This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Consumer Financial Protection Bureau yesterday issued a Notice of Proposed Rulemaking (NPRM) that would prohibit mortgage servicers from starting foreclosure proceedings until 2022 while also providing servicers with the ability to offer streamlined loan modification options to homeowners who have been impacted by the COVID-19 pandemic.

The company was accused of violating consumer protection laws by attempting to collect on old debts tied to second-lien mortgages without proper communication or adherence to foreclosure-prevention measures. The company allegedly waited until borrowers were financially incapable of modifying their loans before attempting to collect.

There are few life events as stressful as a foreclosure. However, there are ways to prevent foreclosure, even if you can’t afford your mortgage payments. One of those methods is through a loan modification. What is foreclosure? Your lender will then notify you that you are in default and begin foreclosure proceedings.

When an Indiana homeowner is unable to make their mortgage payments, the lender eventually starts a foreclosure. The foreclosure process, if left to proceed, ultimately results in the house being sold off to settle all or part of the debt. Here are the important things you should know about Indiana’s foreclosure laws.

When you’re going through the process of filing Chapter 13, foreclosure cannot occur because you’re granted an automatic stay, meaning that lenders cannot pursue your debts and recover collateral, including your home. Can I Stop Foreclosure with Chapter 13 Bankruptcy? If you’re wondering, “How long will Chapter 13 delay foreclosure?”

consumers are enduring—including mortgage payment forbearance of foreclosure. Forbearance is the postponement of mortgage payments, or the lowering of monthly payments for a specified time period; it’s not loan forgiveness. Federally backed mortgages are protected against foreclosure through December 31, 2020.

When a lender holds a defaulted loan there are several issues that need to be considered before initiating a foreclosure. Additionally, specific Federal regulations may also apply and provide additional requirements for lenders holding VA loans or FHA loans, or provide protections for service members. Florida State Laws.

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. if the collateral is likely to be acquired by SBA or the lender at the foreclosure sale, the expenses associated with the care, preservation and resale of the acquired collateral. Lien Foreclosure.

In Florida, a lender initiates a foreclosure by commencing a lawsuit in the county where the property is located. If the lender is successful, the lender will receive a final judgment of foreclosure from the court and the property will be sold at a public auction. Sometimes, a lender’s foreclosure lawsuit will be dismissed.

Sometimes, foreclosure of a commercial property is the only option available to lenders and servicers to limit losses as a result of defaults on hotel and restaurant mortgages. Parts 1-4 of this series discussed pre-foreclosure options available to lenders dealing with hotel/restaurant mortgage defaults. 702.015(4) , Fla. York, 903 So.

The first half of this series evaluated options available to lenders prior to instituting a commercial foreclosure action. The second-half of this series has evaluated available options to lenders during the pendency of the foreclosure action. 1), directs the defendants to show cause why a foreclosure judgment should not be entered.

As discussed in parts 1-4 of this series, lenders have several options prior to instituting a commercial foreclosure action. Additionally, as briefly discussed in part 5 of this series, during the foreclosure action, lenders have options to try to preserve the value of the underlying collateral and to minimize further losses.

The Consumer Financial Protection Bureau yesterday announced it had filed suit against a developer and lender for operating an illegal land sale scheme and targeting Hispanic borrowers with loans they couldn’t afford, many of which ended up in foreclosure and allowed the company to repeat the process.

When you are struggling to pay your bills, there may come a point where you are faced with deciding between bankruptcy vs foreclosure. If you are facing foreclosure or bankruptcy, the best way to determine which choice is right for you is to speak with an experienced bankruptcy attorney. Bankruptcy vs. Foreclosure: Which is Worse?

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. if the collateral is likely to be acquired by SBA or the lender at the foreclosure sale, the expenses associated with the care, preservation and resale of the acquired collateral. Liquidation Methods.

On May 3, the New York State Senate passed S5473D (Bill), which will apply immediately in all actions “in which a final judgment of foreclosure and sale has not been enforced.” ( See S5473D at Section 10.) 3d 1 (2021), and retroactively annul lenders’ longstanding right to revoke their option to accelerate mortgage loans after default.

Conducting site visits are an important aspect of servicing SBA loans. a bankruptcy filing, business shutdown, or foreclosure by a prior lienholder) that caused the loan to be classified in liquidation status or sooner if the collateral could be removed, lost, or dissipated. SOP 50 57 2 ; SOP 50 55.

And her bank wouldn’t give her and her husband Larry a loan to buy a replacement home. Brenda’s still tending her garden, though, thanks to a second-chance loan from the New Hampshire Community Loan Fund-a Community Development Financial Institution (CDFI). Flexible loan amounts. Flexible loan amounts.

With the COVID-19 foreclosure moratoriums over, housing foreclosures are once again on the rise nationally. In fact, in September of 2023, we saw home foreclosures on the rise by a whopping 18.4% Foreclosures in Indianapolis have also been increasingly more common. from this time last year.

MA non-judicial mortgage foreclosure can take about 120 days, or four months, to complete. Judicial foreclosures vary depending on your state. A nonjudicial mortgage foreclosure can take about 120 days, or four months, to complete. Judicial foreclosures vary depending on your state. What Is Foreclosure?

In the event a borrower is seriously delinquent on making payments under a SBA loan, or the SBA loan is classified in liquidation status, lenders and CDCs must develop a prudent and commercially reasonable strategy to maximize their recovery on the loan. SOP 50 57 ; SOP 50 55. SOP 50 57 2; SOP 50 55.

When you’ve missed a mortgage payment your mind may immediately spiral to foreclosure. Foreclosure. But, it should bring you some peace of mind to know that foreclosure is not the immediate consequence for missing a loan payment. Foreclosure doesn’t really come up until you’ve missed two or three payments.

In Florida, foreclosure actions must be brought in the county where the land is located. However, lenders often wonder where they should file the foreclosure action if the loan is secured by mortgaged land situated in different counties. allows the lender to bring a single foreclosure action on all mortgages in just one county.

On December 30, 2022, New York Governor Kathy Hochul signed the Foreclosure Abuse Prevention Act (FAPA) into law. The Engel decision allowed lenders and servicers to voluntarily pause the statute of limitations on foreclosures and reserve the right to restart the action again, as long as it was done within six years. Engel , 37 N.Y.3d

consumers are enduring—including mortgage payment forbearance of foreclosure. Forbearance is the postponement of mortgage payments, or the lowering of monthly payments for a specified time period; it’s not loan forgiveness. Federally backed mortgages are protected against foreclosure through December 31, 2020.

When homeowners face the daunting prospect of foreclosure, understanding the defensive options available can potentially help them preserve their homes and financial stability. For example, two common types of bankruptcy , Chapter 7 and Chapter 13, offer different benefits and drawbacks in the context of foreclosure.

The first-half of this series evaluated considerations for lenders faced with borrowers who were unable to meet their mortgage and loan obligations. The second-half of this series evaluated options available to lenders during the commercial foreclosure process. Opportunities to Gain Concessions in Loan Workouts with Existing Borrowers.

Lenders must pay particular attention to subordinate liens and encumbrances prior to initiating any foreclosure action. Lenders can discover whether subordinate liens and encumbrances exist on a property by performing a title examination prior to initiating foreclosure. & Loan Ass’n, 214 So.2d Subordinate Liens.

On Tuesday, March 23, 2021, four of our partners presented Properly Handling Mortgage Foreclosures. This webinar addressed what is new in foreclosures, including recent developments in the law since the last foreclosure crisis and how banks can utilize the law to their advantage. There is a tenant in the foreclosed property.

However, lenders are not always the successful party in the foreclosure and, to the disappointment of the lender, the lawsuit may be dismissed. 2016) , lenders may be able to file a foreclosure lawsuit on the same property more than once. In this case, the mortgagee brought two foreclosure lawsuits against the mortgagor.

In order to maintain a foreclosure action against a borrower, lenders must ensure they can establish “standing”. Standing is a fundamental requirement for a foreclosure, as lenders who desire to initiate a foreclosure proceeding are required to have standing. Aurora Loan Services, LLC, 163 So. What is Standing?

Fitch Ratings-New York-15 July 2022: Borrowers continue to work with their servicers post-forbearance to avoid loan default, according to Fitch Ratings’ 1Q22 U.S. The sole metric showing stress is in the foreclosure category, which rose marginally to 2% from 1% and to 3% from 2% for bank and non-bank servicers, respectively.

In just a few days, on July 31, 2021, the national moratoriums on residential evictions and foreclosures are set to expire. The new program is aimed at reducing the monthly payments for individuals with qualifying mortgage loans. Department of Agriculture. 1] The White House, www.whitehouse.gov , July 23, 2021.

Lenders need to be aware that borrowers and other lienholders can bring an action or proceeding to set aside, invalidate, or challenge the validity of a final judgment of foreclosure of a mortgage, even after the foreclosure sale. When Can the Foreclosure Sale Be Invalidated? Nationstar Mortg., Diaz , 227 So. 3d 726, 730 (Fla.

In every foreclosure action, the foreclosing lender will be required to publish some sort of legal advertisement or notice in a newspaper (e.g. the Notice of Foreclosure Sale). Since publishing a legal notice concerning a foreclosure action is inevitable, it is imperative for lenders to know how to do so properly. Conclusion.

Office loan defaults pose a high risk for major US financial districts, potentially signaling impending issues for large cities. A new study by The Kaplan Group analyzed office building data in key US financial districts to determine which are most at risk of a large number of loan defaults or even geo-centric office firesales.

Engel, the Court of Appeals established a bright-line rule that when the acceleration of a mortgage debt occurs by filing a foreclosure complaint, a lender’s voluntary discontinuance of that action constitutes a revocation of acceleration as a matter of law, absent an express, contemporaneous statement to the contrary by the lender.

Except in cases of an owner-occupied residence, lenders are entitled under Florida law to receive payments during the pendency of a foreclosure proceeding. Courts have held that reference to “some other method of enforcement” of a court’s payment order includes the entry of a foreclosure judgment. 2), Florida Statutes.

Two common loan options are conventional and FHA loans. A Federal Housing Administration loan, or FHA loan, is insured by the federal government. A conventional loan is not. The backing of the federal government makes FHA loans a bit easier to qualify for because they’re considered less risky for lenders.

In 2017, the Lender moved for summary judgment against Mr. Kessler on its foreclosure complaint. On February 14, 2023, the New York Court of Appeals overturned the Appellate Division, Second Department’s Kessler decision, which had applied a strict application of Real Property Actions and Proceedings Law § 1304, also known as a 90-day notice.

An “assignment of rents” allows the lender to collect the rent payments, if the borrower defaults on their loan payments. Although the lender and borrower may agree to the assignment of rents in the loan documents, the procedure for enforcing the assignment of rent is governed by Section 697.07, Florida Statutes. 3d 932, 934 (Fla.

In 2013, the Legislature enacted Section 702.015 , Florida Statutes, which sets forth new pleading requirements for residential foreclosure actions. At that time, the Legislature requested the Florida Supreme Court to amend the Florida Rules of Civil Procedure to provide expedited foreclosure proceedings in conformity with Section 702.015.

John's University School of Law American Bankruptcy Institute Law Review Staff Section 362 of title 11 of the United States Code (the “Bankruptcy Code”) provides that the filing of a bankruptcy petition results in an automatic stay generally enjoining all actions, including a foreclosure sale, against a debtor or its property. [1]

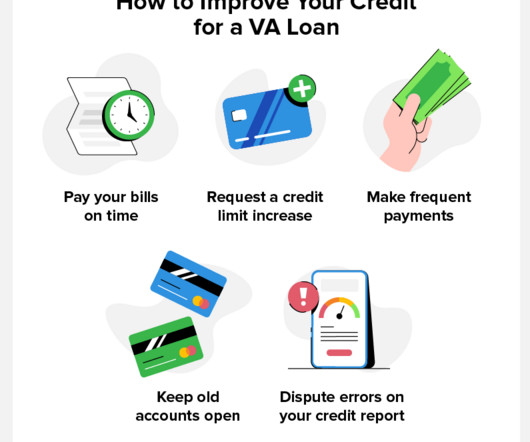

A VA home loan is a mortgage backed by the Department of Veterans Affairs (VA) for service members, veterans, and their families. The purpose of VA loans is to help veterans purchase homes with lower interest rates and better terms. Read on to learn how to get a VA loan with bad credit. What Are the Benefits of a VA Loan?

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content