This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Amidst the chaos of the pandemic, federal and state governments have made efforts to protect against the financial strain U.S. consumers are enduring—including mortgage payment forbearance of foreclosure. Federally backed mortgages are protected against foreclosure through December 31, 2020. What Is a Forbearance?

As discussed in parts 1-4 of this series, lenders have several options prior to instituting a commercial foreclosure action. Additionally, as briefly discussed in part 5 of this series, during the foreclosure action, lenders have options to try to preserve the value of the underlying collateral and to minimize further losses.

On May 3, the New York State Senate passed S5473D (Bill), which will apply immediately in all actions “in which a final judgment of foreclosure and sale has not been enforced.” ( See S5473D at Section 10.) 3d 1 (2021), and retroactively annul lenders’ longstanding right to revoke their option to accelerate mortgage loans after default.

On December 30, 2022, New York Governor Kathy Hochul signed the Foreclosure Abuse Prevention Act (FAPA) into law. The Engel decision allowed lenders and servicers to voluntarily pause the statute of limitations on foreclosures and reserve the right to restart the action again, as long as it was done within six years. Engel , 37 N.Y.3d

Amidst the chaos of the pandemic, federal and state governments have made efforts to protect against the financial strain U.S. consumers are enduring—including mortgage payment forbearance of foreclosure. Federally backed mortgages are protected against foreclosure through December 31, 2020. What Is a Forbearance?

Two common loan options are conventional and FHA loans. A Federal Housing Administration loan, or FHA loan, is insured by the federal government. A conventional loan is not. But when it comes to conventional loans vs. FHA loans, which one is right for you? Conventional Loan vs. FHA Loan.

Fitch Ratings-New York-15 July 2022: Borrowers continue to work with their servicers post-forbearance to avoid loan default, according to Fitch Ratings’ 1Q22 U.S. The sole metric showing stress is in the foreclosure category, which rose marginally to 2% from 1% and to 3% from 2% for bank and non-bank servicers, respectively.

An “assignment of rents” allows the lender to collect the rent payments, if the borrower defaults on their loan payments. Although the lender and borrower may agree to the assignment of rents in the loan documents, the procedure for enforcing the assignment of rent is governed by Section 697.07, Florida Statutes. Conclusion.

million people carry some form of student loan debt, with most averaging around $39,000 —although many of us have a lot more. Refinancing your student loans could help lower your monthly payments and reduce your overall repayment amount. Keep reading for a deep dive into our picks for the seven best student loan refinancing companies.

This program offers a flexible framework for loans that helps eligible borrowers to modify their monthly mortgage payments and avoid foreclosure. Modifying the loan terms can make mortgage payments more affordable and sustainable for struggling homeowners. How Do Fannie Mae and Freddie Mac Work? But how does it work?

This all points to the likelihood of a protracted period of economic uncertainty as governments act to contain outbreaks when, and where, they appear. Further assistance was announced in July offering customers a further four month deferral or the option to restructure their loan. This also has implications for the property market.

So far the offers have been vague, the most likely concessions will be for your lenders on your home and cars to allow you to move a monthly payment to the end of the loan and for credit cards to temporarily reduce your interest rate. There are more tools for dealing with your mortgage than any other type of loan. Student Loans.

The United States Bankruptcy Code governs both chapter 7 and chapter 13 bankruptcy. Unlike Chapter 7, Chapter 13 bankruptcy enables you to decrease the interest rate on your vehicle loan and, in certain situations, the total amount owed. The lender protects the borrower against foreclosure. Chapter 7 (Liquidation).

If a borrower defaults on a SBA loan, the lender or CDC must assess the environmental risk of contamination before conducting any liquidation action that could result in a loss, or otherwise increase the risk of loss, due to the actual or alleged presence of contamination. SOP 50 10 5(E), Appendix 2. SOP 50 57 2 ; SOP 50 55.

COVID-19 loans for bad credit are on the rise—but do they deliver, or do they make things even worse? Economic injury disaster loan : If you’re a small business recovering from an economic disaster—the COVID-19 pandemic, for instance—you could be eligible for a loan from the SBA. Read this article to learn how to apply.

When government assistance is not providing enough income to cover job losses, should you file for bankruptcy or hold out for the economic recovery? Filers can typically retain the home and vehicle as long as you make payments on the loan. Federally managed student loans received an automatic six-month payment waiver.

The four key trends we’re studying are: resumed foreclosure activity, extensive medical bills, the end of child tax credits and historically high inflation. For one, the consumer credit market is looking strong with signs of expansion, specifically, originations for credit cards and personal loans are increasing. million U.S.

The Consumer Financial Protection Bureau (“CFPB”) hopes that these provisions will prevent a new foreclosure crisis when the majority of existing foreclosure moratoria implemented by state and federal governments expire over the course of this summer.

The Consumer Financial Protection Bureau (“CFPB”) hopes that these provisions will prevent a new foreclosure crisis when the majority of existing foreclosure moratoria implemented by state and federal governments expire over the course of this summer.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. For more information, click here. For more information, click here. On August 3, the Washington, D.C.

While the government created programs to assist those financially affected—such as the CARES Act—many who were already struggling before the hit of COVID-19 fell even further into debt. After the pandemic hit and it was evident that Americans were struggling to make ends meet, the government took action and enacted the CARES Act.

Today, the Supreme Court held that collecting government debt by robocalling cellphones didn’t deserve special First Amendment treatment. The Federal Government receives a staggering number of complaints about robocalls—3.7 The Government’s stated justification for the government-debt exception is collecting government debt.

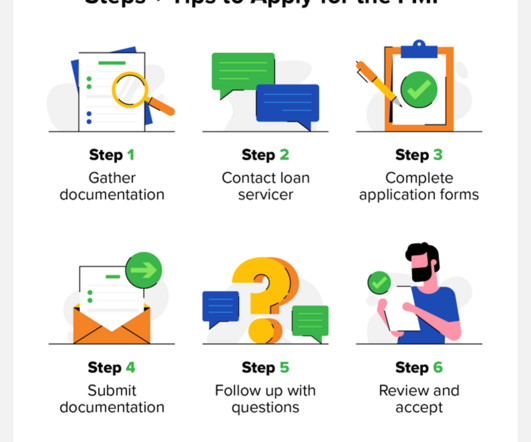

First, Make Contact With Your Loan Servicer. Before deciding how to move forward, your first step is to contact your mortgage loan servicer. Because loans are often sold to other lenders, it might not be the servicer that first agreed to grant you the mortgage. Refinance Your Loan. Loan Modification.

A mortgage is a type of secured debt , which means your lender can seize your property and sell it if you don’t repay the loan as agreed. In the mortgage industry, this is known as a foreclosure. The purpose of conducting a foreclosure is to repossess the property, sell it, and use the money from the sale to cover your loan balance.

. “So there are a few ‘Zero Down’ options, and some low down payment options, often backed by the government, designed to help remove that roadblock.” ” Of course, government-back Zero Down mortgages require a few qualifications, and navigating the world of low-down payments can also be tricky.

2] This result can be potentially disastrous to a mortgage lender that may lose the value of a first priority mortgage lien as security for the loan, and potentially have the mortgage subject to being foreclosed in a construction lien foreclosure lawsuit. Notices of commencement are governed by Fla. 2d 948, 950 (Fla. 713.132(4).

This leads some to fear that, without direct assistance for renters and/or landlords in the form of government funds, an even greater backlog of eviction cases will flood the courts once this CDC Order expires at the end of the year.

Prohibiting servicers of private education loans from reporting an adverse item of information relating to the nonpayment of the loan for an established period of time. Prohibiting servicers of private education loans from reporting an adverse item of information relating to the nonpayment of the loan for an established period of time.

Many people worry that bankruptcy will simply delay the inevitable, such as a lawsuit, wage garnishment, or a foreclosure, and that their creditors will still come after them. Pension loans: If you took out a loan against your pension, an automatic stay would not protect you from wage garnishment to repay the loan.

Many people worry that bankruptcy will simply delay the inevitable, such as a lawsuit, wage garnishment, or a foreclosure, and that their creditors will still come after them. Pension loans: If you took out a loan against your pension, an automatic stay would not protect you from wage garnishment to repay the loan.

Luisa Palmero signed five documents related to a reverse mortgage on their primary residence and homestead: (1) a residential loan application; (2) a home equity conversion loan agreement; (3) an adjustable-rate note; (4) a nonborrower spouse ownership interest certification; and (5) a reverse mortgage.

For the lender, it’s all about the bottom line, and if they think they can get more money from a foreclosure, they won’t agree to a short sale. Even if the lender does forgive the amount of the loan not paid upon closing, you may be taxed on this money by the IRS. A short sale is a significant negative on your credit score.

The number of people seeking bankruptcy fell sharply during the pandemic as government aid propped up income and staved off housing and student-loan obligations. Several rounds of government aid padded incomes with direct payments to households and enhanced unemployment benefits. Source: site.

The advisory opinion clarifies that a covered debt collector who brings or threatens to bring a state court foreclosure action to collect a time-barred mortgage debt may violate the Fair Debt Collection Practices Act and its implementing regulation. Read the blog, Zombie second mortgages: When collectors come for long forgotten home loans.

Short sales and loan modifications are viable alternatives to bankruptcy. You can never obtain a loan or a mortgage. The following are some of the most common bankruptcy myths in Littleton, Colorado: Myth #1: Short sales and loan modifications are viable alternatives to bankruptcy. Definitely not.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The department estimates the waiver will make roughly 22,000 borrowers immediately eligible to have their loans erased automatically.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The CFPB also provided individuals a series of questions to identify whether an emergency rental assistance program is a scam or legitimate.

The proposed amendments would establish a pre-foreclosure review period to provide an opportunity for borrowers affected by the Covid-19 pandemic to be evaluated for loss mitigation before a servicer files for foreclosure. 9056(a)(1)).”.

USDA and VA home loans traditionally don’t require down payments. Below, we’ll share our expertise to help you learn all about loans and mortgage options. Conventional Mortgage A conventional loan is a mortgage option that’s offered by a private lender instead of the government. How much money do you need to buy a house?

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. This action brings the total amount of loan discharges approved by the DOE since January 2021 to $9.5

It has taken actions to collect data on a number of new industries, including debt relief and earned wage access providers, and has filed a cease-and-desist order against a student loan debt relief company charging borrowers exorbitant fees for the false promise of getting their student debt wiped.

In the letter, Nussle stated, “Lenders rely on complete and accurate credit reports when underwriting loans. 2547, the Non-Judicial Foreclosure Debt Collection Clarification Act, which would reverse the unanimous decision made by the Supreme Court of the United States (SCOTUS) in 2019.

Other balances, which include retail cards and other consumer loans, increased by $15 billion. Auto loan balances rose by $20 billion, consistent with the upward trajectory seen since 2011. Student loan balances fell by $35 billion and stood at $1.57 Student Loans Outstanding student loan debt stood at $1.57

New York SPOC Requirements : As created effective January 2, 2022 , Section 6-o of the New York Banking Law required a lender to provide a single point of contact (“SPOC”) to a borrower who: (a) is 60 or more days delinquent on a “home loan”; and (b) chooses to pursue a loan modification or other foreclosure prevention alternative.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content