the listed lenders?

Compare Rates on Debt Consolidation Loans. If you’re in a financial rough patch, don’t panic. First, call all your lenders and tell them what’s going on. Many financialinstitutions offer deferments, temporarily lower payments, low-cost structured repayment plans and other reassuring options—but only if you ask.

There are many types of loans for a variety of purposes, but it’s always critical to consider certain key criteria in detail before making any final decisions. Even a few small differences between lenders and the loans that they’re offering can have an impact on your finances. Important Tips for Securing a Low-Interest Loan.

When you take out a mortgage, a financialinstitution agrees to lend you enough money to purchase a home. In exchange, you promise to make monthly payments until you’ve paid off the loan balance. Before approving your mortgage application, a lender needs to know you have the ability to pay back the loan.

According to the FICO scoring model, the following are the typical ranges: Exceptional: 800–850 Very Good: 740–799 Good: 670–739 Fair: 580–669 Poor: 300–579 Your credit score is a simple way for financialinstitutions to gauge risk. Lower credit scores are often a red flag and signal to lenders that a person may not pay back a loan.

Best of all, you can have accounts with multiple institutions, maximizing convenience. There’s no one-size-fits-all financialinstitution that works for every consumer on the planet, but there are some reasons you might want to choose a credit union over a brick-and-mortar or online bank. Personalloans.

Harmoney selected Finvi’s Katabat solution to support its efforts of changing the traditional personal lending model to put the customer at the center, and to use technology and data to make money more human. About Harmoney Harmoney is the only 100% consumer-direct personallender operating across Australia and New Zealand.

When your scholarships, grants, and federal student loans aren’t enough to cover the cost of college, it may be time to turn to a private lender. Private student loans can help you bear the weight of tuition. College Ave also stands out for being fee-free, as they don’t charge application fees or loan origination fees.

While it is possible to get a loan with no credit through some lenders, you may face high interest rates and unfavorable terms. Luckily, there are alternative ways to get a loan with no credit history. Table of Contents: What Is a No-Credit-Check Loan? Continue reading to discover how to get a loan with no credit score.

You’ve likely also heard that a good credit score is essential to getting a mortgage, or a good deal on a personalloan for a car. We talked to finance and credit card experts to get their insight into why lenders care so much about credit, and what you can do to get a good credit score or fix a bad one. Ads by Money.

When the Federal Reserve raises interest rates, financialinstitutions increase their rates accordingly, so those with variable interest rate loans may need to pay more interest than when they initially borrowed the money. Sadly, numerous people struggle to obtain reasonable loans when interest rates are this high.

Other professions have programs that help repay student loans with monthly assistance, one-time payoffs, or matching funds. No matter what or when, contact your lender if you believe you will be unable to make a student loan debt payment. Lenders are usually very open to figuring out a payment plan. Why is it important?

Information reported includes: Personal Information. This section of your credit report tells potential lenders who you are. Who is the person attached to all this credit history? If you see an old phone number, chances are it is still on file with the financialinstitution that issued the loan or credit card.

Looking at the bigger picture, banks, lenders, financialinstitutions, industry and commerce are all now facing the same challenges — on a macro scale. It will also put financialinstitutions in a prime position to flourish in the evolving banking sector.

Building a successful startup comes with its fair share of challenges, chief amongst them being the search for loans and funding. While chasing that dream investment, startups often face a tough time trying to secure loans, primarily due to minimal or no revenue. This can make it easier to justify the loan to yourself and the lender.

Depending on how much capital a business needs and what kind of interest rate it’s willing to pay, the following types of small business loans are available to them: Installment loans. Personalloans. Short-term loans. Some loans may require a personal guarantee from an owner or director. Microloans.

Mexico’s regulatory environment allows lenders to use the credit history of the people in a credit applicant’s household to score them,” said Alejandro Cardini, chief product officer at Círculo de Crédito. Lenders trust the FICO Score. You can read more about this story in the full media release. “The

Personalloans are a flexible type of financing that allows you to borrow money from banks and lenders and use that money however you see fit. You can typically use these loans however you want, with some offering interest rates as low as 5.91%. Lower scores can make it tough to qualify for a loan.

With inflation proving more sticky than policymakers had hoped and uncertainty around how the new administrations policies might affect it, it may take longer for people to see lower interest rates on their mortgages, car loans and credit card balances, which could prove challenging to household budgets.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content