This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It’s a common scenario: You apply for a personalloan or credit card and get denied. The reason seems shrouded in mystery, and you receive a letter with language such as “lack of recent installment loan information” or “proportion of balances to credit limits.”

Depending on the specific credit bureau or bureaus that your vehicle loanlender reports to, it will only show up on those credit reports. There are three different credit bureaus that are mainly used by all lenders: Experian, Equifax, and Transunion. What Is an Installment Loan? What Contributes to Your Credit Score?

One reason that lenders look at credit mix is to make sure that you can be responsible with multiple types of credit. Showing that you can handle different types of credit—and multiple credit accounts at once—indicates financial reliability to potential lenders. You are not required to pay the loan in full each month.

If you’ve gotten behind on payments to a creditor or lender, your debt could be sent to collections after around 120 days of missed payments. Paying off collections can help your credit score if the lender reports to new credit scoring models, including FICO 9®, FICO 10®, VantageScore 3.0® ® and VantageScore 4.0®.

Debt is the amount of money you owe to a lender or creditor. Some examples of debt are mortgages, credit card dues, and personalloans. Although accruing lots of debt isn’t ideal, it may sometimes be unavoidable, such as mortgage payments or student loans. They may still be responsible for paying a portion of the loan.

You can find a certified credit counselor through trade groups like the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA). Debt consolidation loans are another popular way to pay off credit card balances. In comparison, the average credit card interest rate is 16.44%.

When you stop making payments on an auto loan, the lender will take the vehicle back. Your first option is to start negotiating with your original auto lender. This could be a bank, an online lender like Capital One, or the in-house finance company at the dealership. It means your lender has lost money on your loan.

million identity theft reports were filed with the Federal Trade Commission—that’s almost double the number from 2019. The more account types you have in good standing on your credit report, the more likely you are to get approved when you go for a low-interest car loan, personalloan, or mortgage.

Lenders, business partners and others can evaluate this worthiness by looking at the business’s credit report and score. Why can’t you just use your personal credit? First, if you take out personalloans to pay for business expenses, you’re wholly liable for the debt. That’s right.

Other professions have programs that help repay student loans with monthly assistance, one-time payoffs, or matching funds. No matter what or when, contact your lender if you believe you will be unable to make a student loan debt payment. Lenders are usually very open to figuring out a payment plan. Why is it important?

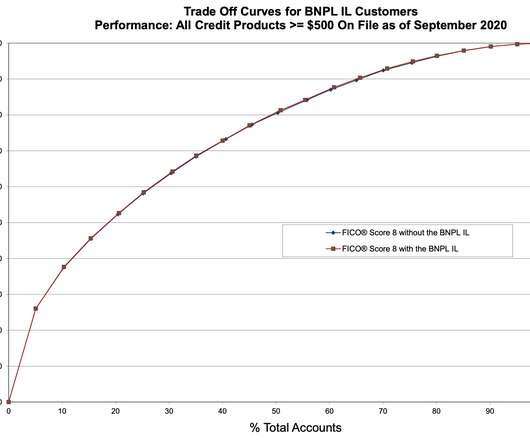

market: BNPL reporting approach: How a BNPL lender reports these accounts to a credit bureau can materially influence the impact these loans ultimately have on the FICO® Score. Trade-off curves are also referred to as Lorenz curves or lift curves. personalloans and credit cards) reported in the credit file.

Exchange-traded funds. Depending on how much capital a business needs and what kind of interest rate it’s willing to pay, the following types of small business loans are available to them: Installment loans. Personalloans. Short-term loans. Commercial property loans. Commercial vehicle loans.

Debt settlement firms expect you to stop paying your lenders and make monthly installments into a secure trust instead. While waiting for money to build up in your secure trust, the debt settlement firm won’t send any to your lenders. Many lenders decide it’s in their best interests to agree. Sounds a little too easy?

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content