This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A personalloan is money borrowed from a lender that can be used for almost any purpose, from debt consolidation to home improvement projects. Most people don’t have $5,000+ sitting in their bank accounts—that’s where personalloans come in. What Is a PersonalLoan? Why Would I Need a PersonalLoan?

Everything is online these days—including personalloans. Online lenders make it easy to compare rates and terms and find the right online personalloan for your situation. Personalloans were the fastest-growing category of consumer debt in 2019 , according to a survey from J.D.

Whether you’re making a big purchase or just refinancing some existing debt, a personalloan could help. But comparing loan options could take days — unless you use an online marketplace like Fiona which lets you compare personalloan offers side by side within minutes. How Fiona Loans Work.

Each year, tens of millions of Americans facing similar situations turn to personalloans to help ease the financial burden. With low interest for borrowers with strong credit scores, fixed rates, and a variety of lending sources to choose from, it’s easy to see why personalloans are so enticing. Rates & Fees.

The best personalloans charge low fees and low fixed interest rates, have flexible loan amounts and terms, and have no prepayment penalties. A personalloan could let you access cash for any purpose. Since personalloans are unsecured, you’ll need an excellent credit score to get the best deal.

When filing for bankruptcy, you can discharge certain types of personalloans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personalloans you can discharge and which filing method suits your financial situation.

And her bank wouldn’t give her and her husband Larry a loan to buy a replacement home. Brenda’s still tending her garden, though, thanks to a second-chance loan from the New Hampshire Community Loan Fund-a Community Development FinancialInstitution (CDFI). Flexible loan amounts.

The ending of various pandemic-era benefits including the pause on student loan payments will impact consumers in the coming months. The amendments lay out a more prescriptive recipe for the safeguards financialinstitutions must have in place around collecting, storing and transmitting consumer information. 9%) to $17.05

If you need money now, an online personalloan can be a fast and easy way to secure funds. Whether they’re for debt consolidation, a home improvement project, or other expenses, these loans often come with low-interest rates and flexible repayment options. Ad If you're struggling to make ends meet, a PersonalLoan can help.

THE NEW ERA OF CONSUMER LENDING In today ’ s rapidly evolving financial landscape, the significant increase in consumer lending presents new challenges for financialinstitutions, particularly in managing collections.

Credit Builder Loans. Credit builder loans aren’t widely publicized, but they are a great way to build credit without a credit card. Smaller institutions like credit unions are generally more likely to offer credit builder loans specifically to help borrowers build credit. Passbook or CD Loans. Peer-to-Peer Loans.

Indiana Attorney General Todd Rokita and the Indiana Department of FinancialInstitutions announced a settlement in excess of $250,000 with Integrity Acceptance Corp., As part of the settlement, the entities will forgive $223,685 in loans, pay $33,991 in restitution, and pay $33,000 in civil penalties and costs to the state.

A bank is a financialinstitution with a license to hold and lend money. It can provide checking and savings accounts, credit cards, mortgages, auto loans, personalloans, small business. Spencer Tierney writes for NerdWallet. Email: spencer.tierney@nerdwallet.com. Twitter: @SpencerNerd.

What is a Personal Line of Credit? For the unaware, a personal line of credit is a set amount of money you can withdraw from whenever you need it. They’re basically a loan—a lender provides you with the money, and you can choose to repay it either right away or over a specific period of time.

Securing a loan can be a big financial decision with a lot of implications on your personal finances and your life. There are many types of loans for a variety of purposes, but it’s always critical to consider certain key criteria in detail before making any final decisions. difference over the duration of the loan.

When your scholarships, grants, and federal student loans aren’t enough to cover the cost of college, it may be time to turn to a private lender. Private student loans can help you bear the weight of tuition. The key to finding the right student loan with the lowest rates and best terms is to shop around. Sallie Mae.

What many people don’t realize is that now is the time to take advantage of low-interest loans. Interest rates are bottoming out at historic lows , which means that it is more affordable than ever to borrow money from financialinstitutions. The old loan is paid off and a new one is created at a better interest rate.

You can start by getting a secured credit card, becoming an authorized user, or getting a cosigner on a loan. A low credit score leads to higher interest rates, larger deposits, and a low approval rate for loans and lines of credit. On your own, you may not receive approval on a personalloan or car loan.

In recent years, the rise of digital lenders like SoFi and Ally has transformed the lending landscape, offering borrowers new options for obtaining loans quickly and conveniently. And how can you navigate the process of shopping for a loan with them? But what sets these digital lenders apart from traditional banks and credit unions?

Basically, credit scoring models want to see that you can manage different types of financing, most notably revolving accounts, such as a credit card, and installment accounts, such as a mortgage or auto loan. You are not required to pay the loan in full each month. Why Does Your Mix of Accounts Matter?

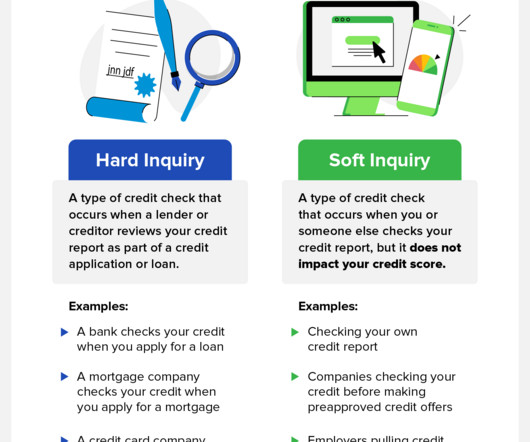

Identity thieves are almost always opportunistic—but the crimes they commit feel very personal. Unauthorized credit card charges, bogus loan applications, missing money, and other financial violations make fraud a major nightmare. Hard enquiries from companies you don’t recognize are a different matter.

Whether you’re applying for a loan or simply want to stay on top of your credit score, these tips will help you access your credit information without causing any harm. Hard inquiries , also known as hard pulls, are typically made by lenders and other financialinstitutions and can harm your credit score. What’s a Hard Inquiry?

While it is possible to get a loan with no credit through some lenders, you may face high interest rates and unfavorable terms. Luckily, there are alternative ways to get a loan with no credit history. Table of Contents: What Is a No-Credit-Check Loan? Continue reading to discover how to get a loan with no credit score.

If you want to lose the plastic altogether, think about applying for a debt consolidation loan. Go for a loan with a low interest. Then, avoid putting any more money on credit cards until you’ve paid off most of the consolidation loan. . Compare Rates on Debt Consolidation Loans. How Can I Get Out of Debt with No Money?

Harmoney selected Finvi’s Katabat solution to support its efforts of changing the traditional personal lending model to put the customer at the center, and to use technology and data to make money more human. About Harmoney Harmoney is the only 100% consumer-direct personal lender operating across Australia and New Zealand.

Both savings accounts and money market accounts are insured by the Federal Deposit Insurance Corporation (FDIC ) with certain financialinstitutions, and in both cases, you generally get instant access to your cash. Installment accounts are products like personalloans and car loans, which have fixed monthly payments.

Best of all, you can have accounts with multiple institutions, maximizing convenience. There’s no one-size-fits-all financialinstitution that works for every consumer on the planet, but there are some reasons you might want to choose a credit union over a brick-and-mortar or online bank. Auto loans. Personalloans.

Building a successful startup comes with its fair share of challenges, chief amongst them being the search for loans and funding. While chasing that dream investment, startups often face a tough time trying to secure loans, primarily due to minimal or no revenue. Personal term loans can be a viable option for startups with no revenue.

Lewis, who started the company with his wife Linda in Lubbock in 1986 after a career in banking, knew that meant a lot of his employees didn’t have a way to save money, get loans, and other benefits of working with a financialinstitution. So the Lewises and a few others started a credit union.

Raising interest rates typically slows down the economy as well as the rate of inflation, but these rates have a direct impact on people’s ability to obtain new loans. Here’s what you need to know about getting a new loan and interest rate after bankruptcy.

Though adoption of digital banking and e-commerce has grown substantially in the past three years, it isn't the case that all consumers prefer to use digital means, namely web portals or mobile apps, to apply for new accounts, cards, or loans. Accounts via Digital, Loans Not as Much. Digital Considered Less Secure.

When you take out a mortgage, a financialinstitution agrees to lend you enough money to purchase a home. In exchange, you promise to make monthly payments until you’ve paid off the loan balance. Before approving your mortgage application, a lender needs to know you have the ability to pay back the loan.

With a 680 credit score, you can get approved for credit cards as well as personal, auto, and home loans. Having a low credit score not only makes it difficult to secure lines of credit and loans, but it can also cost you quite a bit of money. It shouldn’t be a problem to qualify for a mortgage loan with a 680 credit score.

Established credit history can impact everything from getting a future loan (such as a mortgage) to renting an apartment. Monthly expenses might include student loan payments, car payments, and credit card payments. Pay Student Loan Debt. Even in bankruptcy, student loan debt cannot get discharged; it must get paid.

Some of the largest United States banks are bracing themselves for some significant losses coming out of their portfolio of personalloans and credit cards as indicated by their financial reports covering the second quarter of 2024. billion from its revenues to raise its loan loss provision to a staggering amount of $3 billion.

You’ve likely also heard that a good credit score is essential to getting a mortgage, or a good deal on a personalloan for a car. Simply put, lenders will use this number to make a determination about how likely you are to pay back a loan, based on your history of paying off your credit cards. Ok, got it.

That line of credit will then be reported to the credit reporting bureaus as a collection account—a collections account for a credit card, personalloan, etc.—and If you have an otherwise blemish-free credit history, go ahead and ask the financialinstitution for a goodwill deletion.

If you see an old phone number, chances are it is still on file with the financialinstitution that issued the loan or credit card. The types of credit accounts you can expect to see in this section include: Mortgages , home equity loans, and home equity lines of credit. Student Loans. Auto Loans.

Looking at the bigger picture, banks, lenders, financialinstitutions, industry and commerce are all now facing the same challenges — on a macro scale. It will also put financialinstitutions in a prime position to flourish in the evolving banking sector.

2: Digital literacy IS NOT financial literacy. digital natives might not be who financialinstitutions think they are. For example, credit cards (71%), cell phone billing (64%) and personalfinancial accounts like checking and deposits (62%) were the top accounts that customers were prepared to open digitally.

It applies to various credit transactions, including credit cards, mortgages, and personalloans. Debt collectors must comply with TILA’s disclosure requirements when collecting debts related to consumer credit.

Instead, you’ll have to find a financialinstitution or company that permits self-directed IRAs. This financialinstitution is known as an IRA custodian. Some banks allow an IRA to get a mortgage loan. It can be counter-intuitive for a brokerage firm to promote diverting funds out of the stock market.

The report – Americans’ Shadow Financial Lives: The Mobile Apps Banks Don’t Know They Use – found that U.S. financial services customers are increasingly engaged in behaviors and relationships that are deeply meaningful and are not on the radar screens of their incumbent providers. Let’s start with an example.

Last year, the Indiana Department of FinancialInstitutions (IDFI) increased the bankruptcy exemption amounts. These exemptions still apply because they decrease the amount that you’ll need to pay back to creditors with your repayment plan. Why Did Bankruptcy Exemptions Increase in Indiana?

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content